Summary

- Stage Store Inc, heavily depends on in-store clients to push sales amid Geo-restrictive e-commerce applications.

- The company has a negative net cash balance owing to the high outstanding debt as compared to the cash holdings.

- With an EV/Sales ratio of 0.44, the company will be open for a possible take over in the near future.

Stage Store, Inc’s SSI reliance on the WEB@POS program as a driver of e-commerce in the company will be short-lived if the company does not expand its merchandise mix sales potential. This program is exclusive for in-store guests and it allows customers to access the entire online experience. With the company’s future now pegged on the off-price sales strategy, it is imperative to upgrade the sales strategy. In this article I will explain why I am neutral about going long in the company based on a focus on the merchandise mix in the long term prospects of Stage Stores

The company that deals with trendy apparel, footwear, home appliances and cosmetics has carved its market on a relatively small ground. Its departmental stores are located in small rural locations and also midwestern states courtesy of the newly acquired Gordmans off-price stores. CEO Michael Glazer has stated that the company's e-commerce platform grew by double digits in 2018, with the WEB@POS program accounting for a 50% sales drive (in-store)

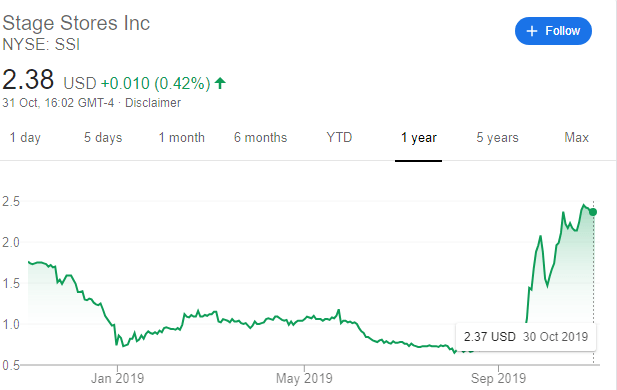

Currently trading at $2.89 as of Nov. 12, 2019, Stage Stores Inc’s stock price has become too affordable to go unnoticed, despite a rally dating back to August. The factors that contributed to the bullish run include:

- Conversion of more than 90 departmental stores to off-price

- Test departmental conversions at lower costs before 2020

- Success of the Gordmans' acquisition including 158 off-price stores

- Planned closure of up to 40 under-performing stores through 2020

Negative Net Cash Outlook

Stage Stores had an outstanding share balance of 28,610,700 (as recorded on the Q1 report on April 17, 2019). The cash holding for the same period was $15,830,000 (less total assets) and the total debt stood at $255,106,000. The net cash balance is thus $-239,276,000 (cash minus outstanding debt). This negative cash balance spells doom for equity shareholders since they would receive no money in the event of the company's liquidation.

EV/Sales

The debt problem escalates to the calculation of the company's enterprise value. With a market capitalization of $60.06 million, Stage Store's enterprise value is $ 697,003,000. The total revenue for 2019 as reported in the first quarter was $1.641 billion. The EV/ Sales ration stands at 0.44 signalling unattractive future prospects of the company. On a positive note though, the total assets of the company are worth $744.161 million meaning the company is highly unlikely to be declared insolvent.

Stage Stores signed a revolving credit facility of $350 million on October 6, 2014, that matured on Oct. 6, 2019. The gross profit ending the quarter of 2019 was $390.6 million. Without considering other liabilities and assuming Stage Stores, will pay all its debt at once, there will only be $40 million left (assuming fixed interests) for running the company's working capital. The net capital expenditures reported in 2018 was $30.1 million. This leaves out a slim chance for growth through the financial year 2019-2020.

Store Count

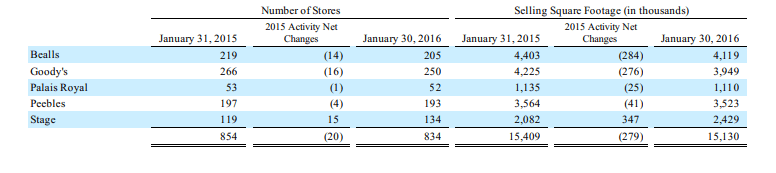

In 2015, Stage Stores Inc, had 854 stores that later reduced to 834 by January 2016. The following table shows the stores against the area coverage of each store. The total footage of the selling square was 15,130,000 feet.

Source: SSI Annual Report of 2015

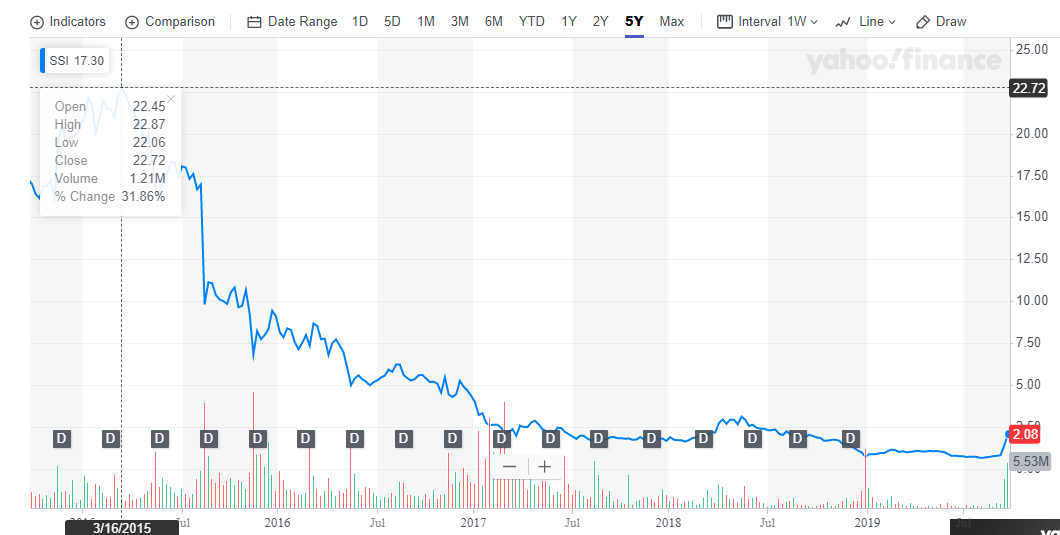

A five year analysis, shows that Stage Stores stock hit a record high in March 2015 after rising to 22.72 (31.86% rise).

Source: Yahoo Finance

At the time, the company had recently closed 23 stores and opened three new stores, with up to 30 stores slated for closure in 2016. However, the company was working on its Style Circle Rewards program that saw it improve sales through customer rewards, especially for credit cardholders. However, the net sales as of 2015 were $1,638.6 billion a difference of $58.5 million from 2019 when the revenue slowed to $1580.1 billion.

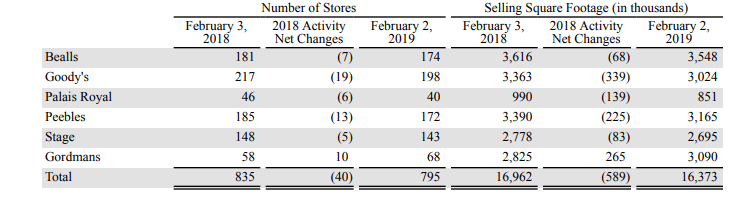

In the Financial Year 2018-2019, Stage Stores Inc, acquired Gordmans and the store count is as follows:

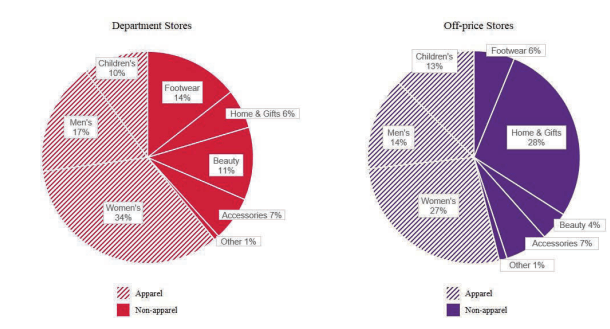

Although the total store coverage reduced by 4% the area square footage increased to 16,373,000 representing an 8.2% increase in selling space. This increase in selling square (with a focus on markup) is seen to have a positive correlation with total sales as far as the FY 2018-2019 is concerned. The difference between sales on departmental stores and off-price stores is shown below

Items such as women's attire (34%), men's (17%) and beauty (11%) were relatively higher in departmental stores than in off-price stores in FY 2018-2019. This correlation shows that the absolute conversion of the departmental stores into an off-price strategy may not form a total turnaround for Stage Stores.

Comparison With JC Penney

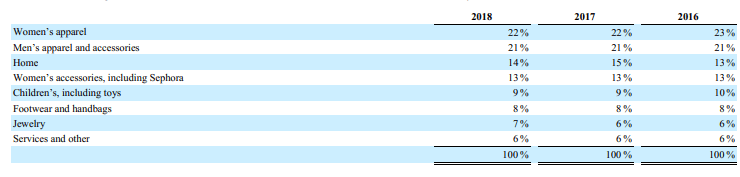

The long-term downtrend in Stage Stores lends itself to a comparison with one of its competitors, JC Penney JCP, which is down 92% since 2016. The following table shows the merchandise mix of JC Penney based on the net sales since 2016.

Source: JC Penney

Among the items that recorded the highest sales were women's apparel (22%), men's commodities (21%) and beauty (13%) in 2018. These three items have been the most sought after in the three-year analysis of JC Penney. As at February 2019, the company operated 864 departmental stores covering a selling space of 95.0 million square feet. The net sales for the 3-year period was $11.664 billion (in 2018), $12.554 billion (in 2017) and $12.571 billion (in 2016).

With an outstanding debt of $4 billion and a cash holding of $333 million (less total assets worth $7.721 billion), the company's net cash balance stands at $-3.687 billion. The market cap of JC Penney was $285.52 million on September 27, 2019. The enterprise value is thus $3.973 billion. However, due to the company's high asset base of $7 billion, it is imperative to consider JC Penney's mode of operation as the cause of the slowing fortunes.

In-Store Online Operations

Like Stage Stores JC Penney also operates on an in-store online basis. Through its Geopolitically restricted website, the company ensures that clients shopping online can only do so from within the store. Clients are required to download the JC Penney app from the company's website and with the help of store associates complete the purchase. This method saw the company's net sales for the period 2018 decrease by $890 million as compared to 2017. Stage Stores also saw a decrease of $12 million in net sales from $1,592 million in 2017 to $1,580 million in 2018.

While we cannot attribute the drop in sales to one sector such as online sales, it is still expedient to recognize the role of available sales platforms. By restricting access of the website outside the stores across the United States and beyond, both Stage Stores and JC Penney have faced significant net losses.

Conclusion

The decision by Stage Stores to limit online sales to in-store clients is detrimental to the company's overall profitability. While some products do well in off-price trading others do well in departmental stores. Full exploitation of three items namely: men's apparel, women and beauty products/ accessories should be conducted to ensure they are not fully converted to off-price trading. They do well in departmental stores as compared to the off-price stores. A spot check on the company's enterprise value shows that it is higher than the market capitalization. We think Stage Stores may be considering a possible takeover in the near future. Since the EV/ Sales ration stands at 2.35, it thus signals an unattractive future prospects of the company although the stock may hold off at a neutral ground for a while. My call to investors is to go neutral in the long run.

Disclaimer: The author is long Stage Stores

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.