Heading into a trading week packed with a pivotal Federal Reserve meeting and another flutter of earnings news, major stock averages have now retraced about half of the “panic selloff” that rocked a sleepy August.

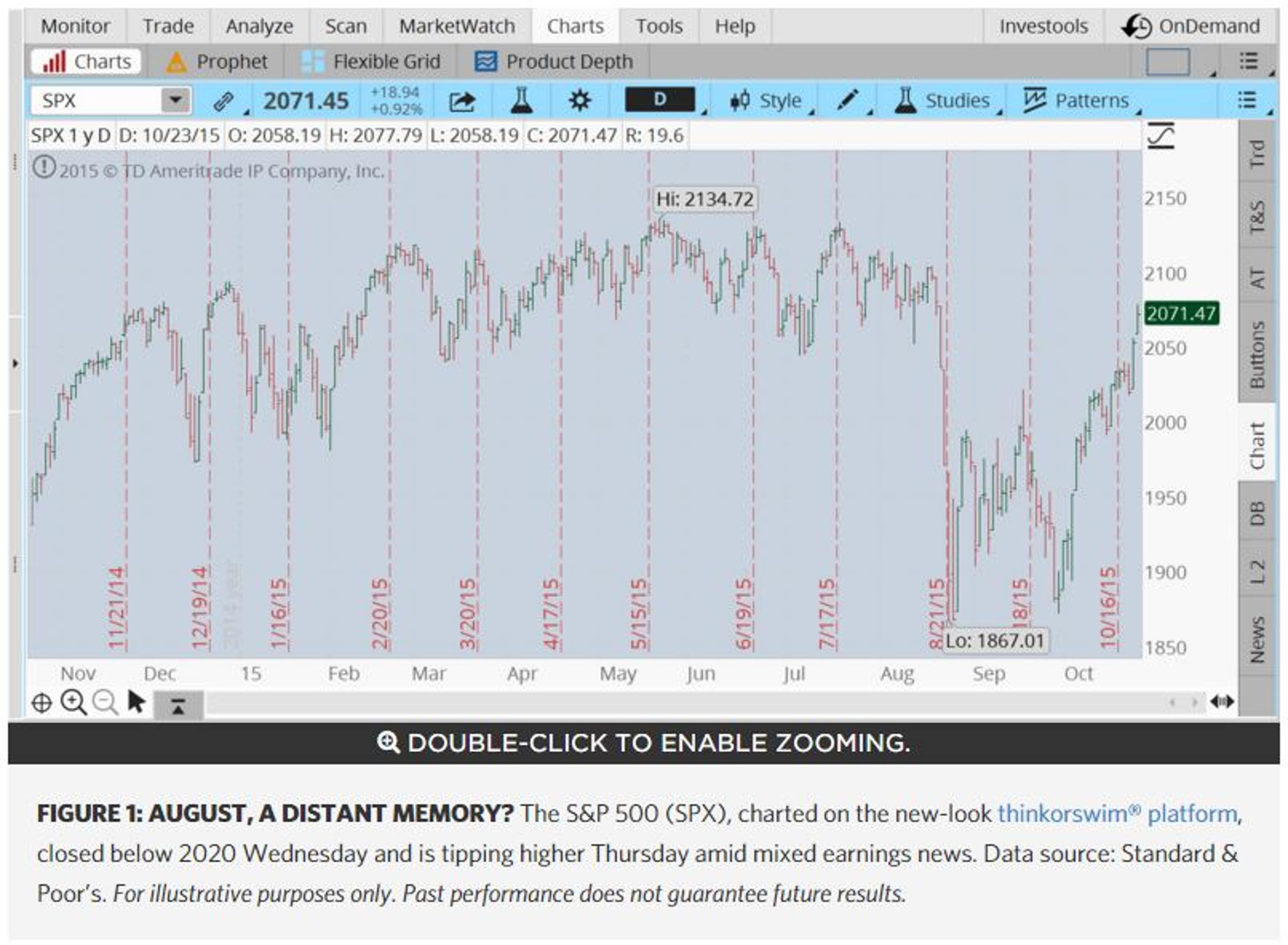

The S&P 500 (SPX), pushed above 2070 on Friday, sits above its August 25 closing low, but is still 4.6% below its May 21 record high (figure 1). The drop in SPX has paired with a 41% drop over three months for the CBOE Volatility Index (VIX), one measure of broad-market jitters (figure 2).

That fairly quick recovery may leave stock averages vulnerable to profit taking should this coming week’s earnings fail to reach the bar set when a trio of technology heavies—Microsoft Corporation MSFT, Alphabet Inc GOOG GOOGL, and Amazon.com, Inc. AMZN—largely beat Street expectations.

In fact, that threesome capped a week that featured mostly encouraging earnings news across select industrials and consumer companies. Analyst sentiment on Q3 earnings has improved thanks to a string of stronger-than-expected results from blue-chips. It appears that Wall Street analysts, and perhaps investors, are getting used to reports tinted by a global economic slowing and a strong dollar’s dent on multinationals’ profits. Estimates and share prices may better reflect corporate reality, inviting mostly upside surprises when the numbers are off target.

Delicate Situation For The Fed

Company-focused news will share the marquee with a two-day Fed gathering that at one time was considered to be all but a lock for an interest rate hike. No so true anymore. The strong dollar, China-triggered global growth worries, and inconsistent U.S. economic indicators have potentially sidelined the central bank’s plans to reverse recession-era interest rate levels. For now.

The Fed wraps its two-day session with a statement at 2 p.m. Eastern on Wednesday, October 28. The majority of Fed watchers expect no action from the panel then, but market-driving news could still emerge especially if the Fed lays any groundwork for its December meeting and early 2016.

The CME Group’s FedWatch Tool, calculated based on pricing in the Fed funds futures market, shows traders are pricing in about a 7% chance the Fed moves next week to raise rates for the first time since 2006. The tool shows about a 39% shot for a rate hike in December and a 60% chance for a hike in March.

The Fed—with rhetoric that indicates it’s poised to raise rates at the first sign the U.S. is back on track—is a rogue among its central bank brethren. Most other large-nation central banks are either cutting rates—China cut benchmark lending rates on Friday for the sixth time in roughly a year—or have shown little intention to remove ultra-loose policy anytime soon. Just last week, the European Central Bank (ECB) made it clear that extra stimulus measures are still on the table as needed. The Bank of Japan is holding its own monetary policy meeting on Oct. 30.

A couple of economic indicators could be of particular importance to a convening Fed. On Tuesday, durable goods data hits. It can be a useful indicator for gauging whether improving hiring trends are producing the kind of wages that translate into big-ticket spending. The first look at Q3 gross domestic product (GDP), the broadest measure of the economy’s health, hits the tape on Thursday (see the full economic calendar in figure 3 below).

Shiny Apple?

Inclusion of specific security names in this commentary does not constitute a recommendation from TD Ameritrade to buy, sell, or hold. Market volatility, volume, and system availability may delay account access and trade executions. Past performance of a security or strategy does not guarantee future results or success. Options are not suitable for all investors as the special risks inherent to options trading may expose investors to potentially rapid and substantial losses. Options trading subject to TD Ameritrade review and approval. Please read Characteristics and Risks of Standardized Options before investing in options. Supporting documentation for any claims, comparisons, statistics, or other technical data will be supplied upon request. The information is not intended to be investment advice or construed as a recommendation or endorsement of any particular investment or investment strategy, and is for illustrative purposes only. Be sure to understand all risks involved with each strategy, including commission costs, before attempting to place any trade. Clients must consider all relevant risk factors, including their own personal financial situations, before trading. TD Ameritrade, Inc., member FINRA/SIPC. TD Ameritrade is a trademark jointly owned by TD Ameritrade IP Company, Inc. and The Toronto-Dominion Bank. © 2015 TD Ameritrade IP Company, Inc. All rights reserved. Used with permission.Come Tuesday post-close, Apple Inc. AAPL is in the hot seat. Can it repeat the general upbeat tone delivered for other big-name tech this earnings round? Investor expectations could be running high for any management chatter on expected holiday sales. Investors will also be dissecting iPhone upgrade sales against the risk that a global slowdown has eaten into sales.

A poll of analysts by S&P Capital IQ shows a consensus of 40 analysts looking for $1.29 per share in AAPL’s fiscal Q4, up from $1.18 a year earlier. The survey pegs revenue at $39.4 billion, up from $37.5 billion a year earlier.

Plenty More Earnings, Too

Monday’s earnings line-up is lengthy and features a trio of pharmaceutical giants: Bristol Myers Squibb BMY, Pfizer PFE, and Merck & Co., Inc. MRK, a sector that could continue to draw interest as the political climate heats up. Tuesday also features results from Twitter Inc TWTR as Wall Street continues to rate its leadership shuffle. Other social media earnings releases include LinkedIn Corp LNKD on Thursday. Facebook Inc FB is up with its results on November 4.

The energy sector has seemingly been off the radar for a few weeks but that could change as Exxon Mobil Corporation XOM and Chevron CVX release results on Friday. U.S.-traded crude fell to a three-week low, widening its discount to Europe-traded Brent. Prices recently tried but failed to test $50 a barrel again as U.S. inventories expanded for a fourth week through Oct. 16, keeping supplies more than 100 million barrels above the five-year seasonal average, according to the Energy Information Administration.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.