Get a full recap of this week's outlook in the video below:

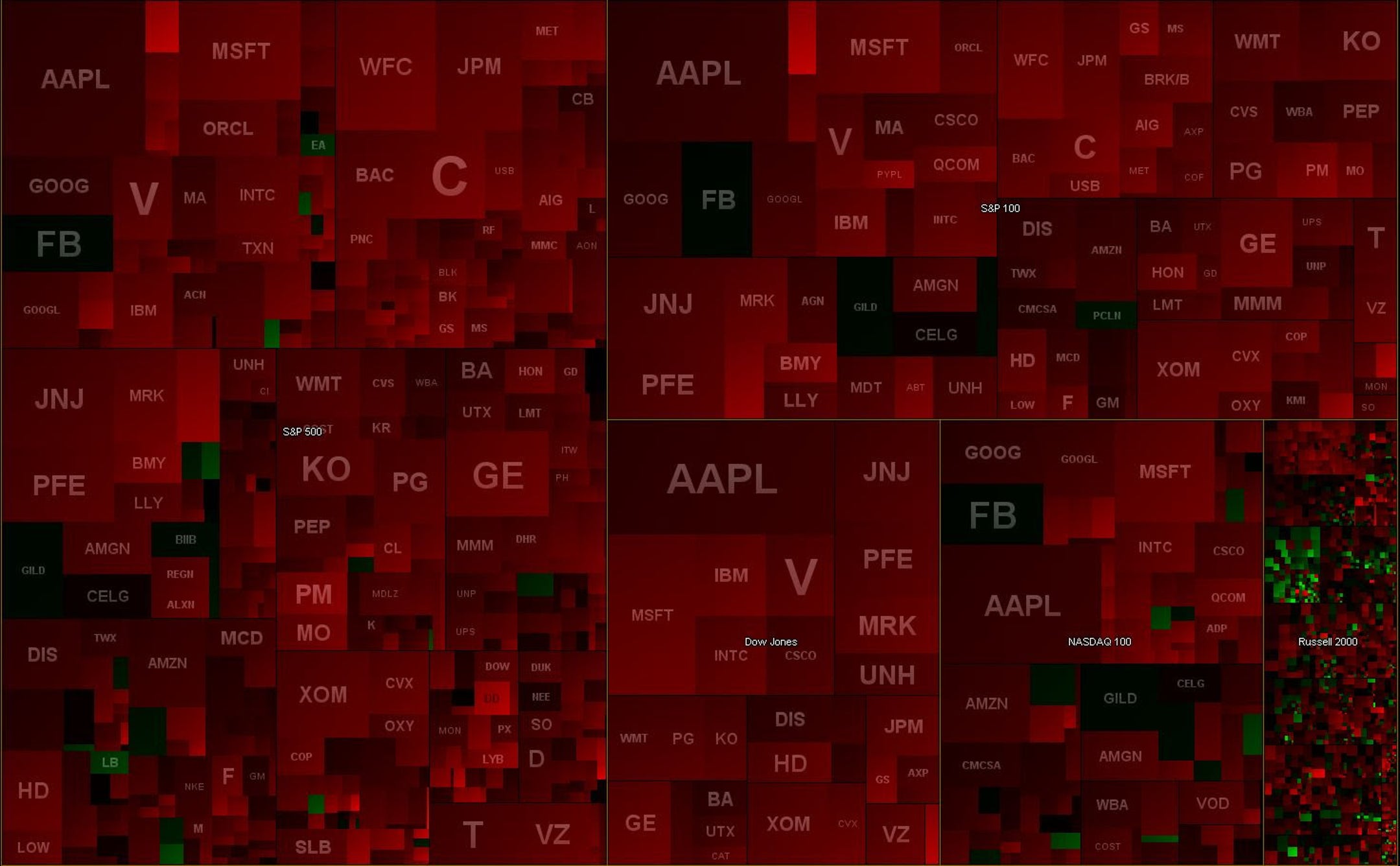

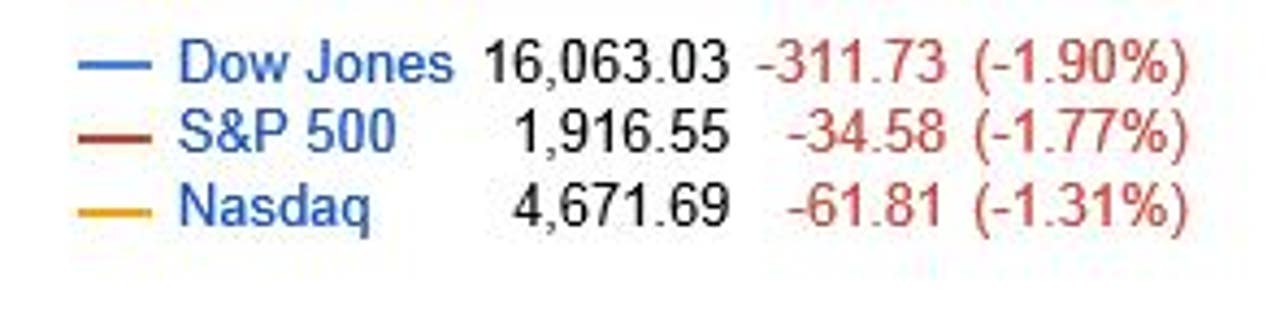

Scoreboard

With the lack of hopium sources, equity markets ended the week on a sour note.

Friday

The Friday close was largely saved from much worse results by Apple Inc. AAPL mightily defending the 108.5 level (see the chart lower). Nevertheless, the day was red.

Why the Friday fall? CNBC blamed the strong employment reports, especially the 5.1 percent unemployment level.

However, that point is contestable. The support? Bond rallied and rates plunged.

This is hardly a sign of rate hike fears. A strong U.S. bond market indicates that traders are pricing in an event outside the United States.

A more likely cause? China. Their markets are set to reopen on Monday after being closed for two days. This opens door of potentially severe drops there that can easily spill into global markets.

Moreover, this notion is also obvious with under-performances from Baidu Inc (ADR) BIDU and Alibaba Group Holding Ltd BABA.

The only Friday effect of the Fed/Hike was that markets did not get signal of a delay in the hike. So that contributed to the downside by not providing hopium that bulls could buy.

Monday/Tuesday

Luckily, U.S. traders will watch as the Chinese markets reopen and how the globe deals with any resulting issues. If the Chinese reopen goes smoothly Monday and global markets react calmly, then U.S. markets are likely to bounce a little Tuesday.

Variables In Focus

Current price movement are largely due to sentiment and headline trading. The fundamentals are still on hold. The main focus points as of late have been catalysts for price fluctuations. Here is an update on those drivers:

Apple: It's a heavyweight and recently proved what it can do when it moves 4.5 percent in one day (for example, causing a 1 percent move in the PowerShares QQQ Trust, Series 1 (ETF) QQQ). Image Credit: Public Domain

The good news is that Apple is the best case for value on the planet. The bad news is that technically one can make the case for another round of failures in its stock price.

Regardless, the one certainty is that markets will react and will likely react negatively when the announcement comes in two weeks. Consequently, the savvy reaction is to remain cautious.

On Friday, crude spiked on a rig count report only to fall back to deep red. Notice the absence of fundamentals. That is a prime example how sentiment and headlines trump fundamentals in turbulent times.

Note Of Caution

Last week's cautionary note about ranges remains relevant. The recent flash crash and recovery have created price elasticity, meaning that it's now easier to have +/-1.5 percent market moves than normally.This is dangerous because any future incident that would have under normal circumstance caused a -1 percent move now can cause a -3 percent move; hence the extra caution.

VIX closed +8.5 percent, while markets only down -1.5 percent. Perhaps the disconnect is due to pricing in the potential downfall from the week's China reopen.

Be careful chasing runups that are not based on fundamentals. No change in thesis. Manage current risk.

Don't chase; don't panic. Be cautious.

Ranges

A visual to how things have changed since just a few weeks ago.

Tickers:

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Date of Trade | ticker | Put/Call | Strike Price | DTE | Sentiment |

|---|

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.