After tacking on another 2.5% over the past few weeks, the S&P 500 (SPX) scratched out a fresh record high heading into the final four trading days of April.

But another steady drip of earnings reports—kicked off by Apple’s AAPL post-close release on Monday—and the latest glimpse into the mind of the Federal Reserve could potentially test stock rally conviction.

Apple’s not the only headliner.

Results from the energy, consumer discretionary, health care, and industrials sectors are also due out as the Q1 earnings season pushes into its second half; emphasis is likely to remain on the potential negative drag from a strong dollar on overseas profits and lackluster revenue following slowing global economic growth.

Almost 30% of the S&P 500 (SPX) is due to report their earnings this week. Among the 202 SPX companies that have already reported, earnings per share are up 8.7% year over year on flat revenues, according to Zacks Investment Research.

Can Apple Push Tech Momentum?

While the market’s slow grind so far in April seems to have instilled a renewed sense of broad-market confidence, earnings have been a catalyst for many individual companies over the past two weeks.

Most of the big banks have already released results, and so have notable large tech names like Google GOOGGOOGL, Microsoft MSFT, and Amazon.com AMZN. Post-earnings tech share gains helped drive the tech-heavy NASDAQ Composite to a record high 5,100 last week.

Monday is Apple’s turn—the No. 1 traded stock at TD Ameritrade. Momentum surrounding Apple Watch and company figures that show it’s sold more iPhone 6 Plus models than expected leave Wall Street expecting a positive Q2 earnings report and upbeat guidance. The average stock rating on Apple is overweight.

Analysts expect Apple to report GAAP earnings per share of $2.14 and adjusted earnings, or non-GAAP, of $2.19, which would mark a 24% year-over-year improvement from Apple’s $1.77 per share in the previous period.

Muffled Response to Earnings

Earnings have been just good enough to keep the broader stock market afloat (afloat meant new record highs, after all). At the same time, revenue disappointments (and a few revenue warnings for coming quarters) have kept stock gains in check.

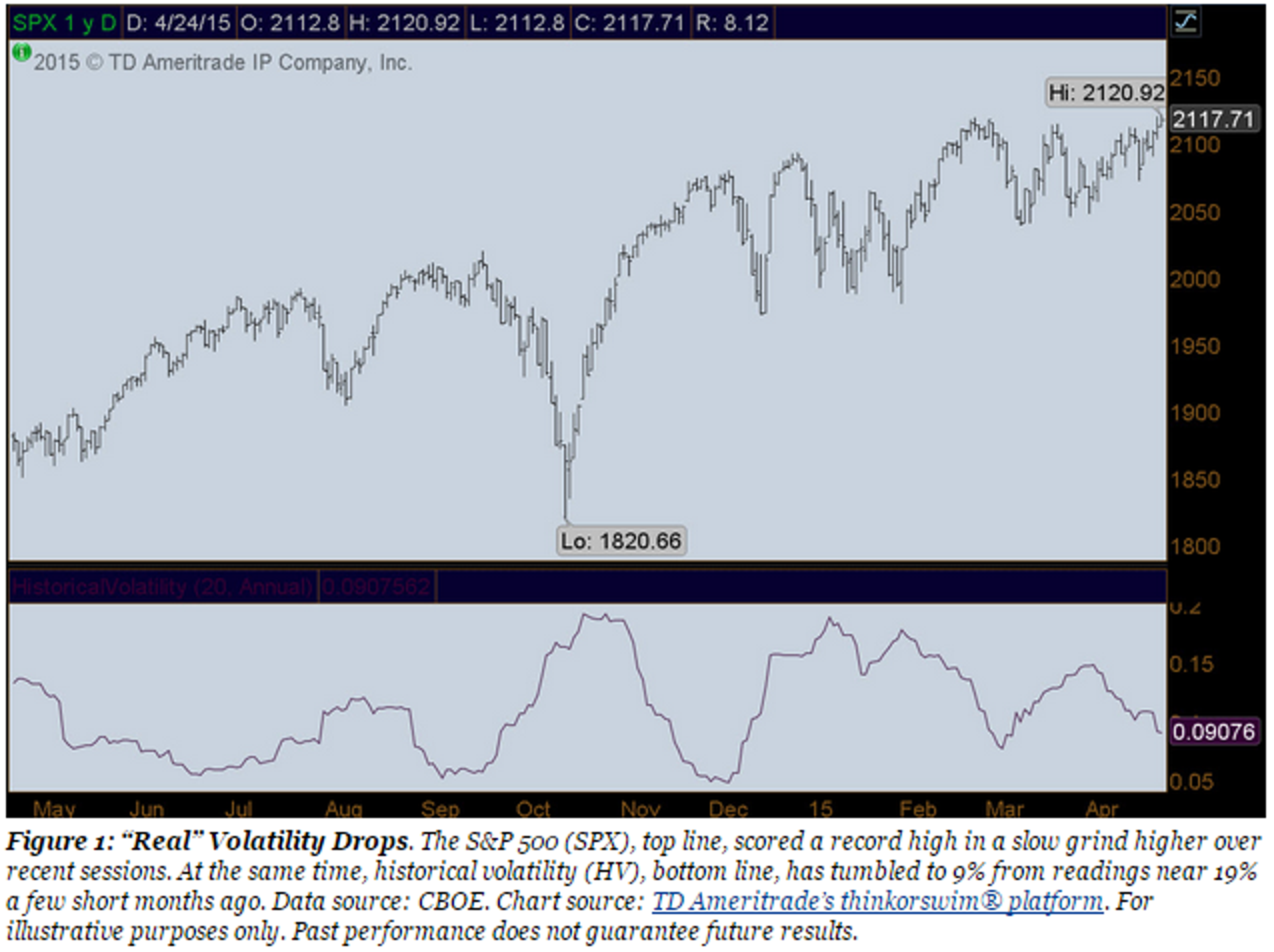

The SPX’s latest leg higher was a slow grind to say the least; the average daily move in the index so far this month is 9 points. Compare that to the 15-point daily swings seen in March. What’s more, actual SPX volatility might be easing. Its 20-day historical volatility (HV) has dropped to 9%, well off the 15% from early April and readings nearing 19% in January (figure 1).

The CBOE Volatility Index (VIX) is slipping as well. While HV measures volatility based on closing prices (annualized standard deviation), VIX reflects the implied volatility priced into short-term SPX options. In other words, it tracks volatility expectations.

VIX hit 2015 lows of 12.12 intraday Thursday and finished the week at 12.35. That’s down 11% on the week. In fact, Friday marked the lowest close for the index in more than four months (figure 2).

Sometimes called the market’s “fear gauge,” VIX, is considered a broad measure of investor sentiment. When it spikes, as it did in October 2014 to above 31, the jump in the index is typically viewed as a sign that risk perceptions are elevated and investors are becoming more pessimistic or bearish. Now, with the index at its lowest levels since December 5, 2014, is VIX at the opposite extreme? And once at an extreme, is sentiment simply bullish, or overdone? For sure, earnings may need to deliver more than the status quo to justify another big push in stocks.

A More Cautious Fed?

The pace of economic reports picks up after a bit of a lull last week. Data on consumer confidence Tuesday and gross domestic product (GDP) Wednesday come into focus before the Federal Reserve concludes a meeting Wednesday afternoon. Although officials aren’t expected to change rates at the April meeting, post-meeting commentary could shape expectations for changes in monetary policy later this year. Most had prepared for the Fed to ramp up its hints at interest rate increases in the second half of 2015 or early 2016. More recently, however, some industry analysts think the Fed may offer a more downbeat economic assessment this week. It’s hard to speculate until we hear from the Fed itself.

Reports on jobless claims, manufacturing, auto sales, and construction spending are due out in the second half of the week. But unless the Fed disrupts Wall Street with new thinking on the pace of upcoming interest rate hikes, investors may opt to largely ignore economic reports (figure 3) leading up to the May 8 employment report.

Good trading,

JJ

This piece was originally posted here by JJ Kinahan on April 27, 2015.

TD Ameritrade, Inc., member FINRA/SIPC. Commentary provided for educational purposes only. Past performance of a security, strategy, or index is no guarantee of future results or investment success. Inclusion of specific security names in this commentary does not constitute a recommendation from TD Ameritrade to buy, sell, or hold.

Zacks Investment Research is separate from and not affiliated with TD Ameritrade.

Options involve risks and are not suitable for all investors. Please read Characteristics and Risks of Standardized Options before investing. Supporting documentation for any claims, comparison, statistics, or other technical data will be supplied upon request.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.