Iron Mountain Incorporated IRM, the reigning global business records storage king, now has a REIT castle to go along with its storage business moat.

Revenues from the Iron Mountain document storage business have increased for 25 consecutive years. Now, the company could be poised to deliver a very competitive dividend yield as a newly crowned REIT.

Mr. Market Rewards REIT Conversion

Dividends Galore, Plus Special Dividends And "Catch-Up" Dividends

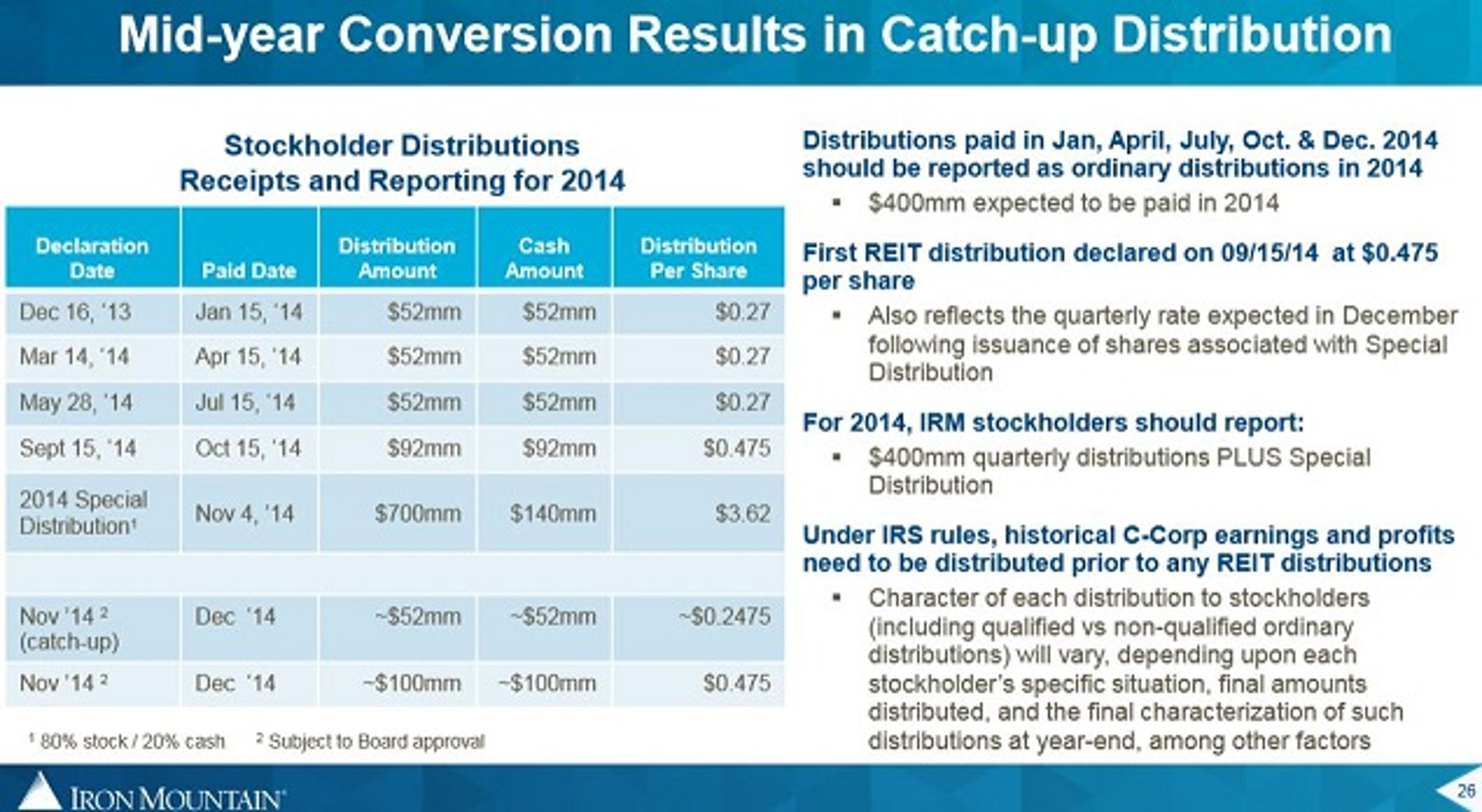

The slide below clarifies how the company plans to increase its dividend distributions to "catch up" with minimum 90-percent distributions of taxable earnings required to take advantage of REIT tax status retroactive to January 1, 2014.

(IRM - Morningstar Presentation 9/17/14)

Shareholders of record as of September 30 will receive a $0.475 dividend per share on October 15, plus a $3.62 Special Distribution on November 4, and a "catch-up" dividend of ~$0.2475, as well as the regular quarterly dividend of $0.475 per share to be paid in December.

At the close of trading on September 22, IRM was trading at $35.32 per share. Based upon the recently declared regular dividend of $1.90 per share, the yield would be 5.38 percent.

However, that significantly understates the actual yield for 2014 based upon a total estimated payout of $4.8175 for shareholders of record September 30 prior to the end of the year.

Key Takeaways: Morningstar - Management Behind The Moat Presentation

Iron Mountain is three times larger than its closest competitor.

A significant part of the Iron Mountain moat flows from marketplace dominance -- especially with large enterprise customers. An estimated 950 of the Fortune 1000 are Iron Mountain customers.

Final Thoughts

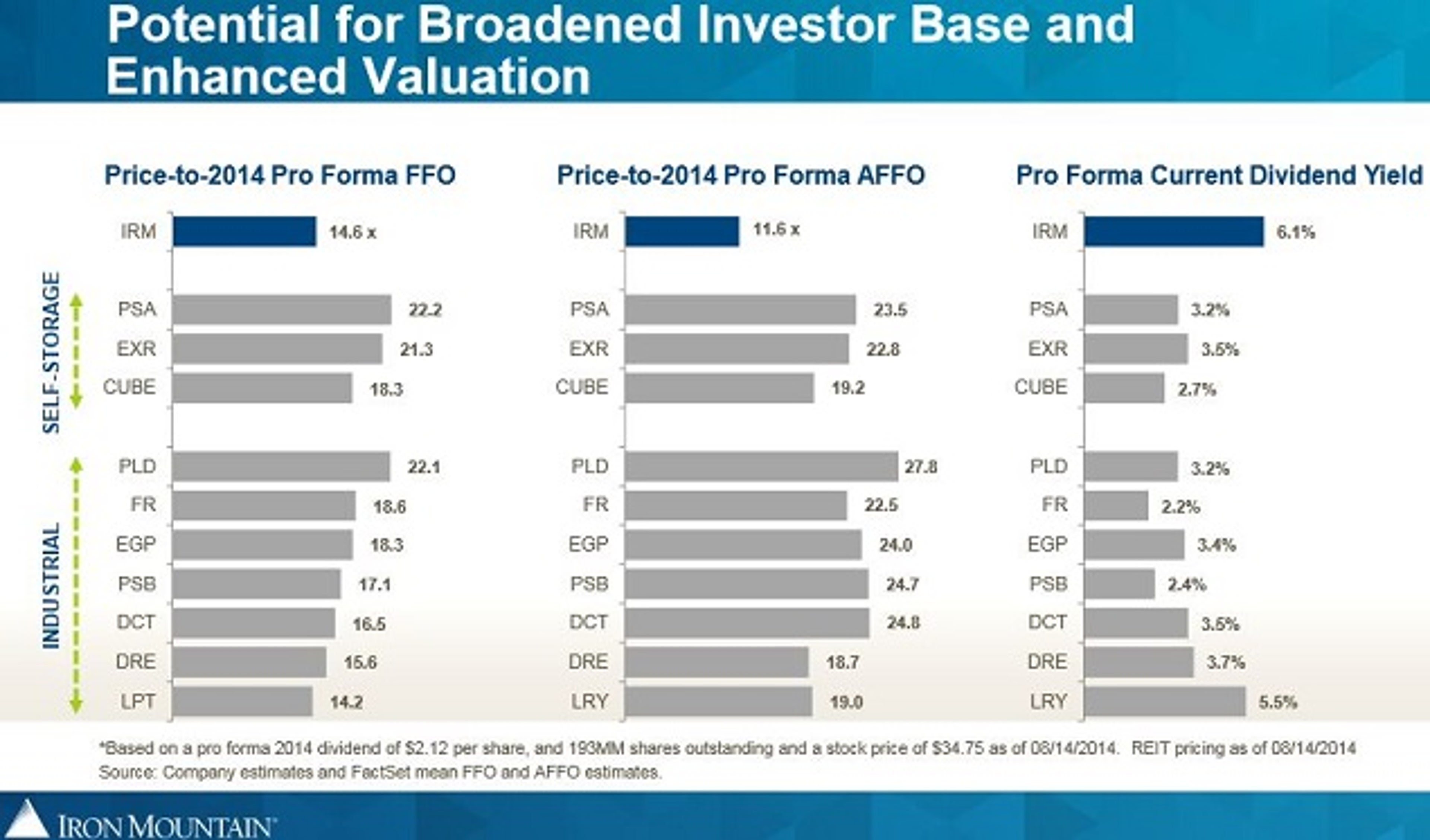

Iron Mountain appears to be an attractive value proposition based upon key REIT metrics such as Price to FFO, Price to AFFO and a very competitive dividend yield.

The storage of critical business documents has proven to be extremely sticky for Iron Mountain, with the average life of a record box in storage being 15 years. This contributes to the Iron Mountain enterprise document storage business, having demonstrated a history of being recession-resistant -- another sign of a competitive moat.

Disclosure: At the time of this writing, the author had no position in the equities mentioned in this report.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.