Connect The Dots

The University of Michigan’s Consumer Sentiment dropped from 91.9 to 85.7 – the lowest level in a year.

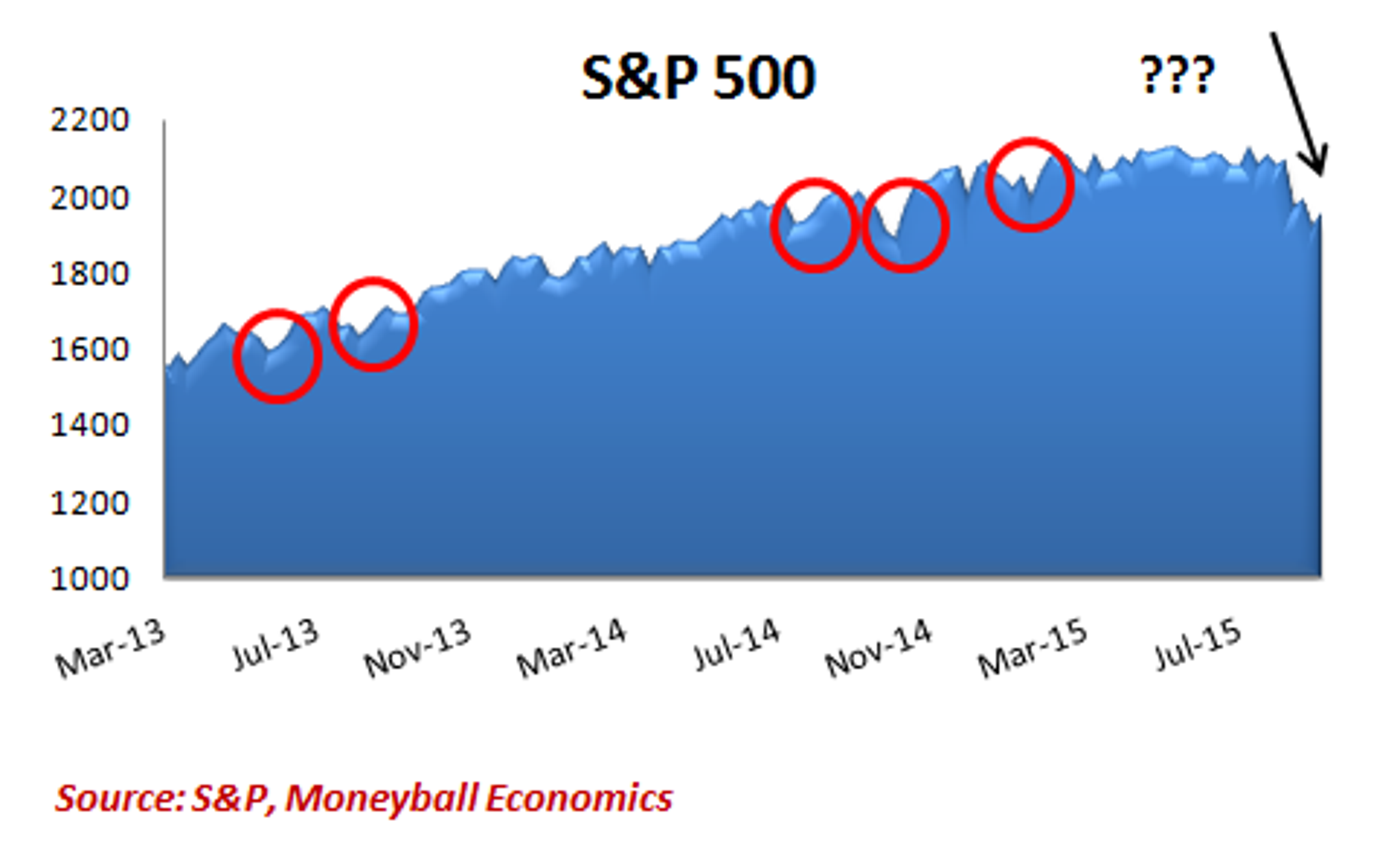

Meanwhile the S&P 500 remains down, -5% year over year and -10% since July.

It’s no coincidence that consumer sentiment stumbled at the same time that the stock market plunged.

Coming back from Summer vacations, households saw:

- The deepest drop in 401K wealth in years

- The most prolonged drop in years

It has been a shock because investors have been conditioned to ignore the dips; or better still, to buy the foolish dips (BTFD) because time-after-time the dips reverse within a few weeks and the market plows onward and upward. In July last year, the market tumbled 3% and then fully recovered within four weeks.

This time is very different. Household 401Ks tumbled 10% and remain down after ten weeks – deeper and longer. That’s a big break from the normal routine. Another difference is that previous market drops had identifiable causes: a government sequester, a Greek bond collapse, and so on. Not this time, and that will create a lot more anxiety and uncertainty because without a clear reason for the collapse there can be no clear remedy.

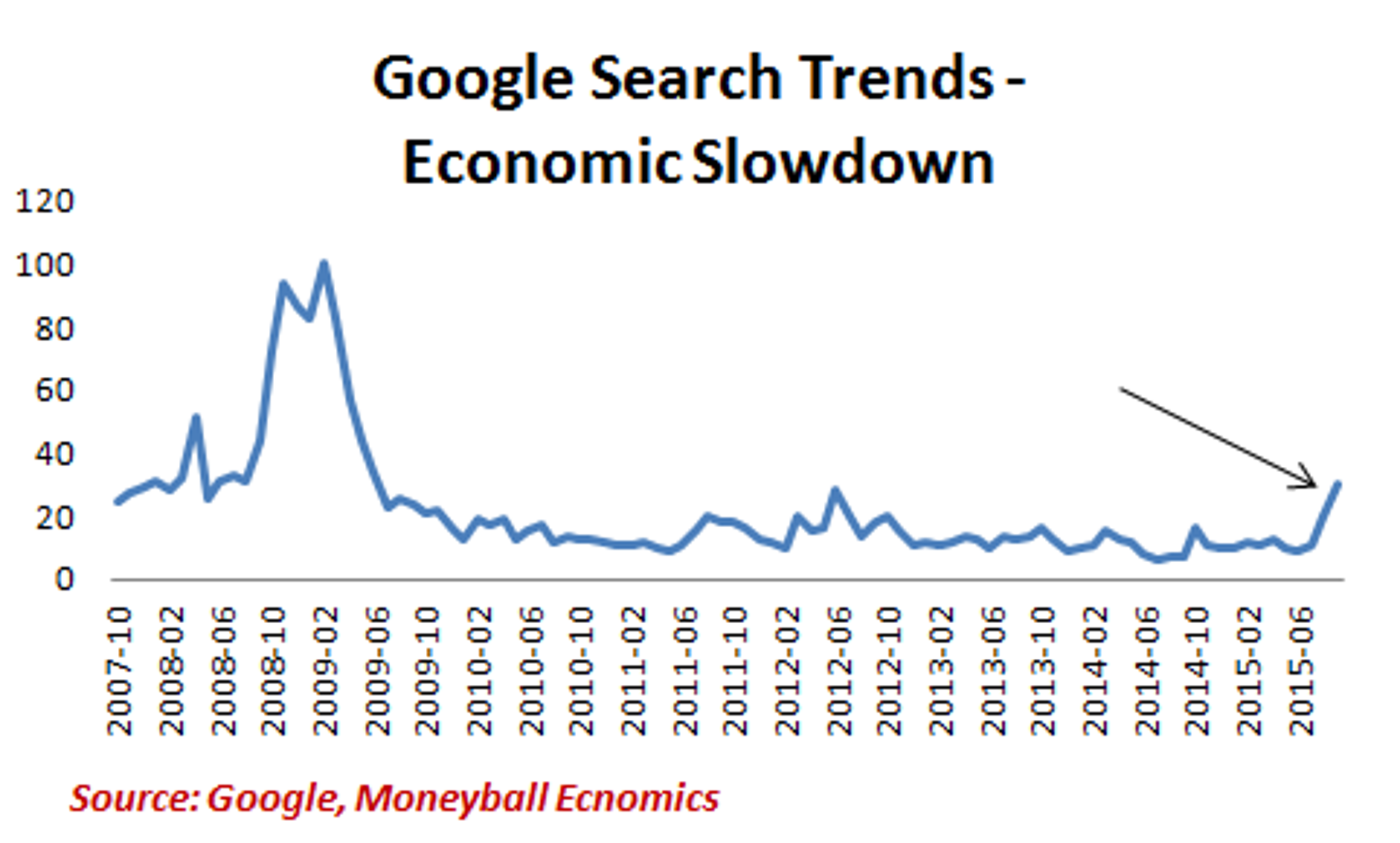

Investors are asking what’s wrong and they can’t help but notice reports of negative economic news, from a slump in payrolls to slowing factory production. From The Economist to USA Today, the media is discussing a global economic slowdown. Once it hits USA Today, Middle America is informed. Fears of a slowdown accompanied by a very real hit to household wealth will make US consumers defensive. We recently warned that consumers were very sensitive to the stock market and that it would definitely hit spending if it did not reverse quickly.

August Retail

Because of the conditioned response and the expectation that all would return to normal growth, the stock market tumble did not hold back consumer spending in August. September, on the other hand, is a much different beast. Suddenly economic slowdown is a very hot topic.

Holiday spending and travel are now at risk. The next few weeks are when travel and holiday shopping budgets are set. Those budgets aren’t typically funded by stock portfolios or 401Ks, but if households suspect that a falling equity market is signaling a recession is coming, then job security anxiety increases. They know from experience that after markets turn bearish, the next shoe to drop will be jobs. That leads to frugality and consumer spending retrenchment. It becomes a self-fulfilling cycle.

Is the stock market down because of an impending recession? I don’t think so. First, because the US economy is more stable than it appears, once we look past the problems in the energy and materials sectors. The economy is slowing and this cycle is long in the tooth. The second reason is the timing, suddenness and breadth of the drop. From July into September, all asset classes fell. Gold wasn’t a safe haven in the carnage – it fell from $1,200 to $1,100. We had a race to the exits as everyone ran to liquidate, and by everyone we mean banks and big investors. The trigger for the sudden run was the strong possibility of a Fed rate hike in mid-September.

Adding to the race for cash was China’s yuan devaluation. A lot of investments were backed by the yuan, so when it dropped in value, a lot of big investors had to cover their very big bets. That meant cashing out of other positions. It launched another liquidity fire sale.

How To Play It

If I’m right, then we have three waves converging:

- China Hard Landing: China has been on a super cycle of growth and it’s coming back down to Earth, but that slowdown hits a lot of countries that have been riding the China coattails – like Brazil, Australia, Germany, Saudi Arabia and so on. The governments have to cut back on spending or dip into their rainy day cash piles or both. Saudi Arabia, for example, has been cashing out tens of billions of dollars in stock market investments, adding to downward pressure in the markets.

- US Slowdown: We can’t ignore the impact of a slower global economy which slows US exports, but the bigger issue for the US economy is that it has rebounded and growth is slowing. We’ve returned to peak auto sales, factories have been upgraded, and problems of over-supply are making companies less willing to expand capacity.

- Fed Tightening: Last year, the Fed stopped throwing easy money into the market via Quantitative Easing. Now, in the seventh year of the recovery, the Fed is starting to talk about raising interest rates. The issue of raising rates is complicated. It slows the economy in various ways which tend to be bad for the stock market. (For example, the dollar gets more valuable, which hurts company profits. Also, the suddenly higher yields of bonds reduces the value of riskier investments like stocks.) However, rate hikes can also be positive because it signals the perception that the US economy is strong (or else why raise rates?).

At the September meeting, the Fed chose to leave rates alone and the markets interpreted the move as a signal that US economic growth is under threat.

I believe that the Fed will do anything to prop up the stock market. After spending trillions to do so, you don’t just walk away. Especially if things are fragile in the markets.

I suggest having a 60 day and a 180 day plan. Until recently, I’ve been preaching the sense of being in cash. Well, it’s time to change that position.

Get bullish for October and November. The stock market will rebound shortly – if only partially – for several reasons.

First it’s October, the start of a new quarter. September is typically a horrible month because institutional managers are closing books and re-balancing their portfolios. A lot of dogs are being dumped. October typically sees a surge as they re-enter the market.

Second, the rush to cash is essentially over. Investors have had six weeks to deal with the yuan devaluation and two weeks to handle the Fed rate decision.

Third, a decent earnings season is about to kick-off. Companies have hit the brakes on hiring and moved to cut costs. Plus they lowered the bar enough to easily jump over it.

Fourth, companies will use cash on share buybacks. If companies are seeing a more entrenched slowdown, then executives know that they have only a few paths to keep stock prices up. Executive and shareholder interests align at the stock price level – executive compensation is heavily tilted towards stock and stock options. Two great ways to get stock prices to move are (1) buying other companies (boosting revenues and EPS) and (2) share buybacks.

One final reason to expect more M&A is that corporate debt is very attractive when the stock market is in turmoil.

For the next 60 days, investment targets should be the most oversold sectors, like semiconductors and high tech. Oil is almost, but not quite bottoming. While oil prices are about as low as they are going to go and dividends look safe, some companies are over-leveraged and there will be some further pain.

We previously advised buying ETFs that were short Asia and emerging markets. The China bloodbath is far from over, but the risk is growing that many of these economies will devalue their currencies, which adds complexity to these investments. Pressure is building in countries like Korea to take major currency actions. In short, don’t go global at the moment.

Longer term, it’s smarter to be defensive and consider shifting into cash (i.e. money markets). We’ve been saying that all summer, and anyone listening made 10% in a few months simply by avoiding the market pullback. Or, as we get closer to December, you could shift some of your portfolio into ETFs that are short the market. Don’t do this now; as described above, there’s more probability of upside moves in the next 60 days. Look for an entry point towards the end of the year or even in early January.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.