Responds to Recent Announcement Regarding Changes in Staples Board Composition and Compensation Practices

Believes that the Best Way to Maximize Value for Staples' Shareholders is Through Exploring and Completing a Business Combination with Office Depot

Urges Staples to Immediately Retain Investment Bankers and Legal Advisors to Assist in Evaluating, Structuring and Executing Transaction with Office Depot

Believes Magnitude of Value Creation from a Staples/Office Depot Combination Far Exceeds Anything that Either Company Could Achieve on a Standalone Basis

NEW YORK, Jan. 20, 2015 /PRNewswire/ -- Starboard Value LP (together with its affiliates, "Starboard"), one of the largest shareholders of Staples, Inc. ("Staples" or the "Company") SPLS, today announced that it has delivered a letter to Ronald L. Sargent, Chairman and Chief Executive Officer of Staples, and the Board of Directors of Staples.

The full text of the letter follows:

January 20, 2015

Ronald L. Sargent

Chairman and Chief Executive Officer

Staples, Inc.

500 Staples Drive

Framingham, MA 01702

cc: Board of Directors

Dear Ron,

As you know, Starboard Value LP (together with its affiliates, "Starboard") is currently one of the largest shareholders of Staples, Inc. ("Staples" or the "Company"). We appreciate the dialogue that we have had with you and members of the Board of Directors (the "Board"). It had been our hope that we could continue these discussions privately. As such, we were surprised by your announcement last week regarding certain changes in Board composition, governance policies and compensation practices. While we appreciate that these are positive changes which address concerns that we and other shareholders have voiced to you, we are troubled by the timing of this announcement. At the Company's annual meeting held on June 2, 2014, the majority of Staples' shareholders voted for a proposal to separate the roles of Chairman and CEO and voted against approval of named executive officer compensation. We are disappointed that it took you more than seven months to respond to this clear mandate from shareholders, and question the motivation behind making these changes now. Furthermore, we are disappointed that these changes stop short of immediately appointing an independent Chairman, but rather provide a vague commitment to "appoint an independent Chair upon the succession of the current Chairman." The timing of your recent announcement certainly appears more characteristic of a company that is making advance preparations in furtherance of defending the status quo rather than one that is fully committed to evaluating and completing a compelling strategic combination, like the one we have suggested to you. We are therefore now compelled to reiterate for you and the Board our views regarding the future direction of Staples and to share these views with our fellow shareholders so that they, too, can engage with you regarding these topics.

As we discussed in our recent meeting, we believe that the best way to maximize value for Staples' shareholders is through exploring and completing a business combination with Office Depot. For a variety of reasons, we believe that now is the right time to pursue such a transaction, and we urge you to immediately retain a reputable investment bank and legal advisors to assist the Board in evaluating, structuring and executing a transaction with Office Depot.

We believe that a strategic combination of Staples and Office Depot would result in synergies that would more than double the operating profits of the combined company and would create an industry-leading office supply retailer that could more effectively compete against larger retailers and online competitors. The magnitude of value creation from such a business combination far exceeds anything that either company could achieve on a standalone basis.

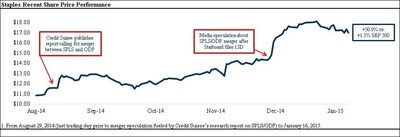

We believe that the evidence is clear that shareholders are broadly supportive of a transaction between Staples and Office Depot. As shown in the chart below, since the merger speculation began last September, Staples' share price has risen over 50%, strongly outperforming the S&P 500.

In addition, Wall Street research analysts have written numerous reports expressing their positive view of a Staples/Office Depot combination.

- "We believe that a merger of the remaining office supply superstore chains, Staples and Office Depot, makes significant financial and operational sense…the merger would create multiple years of earnings growth from synergies, reversing what has been a negative trajectory for Staples… Assuming a cash deal, we believe that the acquirer's stock, SPLS in our view, will more than double in two years…Given both our belief that this is the right strategic direction for SPLS to pursue and the limited downside we see in Staples' stock at its current valuation, we are upgrading SPLS to Outperform." – Credit Suisse (9/2/2014).

- "We are upgrading SPLS to Buy from Underperform and raising our price objective to $20 (from $10)…Beyond the prospect of compelling cost savings, we believe that both SPLS and ODP bring unique strengths that the other lacks that would be amplified as a combined entity…We believe store consolidation would be one of the most compelling aspects of a potential merger. While both ODP and SPLS are closing stores, we believe far more value would be created if they did it holistically and sooner rather than later." – Bank of America (12/12/2014).

- "We believe the possibility of a merger with the kind of upside we estimate bodes well for this stock in the near term…we view SPLS as now in play; hence, our upgrade to E/W and a new price target of $14.50 (up from $13)." – Morgan Stanley (12/12/2014).

- "…we like the idea of a combination since it would likely be more shareholder enhancing than what Staples could do on its own…There is no doubt that a merger between SPLS and ODP would yield large synergies, through accelerated store closings, increased purchasing power, corporate overhead and SG&A leverage, and distribution rationalization. Our initial rough estimate would get us to a synergy estimate of $1.5-$1.7 billion." – Jefferies (12/12/2014).

- "A SPLS / ODP merger would create a lot of value…In a case where SPLS & ODP come together, it's not hard to see the combined co. generate $2b+ of EBIT (~$1.5b as stand-alone co's + $500 m of net synergies), leading to ~$2 of EPS." – UBS (12/12/2014).

- "While a previous merger attempt between the two companies was blocked by the FTC in 1997, we believe a number of things have changed in recent years to make the combination more likely now…Potential ODP-SPLS Merger Synergies Could Create $6+ Billion in Shareholder Value…Assuming a combination of SPLS and ODP could yield a similar level of synergies, our pro forma 2015 revenue estimate of $37B would generate almost $1.5 in synergies from the deal. " – KeyBanc (12/12/2014).

After the recent increase in Staples' share price, we believe the stock now trades at a substantial premium to the intrinsic value of the standalone company. This results in a lower cost of capital for Staples and a stronger currency which could be used to acquire Office Depot.

If Staples fails to fully explore and consummate a transaction with Office Depot, shareholders will undoubtedly be extremely disappointed. Over the past two years, Staples management has pursued a standalone strategy which has resulted in a 31% decline in earnings per share. Without a combination with Office Depot, we would expect Staples' share price to decline to reflect the Company's standalone value. If this occurs, shareholders will be left then to evaluate Staples based only on its poor five-year share price performance, poor corporate governance, and excessive executive compensation, which were only slightly mitigated by your recent announcement.

|

Staples Historical Share Price Performance |

|||||||

|

Share Price Performance (1) |

|||||||

|

1 Year |

3 Year |

5 Year |

|||||

|

S&P 500 Index |

25% |

77% |

118% |

||||

|

Russell 1000 Consumer Discretionary Sector |

19% |

86% |

160% |

||||

|

Proxy Peer Group (2) |

19% |

94% |

163% |

||||

|

Office Depot |

21% |

102% |

(2%) |

||||

|

Staples |

(14%) |

(13%) |

(38%) |

||||

|

Underperformance vs. S&P 500 |

(39%) |

(90%) |

(156%) |

||||

|

Underperformance vs. Consumer Discretionary |

(32%) |

(99%) |

(198%) |

||||

|

Underperformance vs. Proxy Group |

(33%) |

(107%) |

(201%) |

||||

|

Underperformance vs. Office Depot |

(35%) |

(115%) |

(36%) |

||||

|

1. Total return as of 8/29/14 (last trading day prior to merger speculation fueled by Credit Suisse's research report on SPLS/ODP). |

|||||||

|

2. Proxy Group consists of companies used in the Company's proxy to set executive compensation |

|||||||

Since the filing of our initial Schedule 13D on December 11, 2014, we have met with and spoken to a number of large Staples shareholders and Wall Street research analysts who strongly, and without exception, corroborate our view that this merger makes too much sense to ignore. It is time for you to take action – engage advisors and work expeditiously with Office Depot to consummate a transaction. We understand that this will require cooperation from Office Depot, and we have already expressed to them our strong support for a transaction.

As one of Staples' largest shareholders, we have a strong interest in ensuring that you take the proper steps to maximize shareholder value. Our sincere hope is that we can continue to have a constructive dialogue. However, if it becomes clear to us that you have no intention of seriously pursuing this unique and highly attractive opportunity, it would be a clear sign that significant leadership change is needed at Staples.

Best Regards,

Jeffrey C. Smith

Managing Member

Starboard Value LP

About Starboard Value LP

Starboard Value LP is a New York-based investment adviser with a focused and differentiated fundamental approach to investing in publicly traded U.S. small cap companies. Starboard invests in deeply undervalued small cap companies and actively engages with management teams and boards of directors to identify and execute on opportunities to unlock value for the benefit of all shareholders.

Investor contacts:

Peter Feld, (212) 201-4878

Gavin Molinelli, (212) 201-4828

Tom Cusack, (212) 201-4814

www.starboardvalue.com

Photo - http://photos.prnewswire.com/prnh/20150120/170194

To view the original version on PR Newswire, visit:http://www.prnewswire.com/news-releases/starboard-releases-letter-to-staples-ceo-and-board-of-directors-300022852.html

SOURCE Starboard Value LP

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.