The following article originally appeared on Finbox.io.

Lincoln Electric Holdings, Inc. LECO is expected to report earnings on Tuesday, April 18th before the market opens. The stock's valuation is becoming stretched as shares have appreciated over 50% within the last year and currently trade near an all-time high.

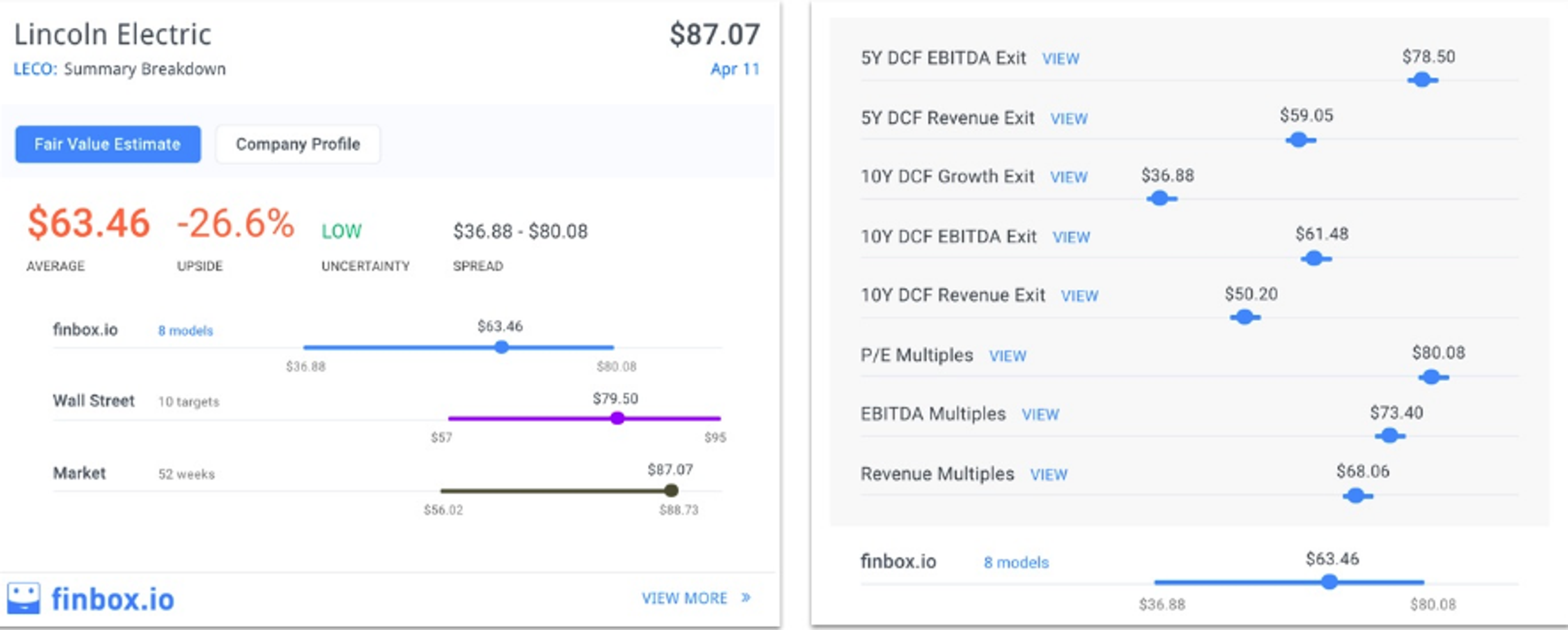

Finbox.io fair value data implies that the stock is approximately 25 percent overvalued. The estimate is calculated by applying Wall Street projections to eight separate valuation analyses as shown below. This compares to Wall Street's consensus price target of $79.50 implying nearly 10 percent downside.

The manufacturer and reseller of welding and cutting products has beat its earnings (EPS) estimates three out of the last four quarters. This positive trend suggests that the stock should be trading near its high. However, this is a misleading statement when analyzing the company's true operating performance.

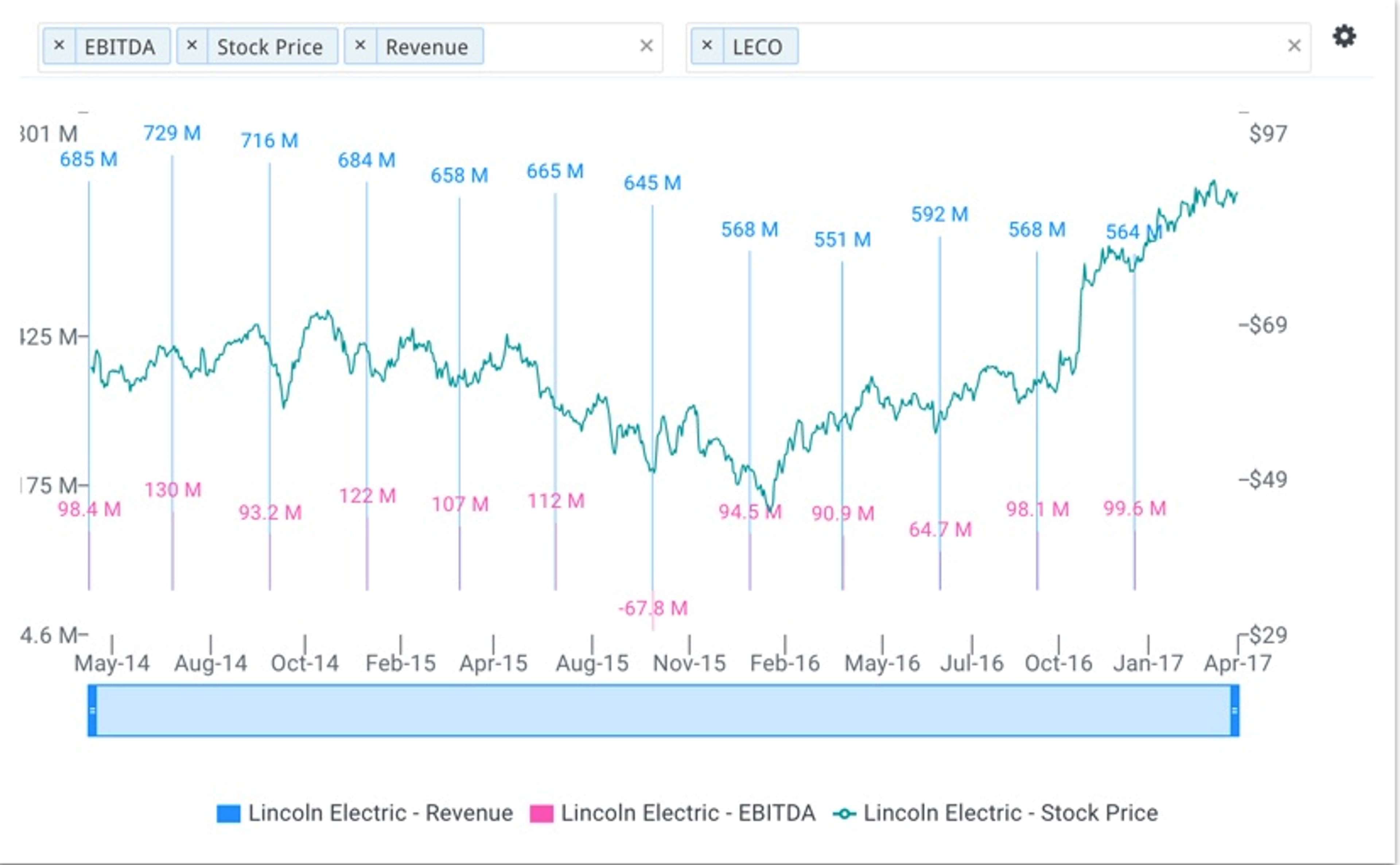

Lincoln Electric's revenue and EBITDA has generally declined over the last twelve quarters as shown in the chart below. In Q4'14, the company generated $122 million of EBITDA on $684 million of revenue. This is well above its Q4'16 EBITDA of $100 million on $564 million of revenue.

While financial performance has deteriorated, the stock has traded higher. Is it because Lincoln Electric is expected to outperform going forward?

Projected Performance vs Peers

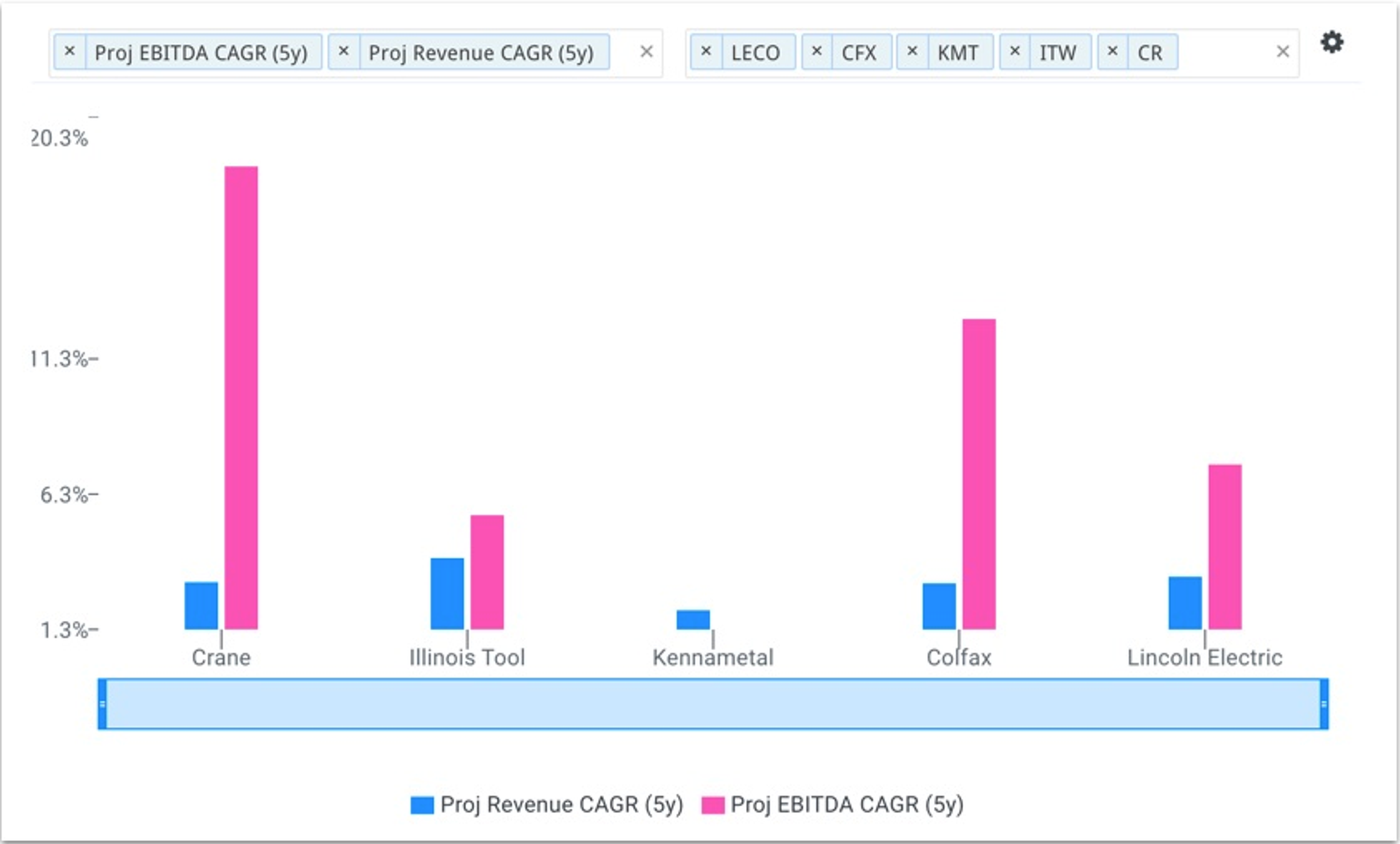

Lincoln Electric's projected revenue and EBITDA growth is middle-of-the-road when compared to its publicly traded peer group: Crane Co. CR, Colfax Corp CFX, Kennametal Inc. KMT and Illinois Tool Works Inc. ITW.

When applying Wall Street's consensus forecast for each company, Lincoln Electric's projected 5yr revenue CAGR of 3.3 percent is slightly above CR (3.1 percent), CFX (3.0 percent), KMT (2.0 percent) and below ITW (3.9 percent). Additionally, the company's projected 5yr EBITDA CAGR of 7.4 percent is only above ITW (5.5 percent) and below CR (18.4 percent) and CFX (12.8 percent).

Valuation Multiples vs Peers

Typically, higher growth stocks will trade at higher valuation multiples but this is not the case for Lincoln Electric. The company's projected growth is mediocre at best but trades at higher valuation multiples relative to its peers.

Lincoln Electric's forward EBITDA multiple of 14.8x is above all of the comparable companies: CR (9.3x), CFX (12.5x), KMT (13.2x) and ITW (13.6x). Furthermore, the company's forward P/E multiple of 25.2x is above CR (16.8x), CFX (24.4x) and ITW (21.4x) and only below KMT (28.5x).

According to S&P's CapitalIQ, Lincoln Electric's forward EBITDA and forward P/E multiple has averaged 10.3x and 17.7x over the last 5 years, respectively. That's a 4.5x EBITDA multiple expansion and a 7.5 P/E multiple expansion! The company's valuation has stretched to an unreasonable level which is not supported by underlying earnings and is getting ready to snap.

Shares May See A Correction Soon

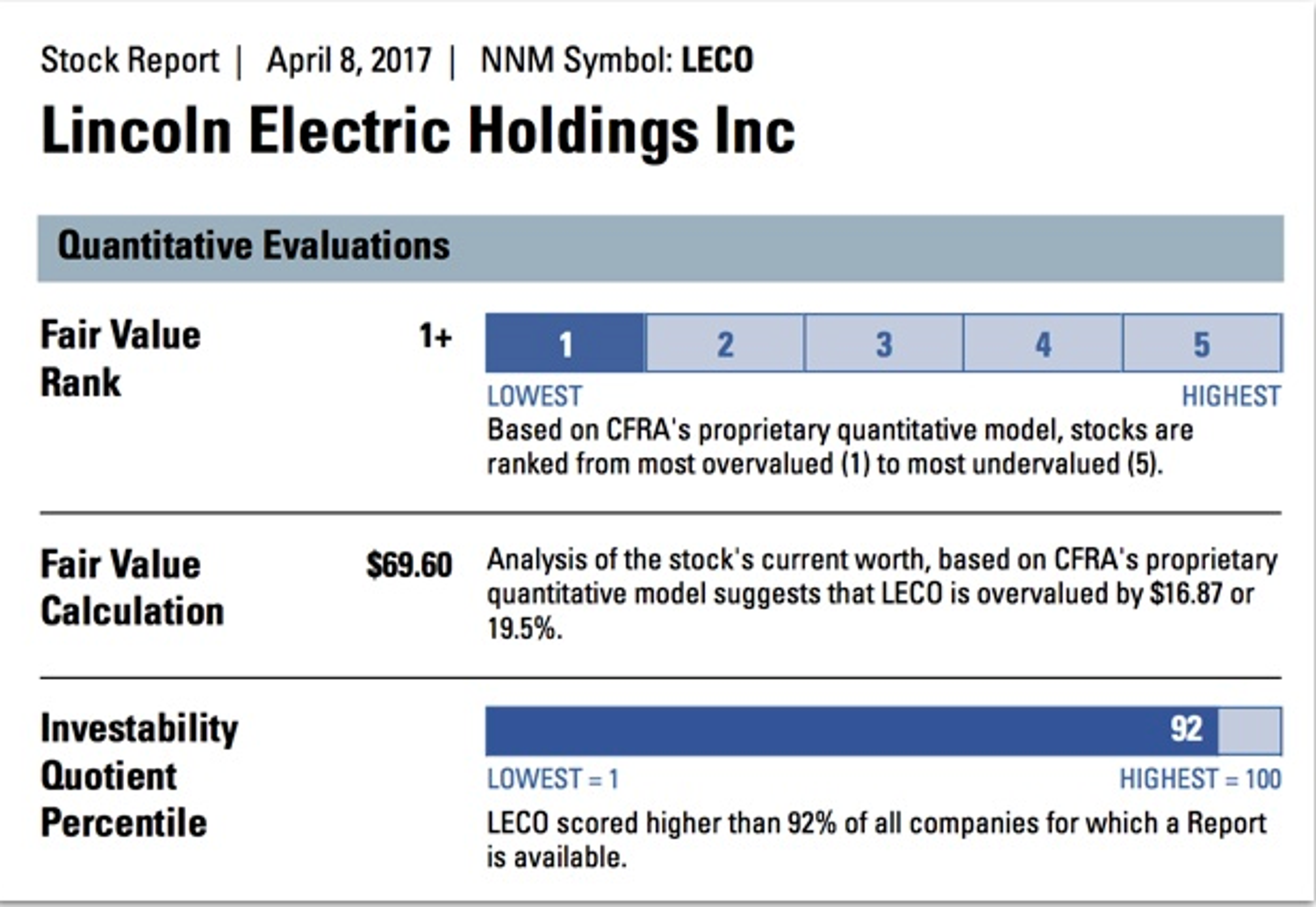

On April 8th, CFRA and S&P Global recommended that investors take profits and sell Lincoln Electric. The independent equity research firm gave the company its lowest fair value rank while suggesting the stock is 20 percent overvalued.

Finbox.io's valuation analyses imply that Lincoln Electric has even more downside purely on a fundamental basis. So what could be the catalyst that causes the stock to fall to a more reasonable level?

An earnings misstep might just do it. Value investors may want to stay clear of LECO before the company reports on Tuesday.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Date | ticker | name | Actual EPS | EPS Surprise | Actual Rev | Rev Surprise |

|---|

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.