After four of the most volatile days of the year, markets seem calmer Thursday as the July 4 holiday approaches, and trading could remain in a tight range.

When the markets close today, half the year will be over. And despite the huge swings back and forth over the last six months, stocks have barely moved from where they started.

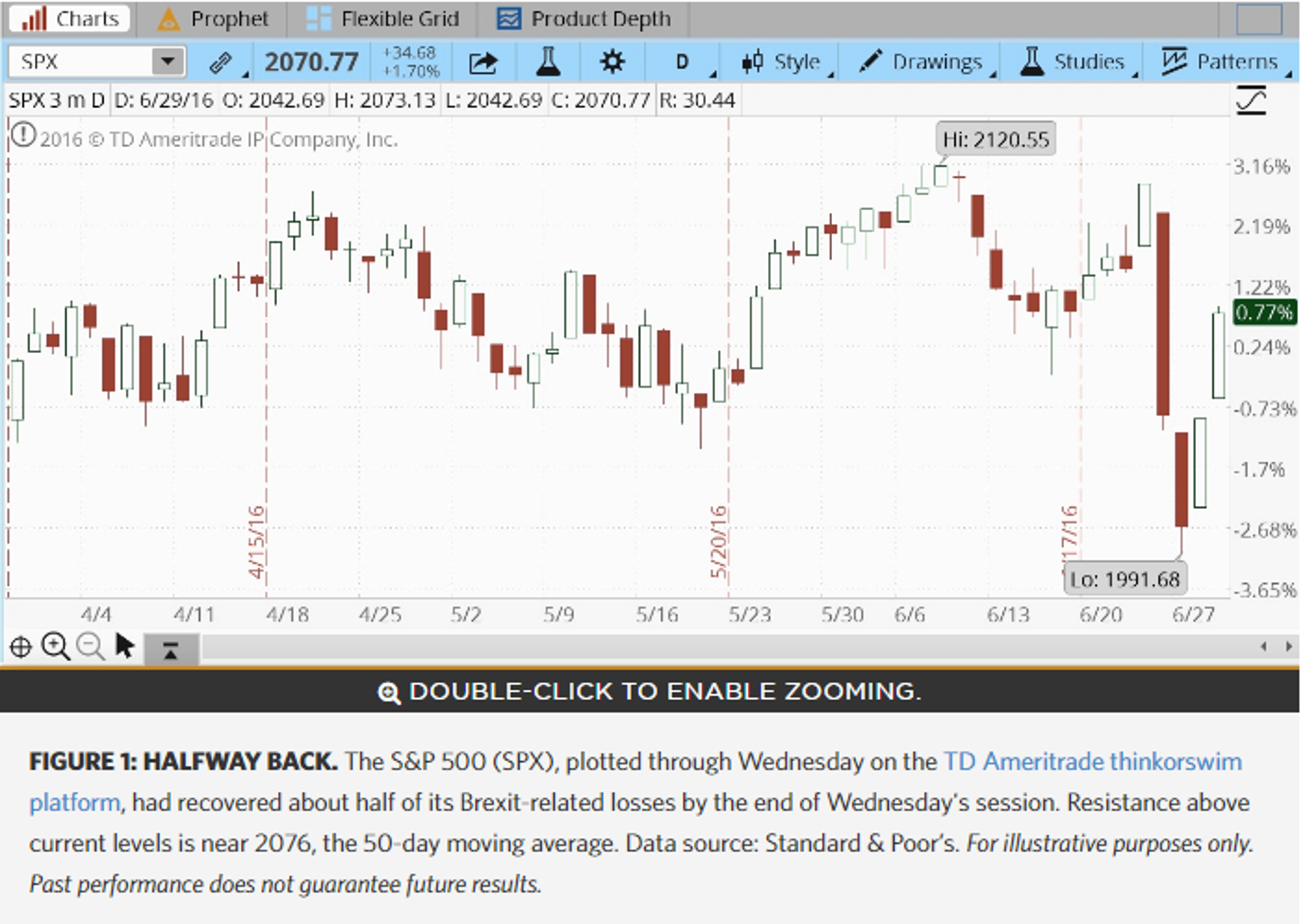

Going into Thursday, the S&P 500 Index (SPX) was up just about 0.1% year to date. Last week’s Brexit vote put the market into a tailspin with two of its worst days of the year. Then, Tuesday and Wednesday, the market had two of its best days of the year as many investors seem to have concluded that Brexit’s implications may be less drastic than previously thought.

When all is said and done, the SPX is down only about 2% from the highs it posted last week ahead of the Brexit vote. If it weren’t for the crazy way it got to its current level, it would just look like a mildly bad week. Typically, it takes about five days for an event like Brexit to work its way through the system, and this is day five. Now the SPX is back right in the middle of the 2050-2100 trading range it’s spent so much time in over the last few months.

Leading sectors Wednesday included financial (up 2.3%), health care (up 1.9%), and industrial (up 1.7%). As stocks recovered their Brexit losses, market volatility continued to ease, with the VIX index falling below 17. It peaked at around 25 shortly after the vote. The market has moved 1% or more five days in a row, but calmer waters appear to be ahead as the holiday approaches. The market could see holiday-type trading set in today, with some action the first couple hours but traders heading out for the weekend by later in the day.

Looking ahead, the July 4 U.S. Independence Day holiday looms on Monday, but things could get interesting immediately after that with the June jobs report scheduled for Friday, July 8, and earnings season getting into gear the following week. The Brexit vote won’t be reflected in this quarter's earnings, but even investors who’ve never listened to an earnings call might want to listen in this quarter to hear executives’ take on the vote and its potential effects. It could be interesting to see how CEOs paint the next six months to one-year outlook. Of particular note are companies that export a lot. Think of the big farm industry names, for instance.

St. Louis Fed President James Bullard is scheduled to speak in London at 2 p.m. ET today at a dinner for economists. This is the first time investors will hear from Bullard since Brexit, and it’s possible he’ll address that topic, especially considering he’s speaking at ground zero of the event, right in London. Recall that Bullard, even before Brexit, was making dovish prognostications, most recently in mid-June when he opined that only one rate hike would be needed through 2018. At that time, he said he saw continued light U.S. economic growth of around 2%, and little inflation risk.

In a positive development for the financial sector, all but three of the 33 largest U.S. banks got permission Wednesday from regulators to return profits to investors, as the Federal Reserve released the final results of its 2016 “stress tests.” Most banks passed the stress tests with relative ease, and now have the ability to appeal more to investors through dividends and share buybacks, a potential boost for the sector. Both Bank of America Corp BAC and Citigroup Inc C announced dividend hikes and stock buybacks in the wake of the stress test results.

Though the real earnings season remains a couple of weeks away, a few companies report this week, including Darden Restaurants, Inc. DRI, which early Thursday posted fiscal Q4 earnings per share that slightly beat analysts’ consensus estimate, though sales were a touch lower than expected. The company’s full-year earnings guidance was also a bit below analysts’ expectations. The restaurant sector is one that bears watching, because restaurant visits are typically among the first thing people cut back on during rough economic times.

Weekly jobless claims Thursday came in at 268,000, right around expectations.

Overseas, the German bund yield remains negative despite some recovery in U.S. Treasury yields late Wednesday.

Bond Market Stays Hot Even as Stocks Recover: Strength in the bond market over the last two days despite huge gains in stocks lends an air of confusion. The U.S. 10-year Treasury bond yield spent much of Wednesday below 1.5%, near the lows it set immediately after the Brexit vote last week, even as the SPX rose about 70 points from its lows. There was a slight recovery back to 1.5% by the day’s end. Typically, bonds fall and yields tend to rise during a stock market rally, but that hasn’t been the case the last couple of days. The market appears to be undergoing a re-pricing process, especially for financials, which could possibly be leading to this dichotomy. But the continued strength in bonds also could point to a stocks rally that may lack long-term strength, because many investors still appear to be choosing safety over risk.

Would Anyone Miss 16,000 Barrels of Oil? Nah! Initially, oil fell with other commodities and equity markets after the Brexit vote, but oil recovered even more quickly than the rest of the market and U.S. crude futures neared the $50 mark in Wednesday trading. Part of the rally was simply average, everyday stuff, like a potential strike among oil workers in Norway and a larger than expected weekly U.S. oil draw. Analysts also did the math on the potential impact of Brexit on British oil demand, and the results weren’t too dramatic. One analyst calculated that a potential slowdown in the British economy due to Brexit would lead to a drop in oil demand of about 16,000 barrels a day. For comparison, the world uses about 94 million barrels of oil daily. How does 16,000 compare to 94 million? A trip of 16,000 miles wouldn’t even take you around the world. A trip of 94 million miles would put you slightly past the sun.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Date | ticker | name | Actual EPS | EPS Surprise | Actual Rev | Rev Surprise |

|---|

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.