The fresh sanctions include banning banking transfers against 25 Iranians and companies that reportedly assisted in Iran's missile program.

Deal's History

The Iran nuclear deal was a preliminary agreement reached in 2015 between Iran and the P5+1 world powers, with P5 standing for the five permanent members of the U.N. Security Council and the "+1" referring to the European Union. The deal called for Iran reducing its nuclear facilities and accepting additional protocol and in turn, economic sanctions against it were to be lifted. Following the agreement, sanctions were lifted in January 2016, as Iran kept up its end of the bargain.

The lifting of sanctions meant freeing up of tens of billions of dollars in oil revenue and frozen assets. However, analysts point out that by the missile testing, Iran has not violated the accord, which does not touch upon Iran's liaison with terror groups or its missile testing.

That said, the development was adequate to trigger a series of reactions from both sides. Trump, with his tweetstorms, and his administration turned the heat on Iran even as Iran retaliated with caustic statements of its own.

Now what does all this mean for the oil market?

Supply Glut Leads To Production Cuts

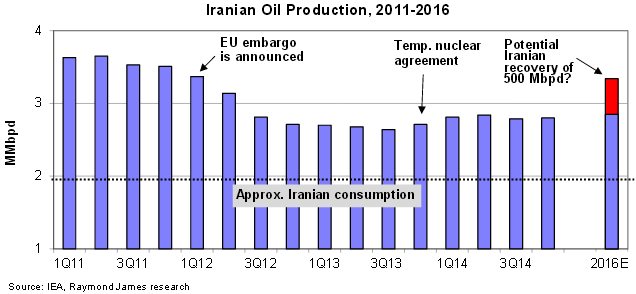

A Forbes article suggests that Iran has the second largest proved crude oil reserve base in the Middle East. It is currently the third largest among the OPEC oil producers.

Since sanctions were lifted in January 2016, Iranian oil exports have nearly doubled. By virtue of the deal, Iran was also able to negotiate trade and investment deals. With Iranian oil coming online, oil prices went into a downward spiral in early 2016. In a bid to arrest the slide in prices, OPEC members and Russia agreed for a production cut in November last, with the accord having come after severe infighting among Saudi Arabia, Iran and Iraq. Finally, OPEC agreed to cut output by 1.2 million barrels per day by January 2017.

Iran was producing more than 3.8 million barrels of oil per day in late 2016 ahead of the production quota freeze, although it did suggest that it would work towards improving production to pre-sanction levels or over 4 million barrels per day. The OPEC deal exempted Iran from the production quota.

Handicapped By Weak Investment Climate

That said, the chances of Iran increasing production beyond current levels are remote, as it is currently operating at full throttle. Any increase beyond this, would require billions of dollars in investment. A FT report suggested that Iran might need to $200 billion in investment to revive its antiquated energy sector over the next five years.

Oil companies, which stayed away from Iran, slowly began to troop in after the sanctions were lifted. A consortium led by French oil giant Total SA (ADR) TOT signed an agreement in November 2016 to develop part of the giant South Pars gasfield.

Will Iran Flex Its Muscles?

Analysts do not see oil prices being boosted by the skirmish between Iran and the U.S. prices may not react much to the recent tensions unless Iran opts to block oil transport via the Strait of Hormuz, which could mean stalling of the bulk of the OPEC oil supply.

According to the Energy Information Administration, about 35 percent of all seaborne traded oil and almost 20 percent of oil traded worldwide goes through the strait, with Asian nations receiving 85 percent of the supply. The agency sees substantial increase in oil prices if there is blockage of the strait.

The sanctions imposed by the United States do not mean that the Iranian nuclear deal would be dismantled, as it would require the concurrence of the other parties involved in the deal. China, which has seen its animosity with the United States reach new levels since Trump's election victory, is unlikely to take sides with the United States.

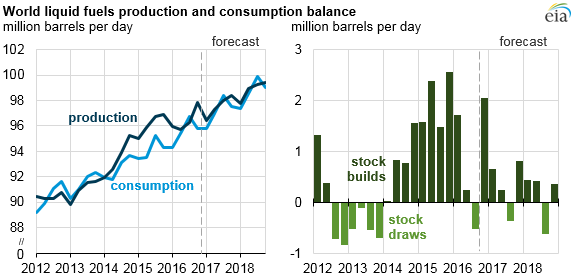

The demand side of the equation and the dollar's move also have an impact on oil prices apart from supply side factors. Given that the economic recovery post the financial crisis can best be termed as lukewarm, global oil demand could stay depressed. However, EIA said in a release in January that consumption growth would being to outpace supply growth in 2018, leading to tightening of global balance.

That apart, the Fed's tightening cycle that had rendered the dollar attractive has also proved bearish for oil prices. Since oil is dollar-denominated, oil and the greenback share an inverse relationship.

The oil market dynamics, therefore, is unlikely to see any meaningful change from the souring of relations between Iran and the United States. This has been reflected in the price of crude oil futures. After rising modestly last Friday, crude oil futures were down 1.56 percent on Monday.

At time of writing, United States Oil Fund LP (ETF) USO was sliding 1.39 percent to 11.38.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.