The U.S. consumer remains under the microscope today after Thursday’s tepid retail sales data, with a key inflation reading coming in higher than expected.

The Consumer Price Index (CPI) for August came out early Friday and surpassed expectations at 0.2%, compared with the consensus among Wall Street analysts for a 0.1% rise. Growth in CPI came amid increased housing and medical costs, the government said, and core inflation, which strips out food and energy, rose 0.3%.

Higher CPI can often be a positive sign, as it typically shows growing demand for goods. And remember, the Fed watches inflation data very closely, with a stated goal of 2% annual inflation, and this is one of the last data points the Fed sees before going into its meeting next week. Core CPI is now up 2.3% over the last year, but it’s also worth noting that inflation-adjusted wages are up just 1.3% during that time, the government said.

Also due this morning is University of Michigan consumer sentiment for August, another number that can often reveal underlying economic strength when it goes up. Consensus among analysts is for a reading of 91.5, up from below 90 in the previous report, according to Briefing.com.

The focus on consumers began Thursday, when some of the market strength might have been a reaction to bearish retail sales data early in the day that helped drive down remaining expectations for a September Fed rate hike. Fed funds futures at the CME Group predict just a 12% chance of a September hike, down from above 30% earlier this month. Futures prices still show a better than 40% chance of a December Fed hike, and that would come a year after the Fed last raised rates.

Despite what appear to be falling chances of a rate increase at the Fed’s meeting next Tuesday and Wednesday, the bond market has been falling the last few days. Yields on the benchmark 10-Year U.S. Treasury note climbed to 1.74% during the session Thursday, the highest level since late June, before falling late in the day back below 1.7%. Many analysts see 1.75% as a technical resistance level for yields on the 10-year. Yields move in the opposite direction of bond prices.

Also, traders seem to be preparing for the Fed’s statement Wednesday afternoon. Even if there’s no rate rise, it’s possible the statement could contain more hawkish language about the future, especially considering some of the more hawkish remarks made recently by a number of Fed officials. Any change in the language from last time should be closely watched. In the meantime, between now and next Wednesday trading in the markets may be characterized by risk avoidance.

The oil market, a source of pressure on equities earlier this week, perked up a little on Thursday, with focus centering around the shutdown of a U.S. gasoline pipeline and news that a major Midwest refinery will undergo repairs. This is typically a season of falling demand for gasoline in the U.S., and one in which refinery maintenance often takes place. Such maintenance can reduce demand for crude oil, pressuring prices. U.S. futures prices closed below $44 a barrel, which is seen as a technical resistance area. Futures were lower early Friday as worries about a possible supply glut persisted. Weekly U.S. rig count data is due later today. Last week’s rig count was the highest since February.

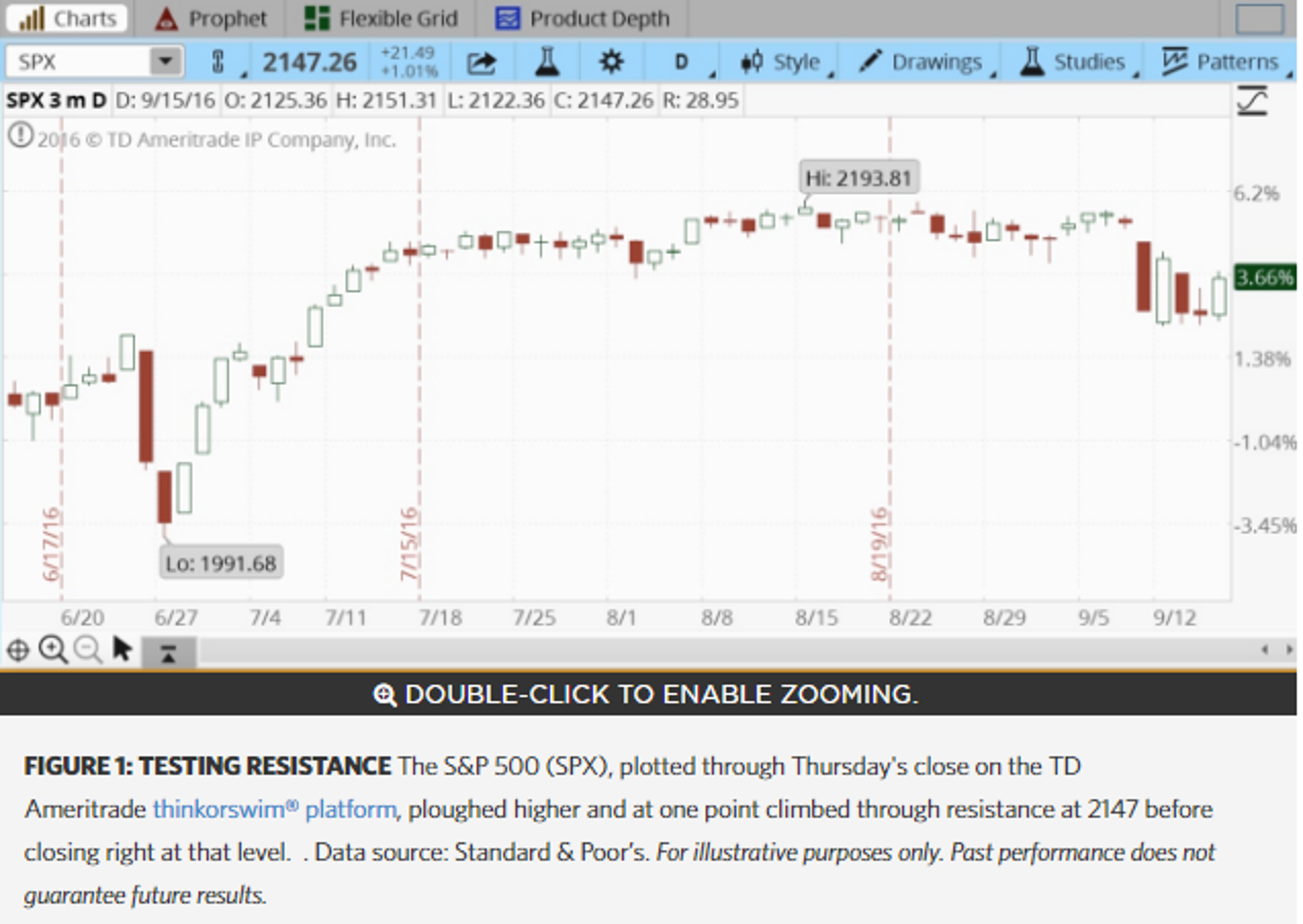

The S&P 500 Index (SPX) had faced technical resistance at 2147 going into Thursday’s session, and managed to trade above that level for part of the day before falling to settle right at 2147.

This is typically a quiet time of year for earnings, but one big company, Oracle Corporation ORCL did report fiscal Q1 results after Thursday’s close. Earnings rose 5%, with cloud computing giving the company’s finances a boost. But shares fell in after-hours trade because both earnings and revenue missed Wall Street’s expectations. Oracle reported after-items earnings of 55 cents and revenue of $8.6 billion. Consensus among Wall Street analysts was for earnings of 58 cents on revenue of $8.7 billion.

Looking for Bullish Data? Keep Looking: Retail sales released early Thursday disappointed, showing a 0.3% drop in August compared with analysts’ consensus expectations for a drop of 0.1%. The weakness ran across various retail sectors, including autos, gas stations, department stores and even online stores. Anyone hoping the government would put out something more positive later in the day Thursday was probably disappointed, as two more important data points also came in below expectations. Industrial production fell 0.4%, compared with analyst expectations for a 0.3% drop; and business inventories were flat, compared with expectations for a rise of 0.1%. Overall, the recent data paint a picture of an economy that’s sputtering along, and some analysts are starting to wonder if the consumer, who put a charge into parts of the economy earlier this year with robust buying of automobiles and big-ticket household items, may be losing steam. There’s even talk that people may be putting off big purchases until after the U.S. election in November, though that’s purely speculation.

Apple Seeds: The information technology sector has been outpacing the broader market this week, and is up nearly 8% over the last three months compared with just a 1.4% rise for the S&P 500 Index (SPX). Recent strength in the biggest stock of the sector, Apple Inc AAPL, may be greasing the skids for other sector stocks as well, analysts say. But there may be more to it than just AAPL’s influence. Safe haven stocks like utilities and consumer staples have begun to look pricey after months of investors flocking to these sectors to find yield. Partly as a result, investors may be looking at sectors like information technology where they think their money may go further. Utilities remain up nearly 12% year to date, but are down 3.4% over the last three months. Consumer staples are up about 4% year to date but down more than 2% over the last three months. Is it possible to pinpoint the money going directly out of some sectors and into others? Not really, but the sector performance numbers do seem to support the theory that investors are looking for new places to put their money after long rallies in safety stocks.

Inclusion of specific security names in this commentary does not constitute a recommendation from TD Ameritrade to buy, sell, or hold.

Market volatility, volume, and system availability may delay account access and trade executions.

Past performance of a security or strategy does not guarantee future results or success.

Options are not suitable for all investors as the special risks inherent to options trading may expose investors to potentially rapid and substantial losses. Options trading subject to TD Ameritrade review and approval. Please read Characteristics and Risks of Standardized Options before investing in options.

Supporting documentation for any claims, comparisons, statistics, or other technical data will be supplied upon request.

The information is not intended to be investment advice or construed as a recommendation or endorsement of any particular investment or investment strategy, and is for illustrative purposes only. Be sure to understand all risks involved with each strategy, including commission costs, before attempting to place any trade. Clients must consider all relevant risk factors, including their own personal financial situations, before trading

TD Ameritrade, Inc., member FINRA/SIPC. TD Ameritrade is a trademark jointly owned by TD Ameritrade IP Company, Inc. and The Toronto-Dominion Bank. © 2016 TD Ameritrade IP Company, Inc. All rights reserved. Used with permission.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.