Friday’s blowout jobs report gave the market some positive momentum heading into a big week. But can the rally continue?

This is where things get interesting. That’s because it now seems clear that the terrible May jobs report was an anomaly, not a trend. Looking ahead to the coming week, the start of earnings season and the all-important July 15 monthly retail sales data could provide investors a sense of how those job gains are filtering through the broader economy, and play a part in determining whether this rally lasts or fizzles out.

Retail sales, which rose a strong 0.5% in May, could really provide a vote of confidence if they once again show consumers pulling out their wallets in a big way. When combined with consumer price index (CPI) data, also due Friday, and what earnings data tell investors in terms of same-store sales, it could give a very good picture of where the consumer stands on the heels of this jobs report. For stock market bulls, it would be nice to see stronger retail sales, housing sales, and auto sales in the wake of the jobs data.

The big number in the jobs report was the headline number, which showed 287,000 jobs created in June, more than 100,000 above consensus and blowing the May report out of the water. This one report, of course, doesn’t mean the economy is free and clear, just as the May report didn’t signal imminent recession. But the great thing about the report is where it showed jobs being created, in areas like business-to-business services and health care, places where people can build careers, not just jobs. That’s positive longer-term, because when more people embark on careers, they can afford to buy homes, cars, and other big-ticket items that help the economy grow.

What’s the job report’s impact on the Fed? Not necessarily much. One data point doesn’t change the outlook, and the Fed has said it plans to look at the numbers going forward. Fed officials radiated caution going into the jobs report, and probably need to see a lot more data before they change their tune. Futures markets continue to show no chance of a July rate hike, though chances of a September hike edged up to 12% by midday Friday. The chance for a rate cut, which futures priced in before the jobs report, is off the table, at least for the moment. Remember, despite signs of a stronger U.S. economy, overseas jitters continue to play a big role in market psychology, and the Fed has said it’s closely watching developments abroad.

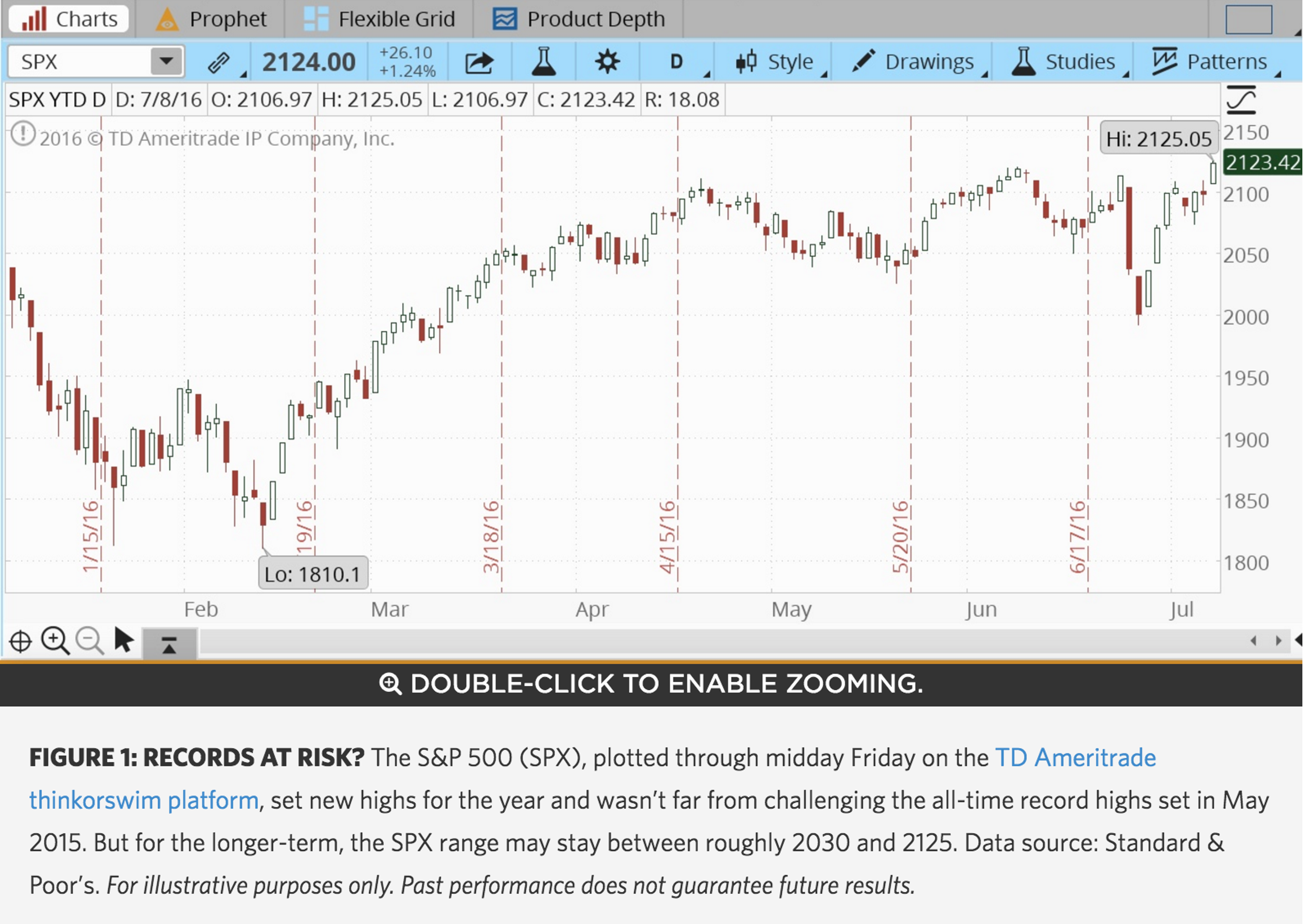

The stock market jumped to new highs for 2016 after the jobs report, and could again challenge all-time highs at the 2130 level. In the stock market, beaten-down financials were the big leaders on Friday, putting up gains of more than 1.6% by midday. Industrials and consumer discretionary names also rallied.

This all sets things up for the coming week, with some of the big financial names like Citigroup Inc C and Wells Fargo & Co WFC scheduled to report earnings Friday. It could be one of the more interesting earnings seasons in a while, namely because CEOs will have to take questions from analysts about how Brexit might affect forward earnings. What’s so hard about that? The United Kingdom hasn’t even chosen its next prime minister, and CEOs will be asked to forecast what the UK’s policies might be. Pay a lot of attention to those companies that have business in the UK, and see if they deliver a sense of how that could affect their businesses going forward. As for the financial sector earnings themselves, it seems logical to expect the same pattern of slow growth seen in recent quarters, with companies beating lower numbers. But the CEO statements could become really important.

In other markets as of midday Friday, the dollar rose against the euro, putting more pressure on commodities like oil, and bonds continued their rally. With no interest rate hikes in sight even in the aftermath of this strong jobs data, investors apparently didn’t see any reason to sell bonds.

Bonds Stay Strong Despite Jobs Report: Some may have expected investors to take profit on the sky-high U.S. bond market in the wake of Friday’s strong jobs report, but as of midday Friday, that wasn’t the case. The U.S. 10-year Treasury bond yield was still trading below 1.4%, not far off the record lows it had scored earlier in the week. Investors still seem to want safety, and Friday’s action, with the rally in stocks, indicated that investors want to own both stocks and bonds. This safety focus may reflect lingering concerns about the U.S. economy, or fears of after-shocks from Brexit. With government bond yields so low, the trend toward dividend stocks could continue as investors seek yield. At this point, even some sectors not known for being dividend plays, like technology, are yielding higher than 10-year bonds.

Home Still on The Range: Jobs report or not, it seems unlikely that the stock market is going to break far out of the current range, with support down around 2030 and resistance at about 2125. Why? For one thing, there’s uncertainty ahead as the U.S. Presidential election approaches. Investors may not want to get positioned too aggressively one way or the other ahead of the vote. Also, rallies may be hard to sustain as long as the current low interest rate environment prevails. That’s because the low rates weigh on the key financial sector, and it could be challenging to stage a major rally without that sector’s vigorous participation. So it’s hard to see the market breaking out of the 2030-2125 range, at least in the short term.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.