If you're like most Americans, you probably had to take out student loans to pay for your college education.

Student loan debt has reached epidemic proportions; 45 million Americans collectively owe about $1.7 trillion in student loan debt, and many young adults are putting off buying a home, saving for retirement or starting a family so they can tackle their student debt first. However, with the right plan and focused saving, even those who feel like they’re drowning in debt can escape and start working toward other goals.

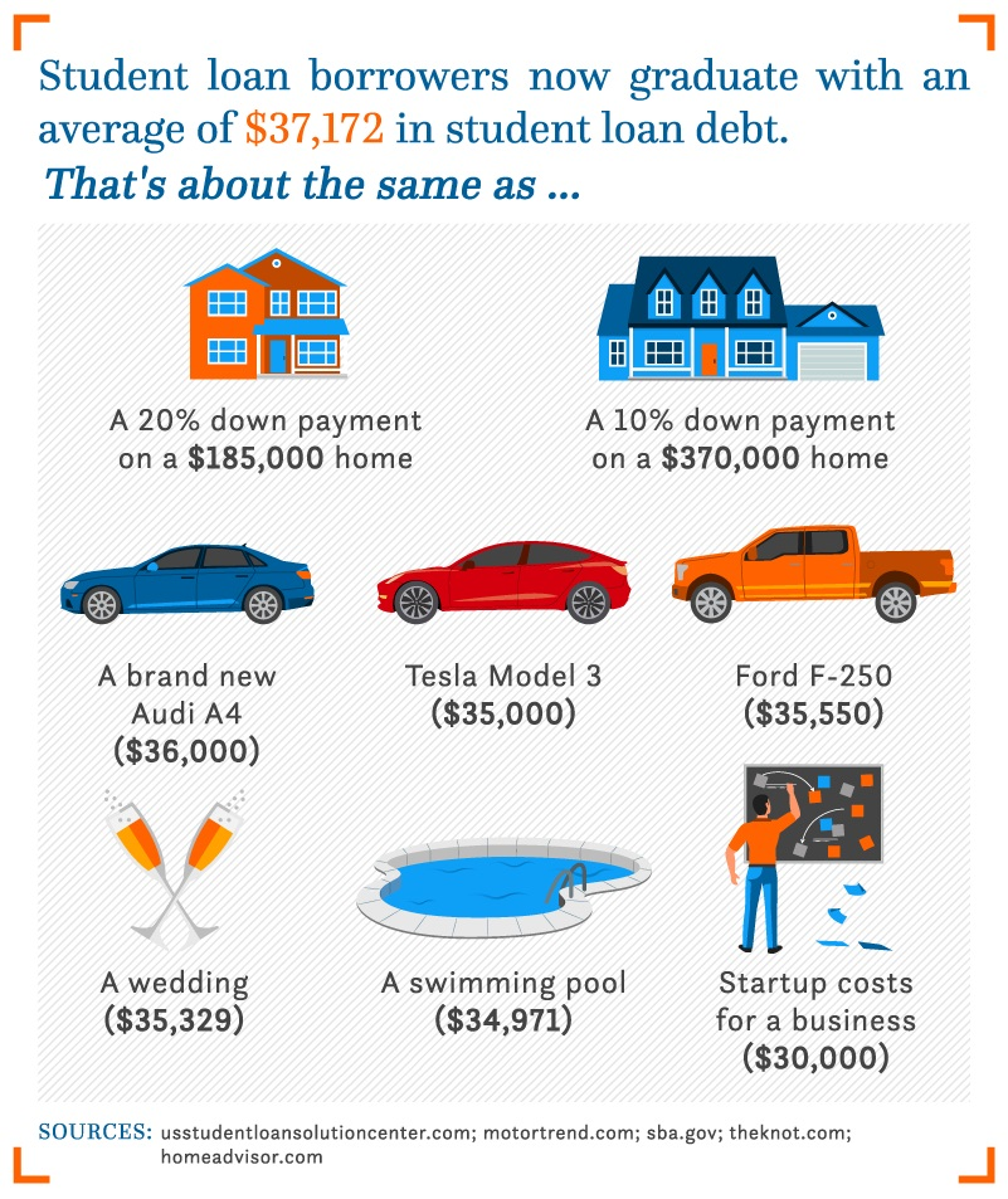

Overview: Student Loan Debt

According to data reported by CNBC, about 70 percent of students graduate college with “excessive debt.” Though a federal student loans’ standard repayment plan lasts ten years, the reality is that most students will take significantly longer to pay back their loans, averaging about 19.7 years for a bachelor’s degree and 23 years for a graduate degree.

When they graduate, the average worker will have about $37,172 in loan debt — about $20,000 more than the average student who graduated 10 to 12 years ago. In fact, the Federal Reserve estimates that the average monthly student loan payment increased from $227 in 2005 to $393 in 2021.

Despite the known challenges of paying back loans, more and more Americans continue to hit the books and head back to school to meet the increasing educational requirements of the current labor market. According to data from the Brown Center on Education Policy, "roughly one-quarter of the increase in student debt since 1989 can be directly attributed to Americans obtaining more education."

Ready to declare bankruptcy to discharge your excessive student loan debt and finally escape that compounding interest? Not so fast. Most student loan debts are not dischargeable under both Chapter 7 and Chapter 13 bankruptcy statutes.

Method 1: Start Paying While You’re Still in College

Okay, you probably won’t be able to pay the entirety of your $40,000 loan with your after-class, work-study job or waiting tables on the weekends.

However, many students underestimate the power that they have while in college to reduce what they owe in the long term because they're not interested in how to pay for college until after they graduate. If you have subsidized federal loans, your student loan payments aren’t due and don’t accumulate interest until you graduate, leave school or your enrollment drops below part-time credit requirements.

Many federal loans also offer a grace period of six months after you graduate or leave school before they begin to accumulate interest.

Pay down as much of your debt as you can while you are still in school or in your grace period to reduce your principal balance — meaning that when your loans start to accumulate interest, there will be a lower balance for them to accumulate on.

Pay down your interest as much as possible to help avoid compounding interest (interest accrued on unpaid interest). In effect, you will pay less over time than you would if you put off your payments until you graduate.

Set up automatic monthly interest payments from your savings accounts to avoid accumulating late fees and charges because you forgot about the payment. To learn more about how to set up automatic payments, start by checking out this article on how to set up direct deposit and debits.

Method 2: Use the Debt Snowball Method

The debt snowball method is a debt repayment plan that can be useful if you have multiple student loans.

Like a snowball that accumulates mass as it rolls down a hill, the debt snowball method prioritizes paying down your smallest loans first and building up to paying down larger loans.

To start the debt snowball method, use the following steps:

- List all of your debts in ascending order, beginning with your smallest debt and work your way up to your largest debt. If two debts are very close in size, list the debt with the highest interest rate first.

- Commit to paying the minimum balance on all of your loans and divert all excess cash to your smallest balance.

- As soon as your smallest loan has been paid in full, continue onto the next smallest loan. Continue to pay the minimum balance on all your outstanding loans and divert your excess income to the second smallest loan, then the third, then the fourth.

- Repeat this process until all your loans have been paid in full.

The debt snowball method lists debts in order of principal amount instead of interest percentage. This means that you may end up paying slightly more over time when using the snowball method because your largest loan may also have the highest interest rate and get paid off last.

However, if you’re the type of person that needs to see that you’re making progress towards eliminating your debts in order to stay motivated, the debt snowball method might be worth the extra interest.

Method 3: Use the Debt Avalanche Method

The debt avalanche method means you’ll pay off your loans in order of interest amount instead of debt size. To use the debt avalanche method, take the following steps:

- List all your debts in ascending order, beginning with loans that have the largest interest percentage. If you have two loans with the same interest percentage, list the smaller debt first.

- Commit to paying the minimum balance on all your loans and divert all excess cash to the loan with the highest interest rate.

- As soon as your highest interest loan has been paid in full, continue onto the loan with the next highest rate. Continue to pay the minimum balance on all your outstanding loans and divert excess income to the next highest interest rate.

- Repeat this process until all your loans have been paid in full.

Unlike the debt snowball method, the debt avalanche method prioritizes your loans by interest amount and allows you to accumulate less interest over time. Loan servicers like Great Lakes automatically employ the debt avalanche method unless you specify that you’d like to pay down a certain loan first.

The debt avalanche method may save you money, but if you know that seeing those “paid-in-full” emails will keep you more motivated to continue paying your loans, you may want to consider choosing the debt snowball method instead.

Method 4: Consolidate Your Loans

If you have multiple federal loans, you might consider combining them with a direct consolidation loan, which takes multiple loans and combines them into a single loan with one monthly payment.

You are eligible to consolidate your loans as soon as you graduate, leave school, or drop below part-time enrollment. Private education loans are not eligible for the direct consolidation loan program. Direct consolidation loans can be useful if you have multiple federal loans with different servicers and need to simplify your loan repayment process.

Consolidation can lower your monthly payment by giving you more time to pay back your debts; some students can be granted up to an additional 30 years to repay. Unfortunately, there are a few drawbacks to loan consolidation.

If you consolidate your loans, you end up paying more in interest because you spread your debts over a longer time period. Any outstanding interest on the loans will automatically become a part of your new loan’s principal amount, which means that depending on the original interest rate on the account, you may end up paying a more interest after consolidation.

If you are on an income-driven repayment plan, consolidating your loans may cause you to lose your benefits under the Public Service Loan Forgiveness program. You should only consider consolidating your loans if you are sure that the consolidated interest rate is lower than your current interest rate and/or you have so many loans that they’re unmanageable.

Method 5: Access Home Equity With Unlock

As you plan to pay off student loans, you may also want to access your home’s equity. But, when you use Unlock, you get an investment in your home that you don’t need to pay back until the house sells. So, it isn’t a loan—it’s much better. The platform accepts credit scores as low as 500, and you can reach out right now to learn if you qualify and how the process works. In this way, you can pay off student debt and stop worrying about those payments.

Final Thoughts

After you’ve chosen a debt repayment plan, it’s time to adjust your budget and/or your spending behavior so you can put as much money as possible towards your loans.

Use a budgeting app like Mint to help you analyze your spending and find places where you can save. Even if you are still in college, it’s never too early to create and stick to a budget.

Lend-Grow

Lend-Grow offers 5-, 10-, 15-, 20- and 25-year student loan refinance terms with fixed rates as low as 2.80% APR and variable rates as low as 1.89% APR.

Lend-Grow pays down your loan, too — 0.10% APR every month for 3 years! Here’s what this means: Lend-Grow deposits 0.10% APR of your loan amount funded each month for up to 3 years (as long as your account is active) with payback rewards.

Lend-Grow deposits the payback reward directly to the loan account you specify at the time of Payback Reward enrollment. Payback reward is not a rate discount and you must continue to meet your full payment obligations with the lender each month.

Apply at Lend-Grow today and pay down your loans faster.

About Sarah Horvath

Sarah is an expert in the insurance, investing for retirement and cryptocurrency space.