Amazon AMZN filed its annual Form 10-K last week. Our analysts have picked through the financial footnotes and fine print. 2013 results reinforce my bearish thesis from May of 2013 that AMZN’s valuation (~$360/share) implies a more unrealistic level of growth and profitability than investors realize.

Profit (NOPAT) margins and return on invested capital (ROIC) have continued their downward trend. Revenue growth has slowed. The future cash flow expectations in the stock’s valuation look even more unlikely for the company to achieve.

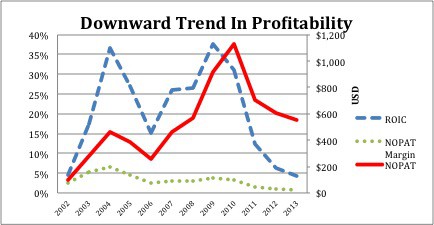

Margins and ROIC in Decline

2013 was Amazon’s worst year in over a decade in terms ofNOPAT margin and ROIC. AMZN’s margins were a paltry 0.7% in 2013, down from 1% the year before, while ROIC shrunk from 6.4% in 2012 to 4.2% last year. Figure 1 shows the long-term trend in margins and ROIC.

Figure 1: NOPAT, NOPAT Margin, and ROIC

Sources: New Constructs, LLC and company filings

GAAP net income says that AMZN swung from a loss in 2012 to a profit in 2013, but in fact the company’s NOPAT declined this past year. Our NOPAT metric strips away non-operating items to get at the cash generated by the company’s core operations.

Looking at NOPAT, we can see that AMZN’s profits have declined for three straight years. Even with double-digit revenue growth, the shrinking of AMZN’s margin has eaten away at profits. Reported earnings can be muddled or unclear, but NOPAT and ROIC tell a clear story of a company with declining profitability.

Slowing Revenue Growth

In addition to the profitability concerns, AMZN’s revenue growth appears to be decelerating. This could be an even bigger concern in the short-term as revenues, rather than profits, have been the driving force behind AMZN’s lofty valuation.

AMZN’s revenue grew by 22% in 2013, its lowest rate since 2001. Its revenue per employee declined by 8% to $635,000. While many companies would envy that figure, it’s the worst mark for Amazon in over a decade. At its peak profitability in 2009 and 2010, AMZN earned over $1 million in revenue per employee.

Everything we’re seeing from AMZN—the declining margin, slowing growth, and decreased efficiency—suggests that the company is really pushing to keep its revenue growth in-line with expectations. One has to wonder how much longer AMZN can keep up 20+% revenue growth. As soon as AMZN’s revenue growth slows to a more modest rate, it will have to start being valued based on profits, and even the most ardent AMZN bulls know it doesn’t have a leg to stand on there.

Valuation Remains Inflated

I won’t spend too much time on this section, as it’s not exactly a secret that AMZN is expensive. However, it’s helpful to dig a little deeper and quantify just how much growth is baked into AMZN’s valuation.

AMZN’s current valuation of ~$340/share implies that the company will grow NOPAT by 28% compounded annually for 18 years. The amount of growth would put Amazon’s NOPAT at $48 billion, which is 2 and a half times more than Wal-Mart’s NOPAT in 2013. I just don’t see that level of growth happening. To grow profits that much it would need to expand margins, but the steps it would have to take to do so (raising prices, cutting back on discretionary expenses like marketing) would in turn slow revenue growth.

Similar to my thesis with Apple (AAPL), Amazon cannot grow market share and raise prices at the same time. Something has to give. With margins near zero, I am not sure how much they have left to give on pricing and margins. And given the recent revenue growth rate decline, it is not clear how well their pricing strategy is working.

AMZN operates in a competitive landscape. It’s no longer the only name in online retail. Every brick and mortar store has an online store as well, and companies like Best Buy BBY that had been left for dead are making a renewed effort to compete with AMZN on price. AMZN’s scale and distribution network still give it an advantage over these competitors, but this advantage is clearly not significant enough to allow AMZN to expand its margins.

Retail is a low-margin business, especially when you go the low price route as AMZN has. The company clearly wants to expand beyond retail, but so far its ventures have just taken it into other competitive businesses. Its foray into online content creation with original programming on Amazon Prime puts it into competition with Netflix (NFLX) and Hulu, while Amazon Web Services competes with a wide variety of cloud platforms. AMZN keeps searching for a way out, but it’s hard to see what strategic move it could make that would allow for the profit growth its valuation implies.

Sam McBride contributed to this report.

Disclosure: David Trainer and Sam McBride receive no compensation to write about any specific stock, sector, or theme.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.