This report is one of a series on the adjustments we make to convert GAAP data to economic earnings. This report focuses on an adjustment we make to convert the reported balance sheet assets into invested capital.

Reported assets don’t tell the whole story of the capital invested in a business. Accounting rules provide numerous loopholes that companies can exploit to hide balance sheet issues and obscure the true amount of capital invested in a business.

Converting GAAP data into economic earnings should be part of every investor’s diligence process. Performing detailed analysis of footnotes and the MD&A is part of fulfilling fiduciary responsibilities.

We’ve performed unrivalled due diligence on 5,500 10-Ks every year for the past decade.

When a company makes an acquisition, the entire purchase price is added to the company’s balance sheet in the year of the acquisition along with any assumed debts or other long-term liabilities. However, the only income added to the income statement is that which occurs after the acquisition closes. In other words, the balance sheet is charged with the full price of the acquisition while the income statement only gets partially impacted.

Except for the rare event that an acquisition closes on the first day of the fiscal year, one must adjust for this accounting mismatch of income vs capital deployed when calculating return on invested capital (ROIC).

To ensure an accurate measurement of cash-on-cash returns, we adjust invested capital to reflect the time-weighted value of the acquisition. This adjustment is necessary to ensure the impact of the acquisition on NOPAT is commensurate with its impact on invested capital.

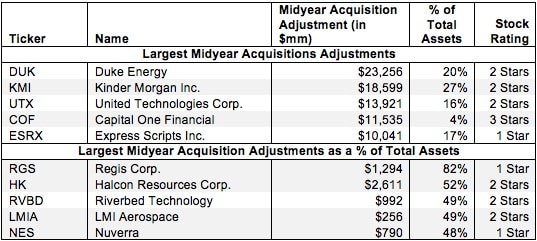

For example, Duke Energy DUK had over $23 billion in midyear acquisition adjustments to invested capital in 2012 for two acquisitions they made during the year. The biggest adjustment came from DUK’s acquisition of competitor Progress Energy on July 2, 2012. DUK paid $18 billion for Progress Energy and acquired an additional $27 billion in debt and other long-term liabilities. Because this acquisition occurred about mid year, we only added $22.6 billion, or the portion of the $45.3 billion that was on DUK’s books for the 182 days after the acquisition closed last year, to DUK’s invested capital for 2012.

Without this adjustment, any measures of return on assets or equity are distorted by the accounting treatment of midyear acquisitions.

Figure 1 shows the five companies with the largest midyear acquisitions adjustments to invested capitalin 2012 and the five companies with the largest midyear acquisition adjustments as a percent of total assets.

Figure 1: Companies With the Largest Invested Capital Adjustment in 2012

Energy and aerospace companies make up four of the ten companies in Figure 1. However, they are far from the only companies that are affected by midyear acquisition adjustments. In 2012 alone, we found 1,139 companies with midyear acquisition adjustments totaling over $343 billion. For all years, our database contains 3,773 instances of acquisition adjustments totaling over $1 trillion.

Since our midyear acquisition adjustments decrease invested capital, companies with significant midyear acquisition adjustments will have a meaningfully higher return on invested capital (ROIC) when this adjustment is applied. For instance, Riverbed Technology, Inc RVBD acquired OPNET on December 18, 2012. RVBD paid roughly $1 billion. Since this acquisition occurred with only 13 days remaining in the year, we include only 13/365 of that $1 billion in RVBD’s average invested capital for the year.

If we simply used the year-end balance sheet data for invested capital, RVBD would have had an ROIC of only 5.6%. Adjusting for the amount of time that RVBD did not have access to the assets from its acquisition of OPNET, we see that it earned an ROIC of 24.1%.

Investors who ignore the impact of midyear acquisitions on invested capital are holding companies accountable for earning returns on assets to which they cannot lay claim for part of the year. By adjusting invested capital for midyear acquisitions, one can get a better picture of the value that management is creating for shareholders. Diligence pays.

Sam McBride and André Rouillard contributed to this report.

Disclosure: David Trainer and Sam McBride receive no compensation to write about any specific stock, sector, or theme.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.