An emerging trend I've identified with new ETFs that have come to market over the past year or two is that providers are now giving investors less of what they "need", and more of what they "want". Think about it for a moment, in the early days of ETF innovation, funds were brought to market to satisfy a specific need within a portfolio. Providers knew that investors required exposure through an ETF to every corner of the equity and bond market if widespread adoption would ever take hold. Now that we've reached a saturation point for the needs of investors, providers are focusing on the wants.

Which brings me to the same conclusion as to why certain mutual funds have remained popular for decades; investors simply want access to superior returns. They want less beta options and more alpha options for their portfolios, since its the intermingling of the two that will most likely allow a typical retail investor to outperform their own expectations over the short and long term. For these reasons, I believe the development trend of actively managed exchange-traded products will at least stay intact, if not accelerate in the years ahead.

I have made it clear in the past that I think that due to it's sheer size, the bond market is a place where investors can more readily seek out opportunities for alpha. A shinning example of this was the creation of actively managed bond ETFs such as the PIMCO Total Return ETF )BOND), which quickly became one of the most successful ETF launches in history. In addition, a lesser know fund, the PIMCO Inflation Linked Bond ETF (ILB) has posted very respectable performance since its inception. I will even point out the WisdomTree Emerging Market Corporate Bond Fund (EMCB) as an excellent option in comparison to it's passively managed counterparts. The reason I bring these three funds to light is that I think they all make great representatives of this new category of ETF, and I look forward to the continued opportunity and prosperity that each respective management team can bring to the table.

With the continued success of those funds in mind, I want to point out a recent newcomer that has already posted some excess returns in comparison to it's peers. The First Trust Preferred Securities and Income ETF (FPE), is an actively managed fund run by Stonebridge Advisors that invests at least 80% of its assets in preferred stocks. Stonebridge is an investment advisor that specializes in the niche' market of hybrid income producing securities such as preferred stocks and convertible bonds, and their strategy is to seek total return in conjunction with current income from the 85 holdings within FPE's portfolio. Performing a quick Morningstar ETF screen, there are really only three or four other preferred ETFs that are suitable comparisons to the new First Trust offering. However, FPE is the only fund that is actively managed, making it an excellent alternative for the roughly 12.5 Billion that has taken up residence in the popular iShares U.S. Preferred Stock ETF (PFF).

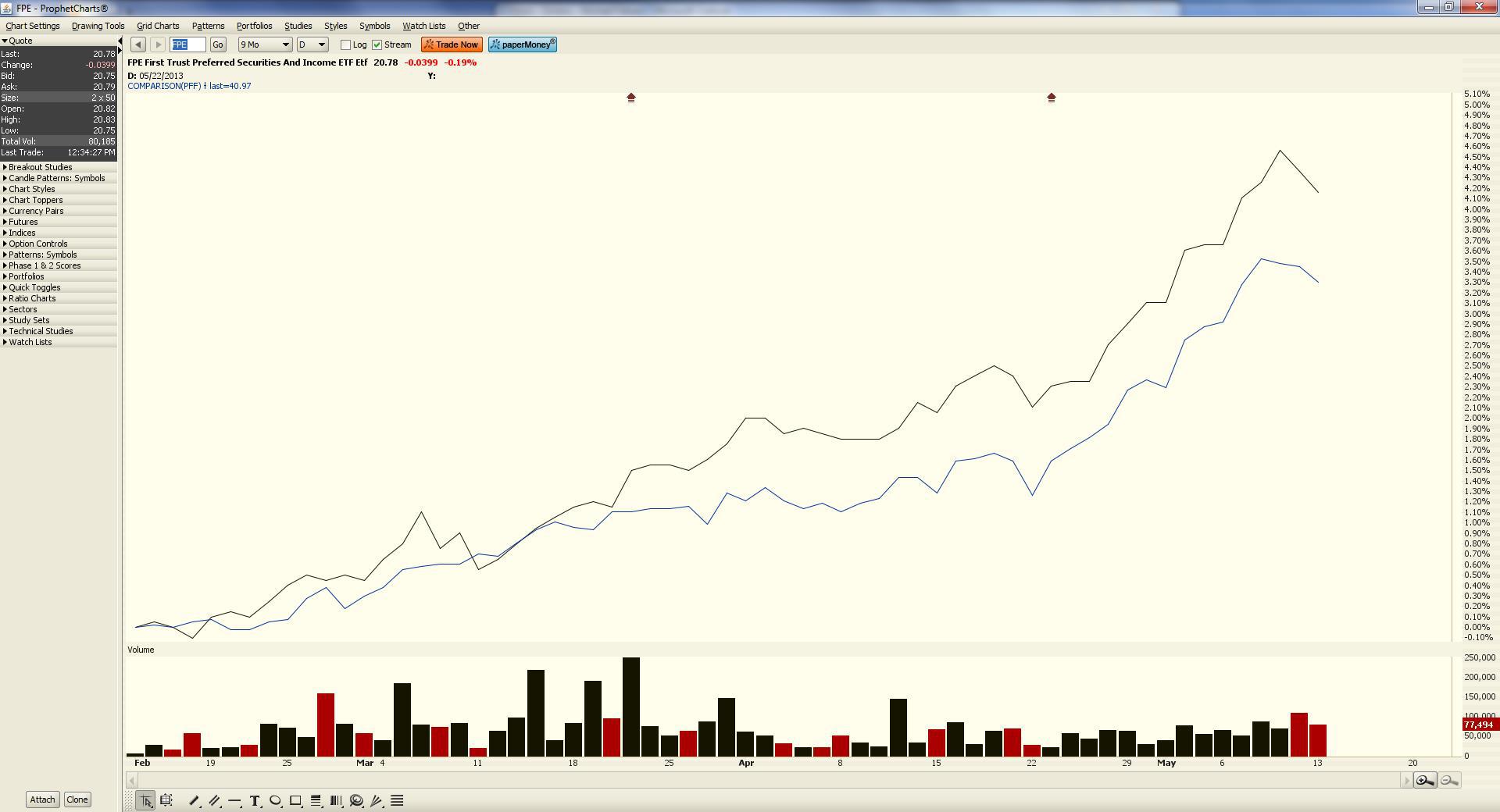

Looking at the chart below, In a very short term performance comparison of FPE (since inception) and PFF, the First Trust fund was able to outperform by a margin of approximately 0.90% over the past 3 months. Nothing to ride home about yet, but performance divergences have to start somewhere, so it will be interesting to see how a full year comparison stacks up.

(click to enlarge)

In drilling down into a few more of the meaningful traits each fund possesses. I will point out that FPE has a much higher management fee, with an expense ratio of 0.85% vs just 0.48% for PFF. Although it appears to be benefiting from a more concentrated mix of holdings than PFF's 316, it will be interesting to see what the next correction will bring. Preferred stocks can fall hard and fast during any type of financial crisis since the majority of issuance in the asset class is offered by banks and insurance companies. So I'm curious to see if FPE will shift its portfolio to more defensive utility and industrial preferreds in response to any future hiccups in our financial system. Another interesting thought is what changes, if any, Stonebridge will make to counteract a rise in long term interest rates, which can have a detrimental impact on preferred stocks. Its that type of fundamental expertise in security selection and strategic transitioning I will be watching for that would persuade me the additional cost is worth the price.

In closely examining FPE, I think it offers all the right characteristics I look for in an actively managed ETF. Although from a timing perspective I'm not compelled to enter a new position within the fund today, it has been permanently added to may watchlist for a future allocation at a time when preferreds offer better relative value. We have gone quite awhile without a substantial correction in this space due to the ramped chase for yield, so patience will continue to play a vital role in the establishment of a position within my client's portfolios.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.