For decades, analysts and investor have bought into the idea of a small cap premium, i.e., that stocks with low market capitalizations can be expected to earn higher returns than stocks with higher market capitalizations. For investors, this has led to the pursuit of small cap stocks and funds for their portfolios, and for analysts, it has translated into the addition of "small cap" premiums of between 3-5 percent to traditional model-based expected returns, for companies that they classify as small cap. While I understand the origins of the practice, I question the adjustment for three reasons:

On closer scrutiny, the historical data, which has been used as the basis of the argument, is yielding more ambiguous results and leading us to question the original judgment that there is a small cap premium.

The forward-looking risk premiums, where we look at the market pricing of stocks to get a measure of what investors are demanding as expected returns, are yielding no premiums for small cap stocks.

If the justification is intuitive, i.e., that smaller firms are riskier than larger firms, much of that additional risk is either diversifiable, better adjusted for in the expected cash flows (instead of the discount rate) or double counted.

The small cap premium is a testimonial to the power of inertia in corporate finance and valuation, where once a practice becomes established, it becomes difficult to challenge, even if the original reasons for it have long since disappeared.

The Basis

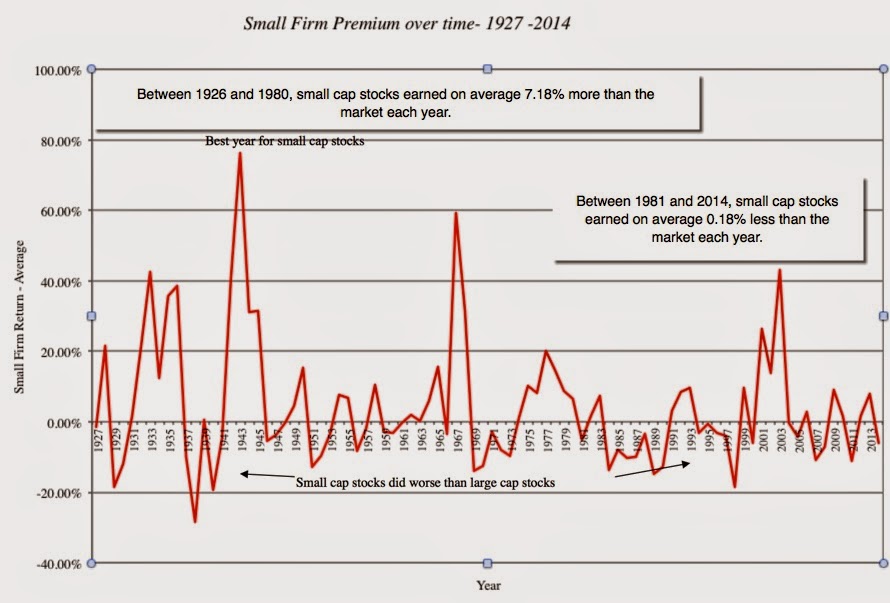

The first studies that uncovered the phenomenon of the small cap premium came out in the 1970s. They broke companies down into deciles, based on market capitalization, and found that companies in the lowest decile earned higher returns, after adjusting for conventional risk measures, than companies in the highest decile. I updated those studies through the end of 2014, and the small cap premium seems intact (at least at first sight). In summary, looking at returns from 1926 to 2014, the smallest cap stocks (in the lowest decile) earned 4.33 percent more than the market, after adjusting for risk.

|

| Source: Ken French's online data |

This is the strongest (and perhaps) only evidence for a small cap premium and it is reproduced in data services that try to estimate historical risk premiums (Ibbotson, Duff and Phelps etc.). This historical premium has become the foundation for both valuation and investment practice. In valuation, analysts have referenced this table to estimate a small cap premium (4-5 percent) that they then add to the required return from conventional risk and return models to estimate discount rates. For instance, in the conventional capital asset pricing model, it plays out as follows:

Expected Return = Risk free rate + Beta * Equity Risk Premium + Small Cap Premium

That discount rate is used to estimate the value of future cash flows, and not surprisingly, the use of a small cap premium lowers the value of smaller companies.

In investing, it has been used as a weapon both for and against active investing. Those who favor active investing have pointed to the small cap premium as a justification for their activity, and during the periods of history when small cap companies outperformed the market, it did make them look like heroes but it quickly gave rise to a counterforce, where performance measurement services (like Morningstar) started incorporating portfolio tilts, comparing small cap funds against small cap indices. Since almost all of the "excess returns" disappeared on this comparison, it was only a matter of time before index funds entered the arena, creating small-cap index funds for investors who wanted to claim the premium, without paying large management fees.

The Problem With The Historical Premium

In the decades since the original small cap premium study, the data on stocks has become richer and deeper, allowing us to take a closer look at the phenomenon. There are some serious questions that can be raised about whether the premium exists and if so, what exactly it is measuring:

- Trend lines and Time Periods: Small cap stocks have earned higher returns than large cap stocks between 1928 and 2014 but the premium has been volatile over history, disappearing for decades and reappearing again. While the premium was strong prior to 1980, it seems to have dissipated since 1981. One reason may be that the small cap premium studies drew attention and investor money to small cap stocks, and in the process led to a repricing of these stocks. Another is that the small cap premium is a side effect of larger macroeconomic variables (inflation, real growth etc.) and that the behavior of those variables has changed since 1980.

|

| Source: Ken French's online data |

Standard Error: Historical equity returns are noisy and any estimates of risk premium from that data will reflect the noise in the form of large standard errors on estimates. I have made this point about the overall historical equity risk premium but it becomes magnified when you dice and slice historical data into sub-classes. The table below lists standard errors in excess returns by decile class and reinforce the notion that the small cap premium is fragile, barely making the threshold for statistical significance over the entire period.

|

| Source: Ken French's online data |

The January Effect: One of the most puzzling aspects of the small cap premium is that almost all of it is earned in one month of the year, January, and removing that month makes it disappear. So what? If your argument for the small cap premium is that small cap stocks are riskier, you now have the onus of explaining why that risk shows up only in the first month of every year.

|

| Source: Ken French's online data |

Weaker globally: The small cap premium seems to be smaller in non-US markets than in US markets and is non-existent in some. In contrast, the value effect (where low price to book stocks outperform the market) is strong globally.

Proxy for other factors: A host of papers argue that the bulk or all of the small size effect can be attributed to a liquidity effect and that putting in a proxy for illiquidity makes the size effect disappear or diminishes it.

Works only with market cap: Finally, you can take issue with the use of a market-priced based measure of size in a study of returns. Others have tried other non-price size measures such as income or revenues but there seems to be no size effect in those variables.

A recent working paper by Asness, Frazini, Moskowitz and Pedersen tries to resurrect the size effect, but accomplishes it only by removing the subset of small companies that they classify as "low quality" or "junk".

While the results are interesting and can be used by active small-cap fund managers as a justification for their activity, they are in no way a basis for adding a small cap premium to every small company, and asking analysts to add it on only for small, high quality companies is problematic. In summary, if the only justification that you can offer for the addition of a small cap premium to your discount rate is the historical risk premium, you are on thin ice.

Market-Implied Small Cap Premium

If the historical data ceases to support the use of a historical risk premium, can we then draw on intuition and argue that since small companies tend to be riskier (or we perceive them to be), investors must require higher return when they invest in them? You can, but the onus is then on you to back up that intuition.

In fact, you can check to see whether investors are demanding a forward looking "small cap" premium, by looking at how they price small as opposed to large companies, and backing out what investors are demanding as expected returns. Put simply, if small cap stocks are viewed by investors as riskier and that risk is being priced in, you should expect to see, other things remaining equal, higher expected returns on small cap stocks than large cap stocks.

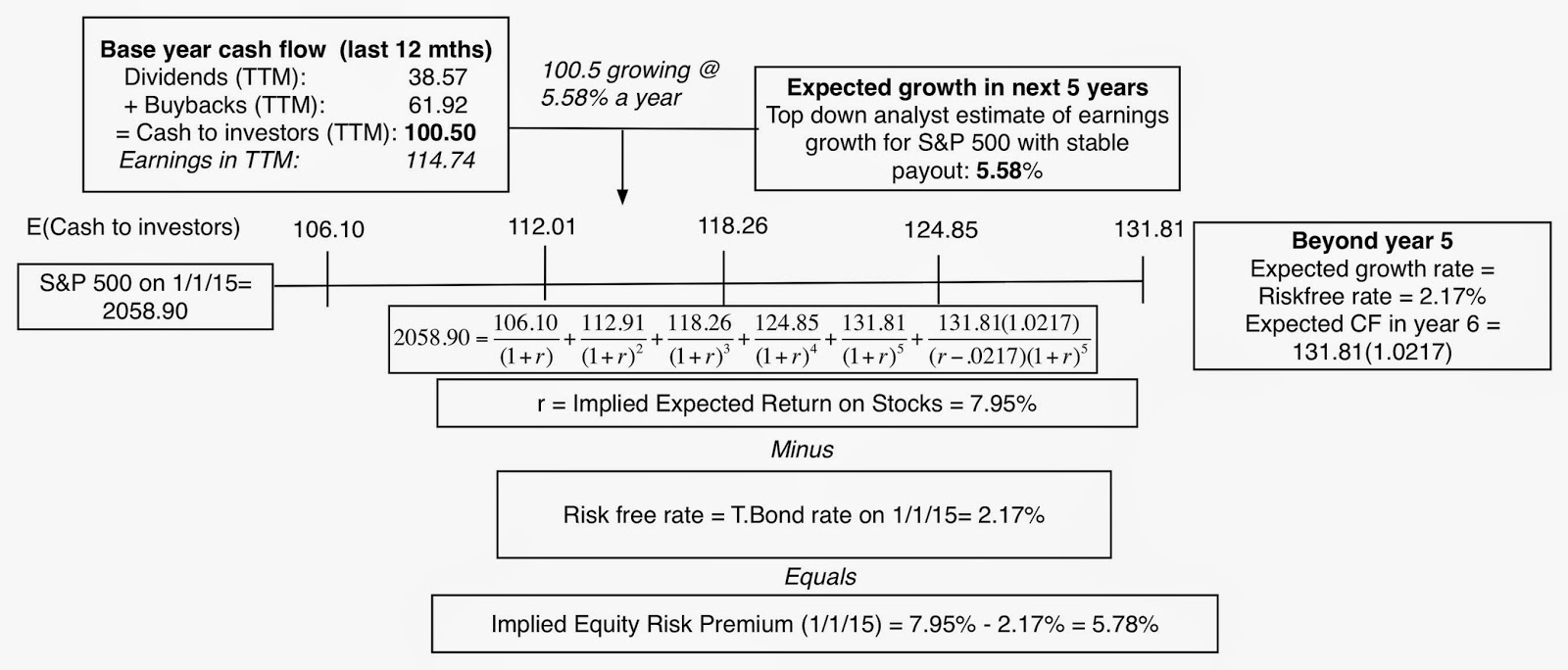

As some of you are aware, I compute a forward-looking equity premium for the S&P 500 at the start of each year, backing out the number from the current level of the index and expected cash flows. On January 1, 2015, this is what I found:

To get a measure of the forward-looking small cap premium, I computed the expected return implied in the S&P 600 Small Cap Index, using the same approach that I used for S&P 500. In spite of using a higher expected earnings growth for small cap stocks, the expected return that I estimate is only 7.61 percent:

In effect, the market is attaching a smaller expected return for small cap stocks than large ones, stories and intuition notwithstanding.

I am not surprised that the market does not seem to buy into the small cap premiums that academics and practitioners are so attached to. After all, if the proponents of small cap premiums are right, bundling together small companies into a larger company should instantly generate a bonus, since you are replacing the much higher required returns of smaller companies with the lower expected return of a larger one.

In fact, small companies should disappear from the market.

The Illiquidity Fig Leaf

Looking at the data, the only argument left, as I see it, for the use of the small cap premium is as a premium for illiquidity, and even on that basis, it fails at one of these four levels:

If illiquidity is your bogey man in valuation, why use market capitalization as a stand-in for it? Market capitalization and illiquidity don't always go hand in hand, since there are small, liquid companies and large, illiquid ones in the market. Four decades ago, your excuse would have been that the data on illiquidity was either inaccessible or unavailable and that market capitalization was the best proxy you could find for illiquidity.

That is no longer the case and there are studies that categorize companies based on measures of illiquidity (bid ask spread, trading volume) and find an "liquidity premium" for illiquid companies.

If illiquidity is what you are adjusting for in the small cap premium, why is it a constant across companies, buyers and time? Even if your defense is that the small cap premium is an imperfect (but reasonable) measure of the illiquidity premium, it is unreasonable to expect it to be the same for every company.

Thus, even if you are valuing just privately owned businesses (where illiquidity is a clear and present danger), that illiquidity should be greater in some businesses than in others and the illiquidity (or small cap) premium should be larger for the former than the latter. Furthermore, the premium you add to the discount rate should be higher in some periods (during market crises and liquidity crunches) than others and for some buyers (cash poor, impatient) than others (patient, cash rich).

Even if you can argue that illiquidity is your rationale for the small cap premium and that it is the same across companies, why is it not changing over the time horizon of your valuation (and especially in your terminal value)? In any valuation, you assume through your company's cash flows and growth rates will change over time and it is inconsistent (with your own narrative for the company) to lock in an illiquidity premium into your discount rate that does not change as your company does.

Thus, if you are using a 30 percent expected growth rate on your company, your "small" company is getting bigger (at least according to your estimates) and presumably more liquid over time. Should your illiquidity premium therefore not follow your own reasoning and decrease over time?

If your argument is that size is a good proxy for illiquidity, that all small companies are equally illiquid and that that illiquidity does not change as you make them bigger, why are you reducing your end value by an illiquidity discount? This question is directed at private company appraisers who routinely use small cap premiums to increase discount rates and also reduce the end (DCF) value by 25 percent or more, because of illiquidity. You can show me data to back up your discount (I have seen restricted stock and IPO studies) but none of them can justify the double counting of illiquidity in valuation.

Why Are We Slow To Give Up On The Small Cap Premium?

It is true that the small cap premium is established practice at many appraisal firms, investment banks and companies. Given the shaky base on which it is built and how much that base has been chipped away in the last two decades, you would think that analysts would reconsider their use of small cap premiums, but there are three powerful forces that keep it in play.

Intuition: Analysts and investors not only start of with the presumption that the discount rates for small companies should be higher than large companies, but also have a "number' in mind. When risk and return models deliver a much lower number, the urge to add to it to make it "more reasonable" is almost unstoppable.

Consequently, an analyst who arrives at an 8 percent cost of equity for a small company feels much more comfortable after adding a 5 percent small cap premium. It is entirely possible that you are an idiot savant with the uncanny capacity to assess the right discount rate for companies, but if that is the case, why go through this charade of using risk and return models and adding premiums to get to your "intuited" discount rate? For most of us, gut feeling and instinct are not good guides to estimating discount rates and here is why.

Not all risk is meant for the discount rate, with some risk (like management skills) being diversifiable (and thus lessened in portfolios) and other risks (like risk of failure or regulatory approval) better reflected in probabilities an expected cash flow. A discount rate cannot and is not meant to be a receptacle for all your hopes and fears, a number that you can tweak until your get to your comfort zone.

Inertia (institutional and individual): The strongest force in corporate finance practice is inertia, where much of what companies, investors and analysts do reflects past practice. The same is true in the use of the small cap premium, where a generation of analysts has been brought up to believe (by valuation handbooks and teaching) that it is the right adjustment to make and now do it by rote.

That inertia is reinforced in the legal arena (where many valuations end up, either as part of business or tax disputes) by the legal system's respect for precedence and general practice. You may view this as harsh, but I believe that you will have an easier time defending the use of a bad, widely used practice of long standing in court than you would arguing for an innovative better practice.

Bias: My experiences with many analysts who use small cap premiums suggest to me that one motive is to get a "lower" value". Why would they want a lower value? First, in accounting and tax valuation, the client that you are doing the valuation for might be made better off with a lower value than a higher one.

Consequently, you will do everything you can to pump up the discount rate with the small cap premium being only one of the many premiums that you use to "build up" your cost of capital. Second, there seems to be a (misplaced) belief that it is better to arrive at too low a value than one that is too high. If you buy into this "conservative" valuation approach, you will view adding a small cap premium as costless, since even it does not exist, all you have done is arrived at "too low" a value.

At the risk of bringing up the memories of statistics classes past, there is always a cost. While "over estimating" discount rates reduces type 1 errors (that you will buy an over valued stock), it comes at the expense of type 2 errors (that you will hold off on buying an under valued stock).

A Requiem For The Small Cap Premium?

I have never used a small cap premium, when valuing a company and I don't plan to start now. Needless to say, I am often asked to justify my non-use of a premium and here are my reasons. First, I am not convinced by either the historical data or by current market behavior that a small cap premium exists.

Second, I do believe that small cap companies are more exposed to some risks than large cap companies but there are other more effective devices to bring these risks into valuation. If it is that they are capital constrained (i.e., that it is more difficult for small companies to raise new capital), I will limit their reinvestment and expected growth (thus lowering value). If it is that they have a greater chance of failure, I will estimate a probability of failure and reflect that in my expected value (as I do in my standard DCF model).

If it is illiquidity that is your concern, it is worth recognizing that one size will not fit all and that the effect on value will vary across investors and across time and will be better captured in a discount on value.

To illustrate how distorted this debate has become, note that those who routinely add small cap premiums to their discount rates are not put to the same test of justifying its use. So, at the risk of opening analysts up to uncomfortable questions, here are some questions that you should pose to anyone who is using a small cap premium (and that includes yourself):

What is your justification for using a small cap premium? If the defense is pointing to history (or a data table in a service), it is paper thin, since that historical premium defense seems to have more holes in it than Swiss cheese. If it is intuitive, i.e., that small companies are riskier and markets must see them as such, I don't see the basis for the intuition, since the implied costs of equity for small companies are no higher than those of large companies. If the argument is that everyone does it, I am sorry but just because something is established practice does not make it right.

What are the additional risks that you see in small companies that you don't see in large ones? I am sure that you can come up with a laundry list that is a mile long, but most of the risks on the list either don't belong in the discount rate (either because they are diversifiable or because they are discrete risks) or can be captured through probability estimates. If it is illiquidity that you are concerned about, see the section on illiquidity above for my response.

If you are investors, here are the lessons I draw from looking at the data. If you are following a strategy of buying small cap stocks, expecting to be rewarded with a premium for just doing that, you will be disappointed.

Even the most favorable papers on the small cap premium suggest that you have to add refinements, with some suggesting that these refinements should screen out the least liquid, riskiest small cap stocks and others arguing for value characteristics (stable earnings, high returns on equity & capital, solid growth).

I do think that there is a glimmer of hope in the recent research that the payoff to looking for under valued stocks may be greater with small companies, partly because they are more likely to be overlooked, but it will take more work on your part and it won't be easy!

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.