Looking at the broader consumer discretionary sector, the National Retail Federation, or NRF, estimates retail sales in 2017 are likely to increase between 3.7% and 4.2% year-over-year (excluding automobiles, gasoline stations and restaurants). That’s roughly in line with the 3.8% increase in retail sales in 2016. “Prospects for consumer spending are straightforward – more jobs and more income will result in more spending,” NRF Chief Economist Jack Kleinhenz said. If wages grow faster than expected and job growth continues, it could be the big catalyst that pushes consumers to spend even more.

That could help revenue growth at companies like Nike and Under Armour that sell higher-priced products than competitors. According to Nike, their revenue growth declined from 14% in fiscal 2015 to 12% revenue growth in fiscal 2016, and slowed to 9% in the first half of fiscal 2017. On Nike’s Q2 2017 conference call, Chief Financial Officer Andy Campion said they expect revenue to grow “squarely in the mid-single-digit range” in Q3 2017. Nike’s Q2 gross profit margin declined 1.4% year-over-year, to 44.2%. The company blamed contracting margins on higher product costs, foreign exchange headwinds, and a larger mix of off-price products—products sold through discount retailers—in its Q2 earnings call. Roughly half of Nike’s business is outside of North America, and the company has acknowledged the strong U.S. dollar and will likely continue to pressure margins in future quarters.

Competitive Pressures

On top of the bankruptcy of major sporting-goods retailer The Sports Authority, which impacted many consumer discretionary companies, Nike has acknowledged greater challenges from competitors like Under Armour. Under Armour’s sales have been growing in the mid- to high-double digits while Nike’s dropped to high-single digits in the past several quarters. One thing to note is Nike is significantly larger than most of its competitors and sales growth tends to slow the larger a company gets, while smaller companies like Under Armour are usually able to grow more quickly.

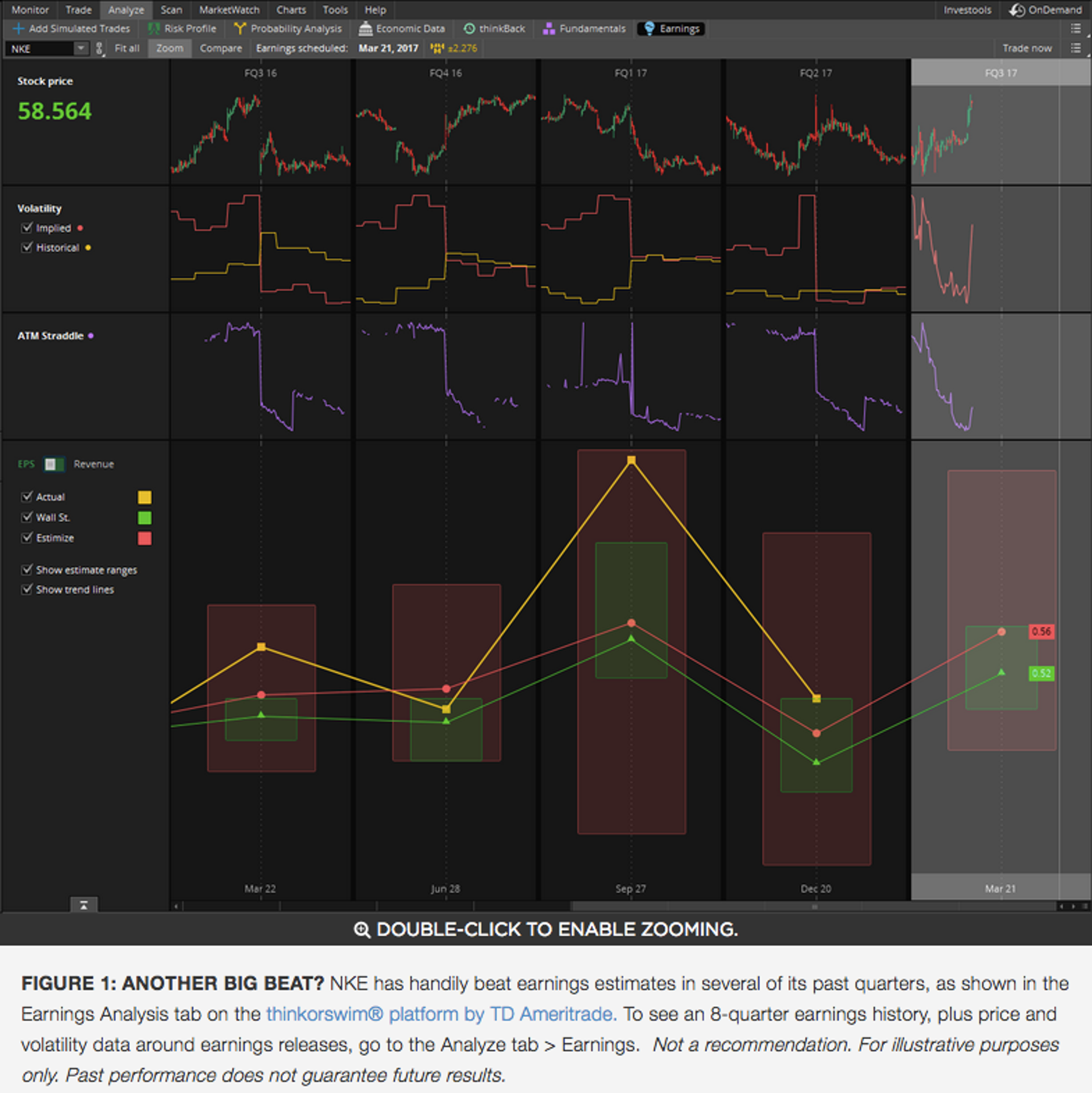

Nike’s Q3 consensus earnings estimate from third-party Wall Street analysts is $0.52 a share, according to the Earnings Analysis tab on the thinkorswim® platform from TD Ameritrade Holding Corp.AMTD. Revenue is projected to increase 5.2% to $8.45 billion, from $8.03 billion in Q3 2016.

The options market has priced in an expected share price move of 4.2% in either direction around the earnings release, according to the Market Maker Move™ indicator on the thinkorswim® platform.

Calls have been active at the weekly 58 strike while puts have seen activity at the weekly 54 and 57.5 strikes. The implied volatility sits at the 57th percentile. (Please remember past performance is no guarantee of future results.)

Note: Call options represent the right, but not the obligation, to buy the underlying security at a predetermined price over a set period of time. Put options represent the right, but not the obligation, to sell the underlying security at a predetermined price over a set period of time.

Looking Ahead

There’s a month to go until Under Armour reports Q1 2017 earnings. Many analysts considered Under Armour one of the biggest threats to Nike’s dominance of sporting apparel, but it has faced some of its own growing pains and its stock has lost about a quarter of its value since the beginning of 2017. Some things investors might want to keep an eye on over the next several quarters are Nike’s forward guidance for holiday quarters, if profit margins are improving, and its performance compared to the competition.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Date | ticker | name | Actual EPS | EPS Surprise | Actual Rev | Rev Surprise |

|---|

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.