Two more big banks, Goldman Sachs Group Inc GS and Citigroup Inc C, are scheduled to open the books on their Q4 performances before the markets open Wednesday. If Friday’s robust results from its competitors are any indication, and some analysts believe they are, Q4 may have been a boon for GS and C too.

Overall, the three biggest U.S. banks that reported Friday, JPMorgan Chase & Co. JPM, Bank of America Corp BAC, and Wells Fargo & Co WFC submitted total net income that climbed 2% on a year-over-year basis to $64.6 billion in 2016—results that came with partial thanks to a Q4 revival in their trading units. Did GS and C enjoy such a renaissance as well? And how might investors fare under a new administration that has vowed to lower taxes and loosen the regulatory reins?

Goldman Sachs Revenue March

Some analysts have said they expect Q4 to show sizable results from a revenue perspective. Rising prices in stocks and the increased trading volumes that appeared evident in Q4 may inflate GS’ top line. Why? Some analysts say it’s because GS has the highest revenue concentration in the capital markets when compared with its closest rivals.

Like its big-bank competitors, GS’ investment units, both investing and lending, as well as its institutional client-services division, which makes markets and facilitates client transactions in equity, fixed income, currencies and commodities (FICC), are likely to have rung up healthy revenues in the energetic post-election trading environment.

Looking ahead, some analysts are likely to be listening for insight into what GS sees in mergers and acquisitions, as well as equity allocations. Like its competitors, GS’ M&A revenues appear to have been impacted by a slowdown in activity that some market watchers believe will be rejuvenated with the new administration in Washington.

Some analysts also note that the possible uplift in trading activity expected under a Trump administration may lead investors to juice their equity allocations in 2017. FICC trading is expected to climb by an estimated $15 billion over the next two years, according to a recent Barron’s article. Analysts add, however, that volatility may be jumpy.

Also of interest is what, if any, market share has GS picked up from European banks. JPM executives noted in their conference call that the bank had scooped up market share in investment banking fees in the U.S. and Europe. Some analysts say they expect the same from GS.

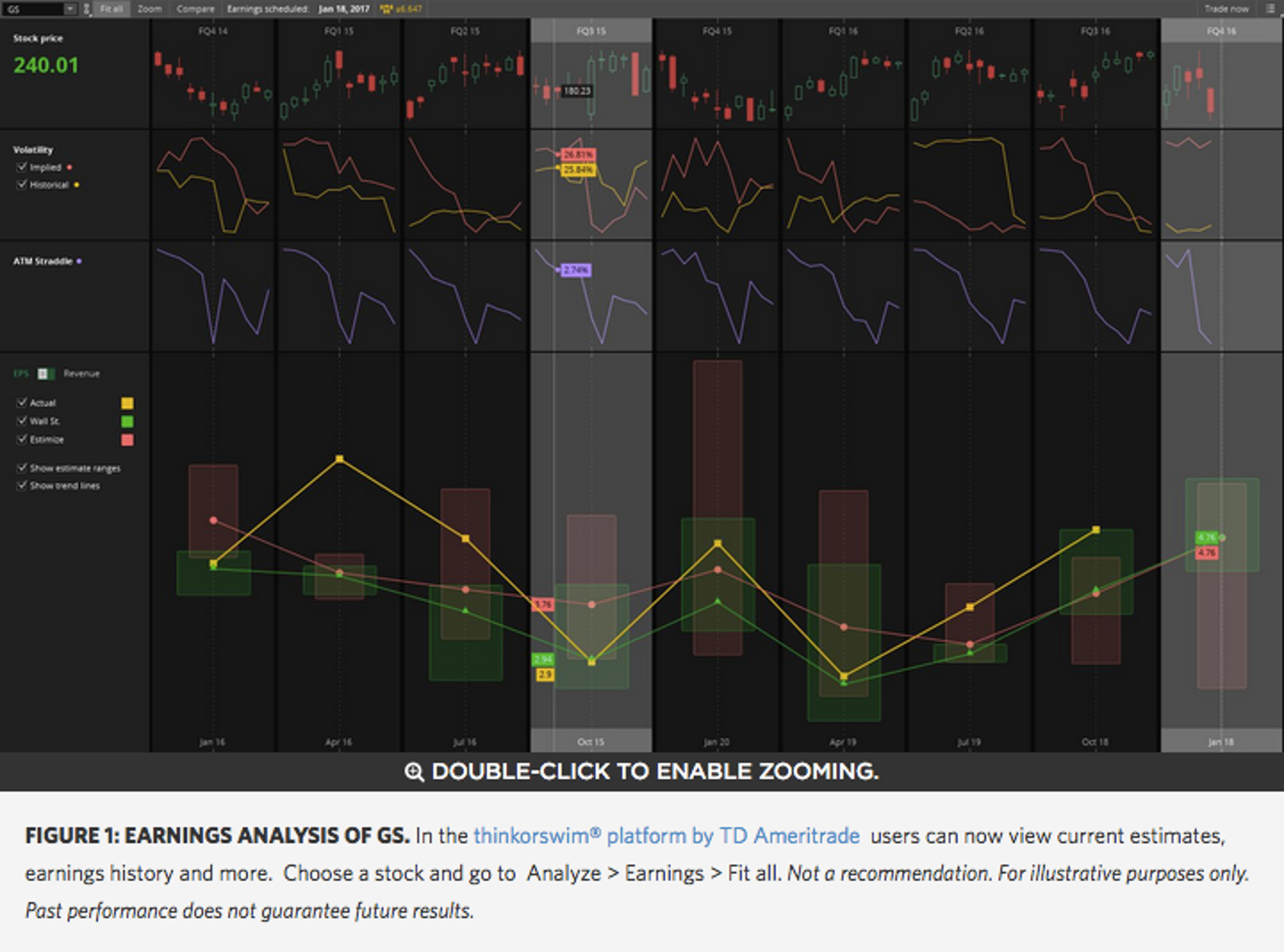

Data from Estimize* point to per-share earnings of $4.76. GS' earnings numbers have been trending higher all year, with the last three quarters coming in at $2.68, $3.72 and $4.88 respectively. Revenues are anticipated to reach $7.72 billion, up 5.5% from last year’s $7.3 billion. GS has outperformed Wall Street’s expectations in the last three quarters.

Short-term options traders have priced in a potential share price move of 2.7% in either direction around the earnings release, according to the Market Maker Move™ indicator on the thinkorswim® platform from TD Ameritrade.

There are call buyers at the weekly 245-strike and 250-strikes, with put activity heaviest at the 235 strike. The implied volatility sits at the 24th percentile. (Please remember past performance is no guarantee of future results.)

Note: Call options represent the right, but not the obligation, to buy the underlying security at a predetermined price over a set period of time. Put options represent the right, but not the obligation, to sell the underlying security at a predetermined price over a set period of time.

Citigroup Gets in on Rally Too

At a banking conference in November, Jamie Froese, C’s president, said his financial holdings group trading levels also had been a beneficiary of the surprise election results. But he cautioned then that there was still plenty of time left in the quarter. Moreover, he noted that he was looking for trading revenues to be slightly lower than they were in Q3 when banks reaped the benefits of uncertainty around the Brexit vote and a Federal Reserve rate hike. How might that have played out for C?

Remember, though, that C is well known for its credit card and consumer banking units. During the Q3 conference call, CFO Marianne Lake said she expected revenue growth across North America, Latin America and Asia on the consumer-banking business side. However, she remained cautious on mortgage activity, which she saw as slowing down from Q3, mostly because of seasonal factors.

Analysts also are looking at progress the bank is making in whittling down Citi Holdings, the so-called “bad bank” created in 2009 to house troubled assets in the wake of the financial crisis. Last year, CEO Michael Corbat said in a statement that “winding down Holdings has been a longtime goal and shows Citi’s progress in becoming a simpler, smaller, safer and stronger institution. Some analysts expect the unit to break even in Q4, but say they want to know what the next steps are.

At the Financial Times, analysts reporting see average earnings per share of $1.12 compared with $1.06 a year ago on revenues of $17.3 billion, below last years’ $18.6 billion.

Short-term options traders have priced in a potential share price move of 2.1% in either direction around the earnings release, according to the Market Maker Move™ indicator.

Options activity has been strong at the weekly 60-strike line for calls and at the 57.5 strike for puts. The implied volatility sits in the lower quarter at the 9th percentile. (Please remember past performance is no guarantee of future results.)

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

Date | ticker | name | Actual EPS | EPS Surprise | Actual Rev | Rev Surprise |

|---|

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.