Loading...

Loading...

On July 10, JMP Securities analyst Mitch Germain initiated coverage on Wheeler Real Estate Investment Trust

WHLR at Market Outperform.

Wheeler sports a market cap below $150 million, which is tiny compared with most publicly traded shopping center REITs.

Wheeler has been described by many REIT experts over the past year as being a speculative investment; largely because the current dividend distribution yielding over 10.5 percent, exceeds cash available for distribution.

However, as part of the JMP bullish case, Germain expects this situation to resolve favorably moving forward.

The Price Of Growth

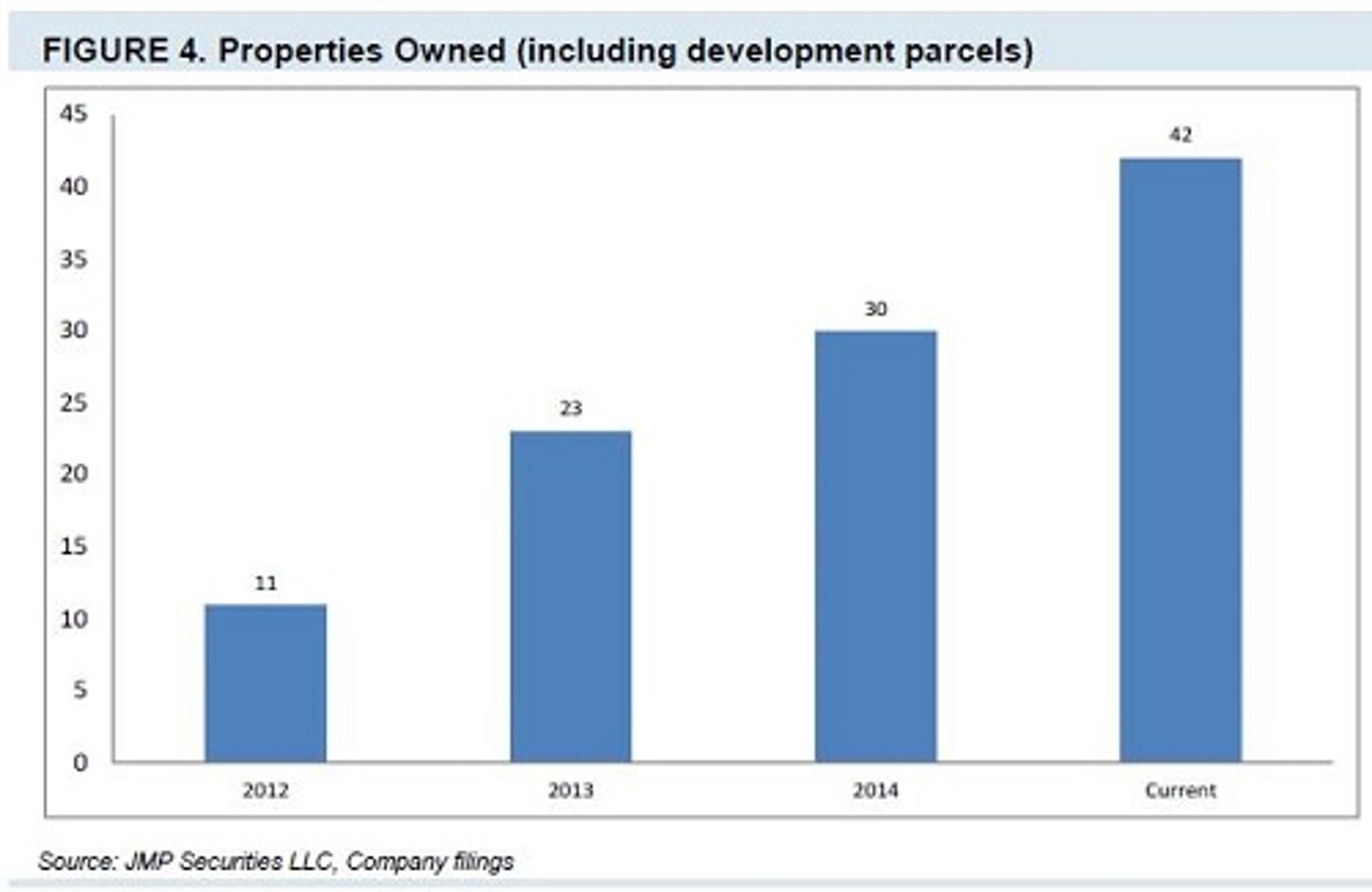

Wheeler became a publicly traded REIT in 2012, and currently owns 35 shopping center and 7 land parcels, located in secondary and tertiary markets.

This small market focus is key to the Wheeler investment thesis, because the REIT has little institutional competition for these acquisitions.

However, this growth path has not been a bed of roses for longer tenured WHLR shareholders with an IPO cost basis of $5.25 per share.

Tale Of The Tape - A Difficult Year

The first half of 2015 has featured a series of transformative WHLR balance sheet events, including a ~$93 million preferred stock private placement -- which converted to common at $2.00 per share -- structured when the stock was trading in the $3.50 per share range.

During the past 52-weeks, Wheeler shares have traded in a range of $1.93 - $4.71, closing up two cents on Friday at $1.98 per share.

A Recapitalized "Wheeler 2.0"

After shareholders voted to approve the recapitalization, CEO Jon Wheeler's 30 percent ownership stake was diluted down to 5 percent, as there are now 6x more common shares outstanding.

On June 1, Wheeler also announced a new $45 million revolving credit facility led by KeyBanc.

Along with the $93 million dilution, Wheeler shareholders gained experienced institutional investors as board members, with considerable skin in the game.

JMP - Wheeler: Market Outperform, $2.75 PT

The JPM $2.75 target price represents a potential ~40 percent upside in the shares, not including the current ~10.5 percent dividend yield.

The valuation was based upon JMP's "…2016 year-end forward NOI, which assumes that all capital raised from the convert offering is invested, and that a conservative $120M of new investments are initiated in 2016, funded with an even combination of equity and mortgage financing."

Germain utilized a 7.5% cap rate, conservative when "…compared to strip center cap rates of 7.2%, according to Real Capital Analytics, and the most recent CBRE Cap Rate Survey, which has class-B strip centers trading at 7% cap rates."

JMP valued Wheeler land holdings at cost since management has not given guidance on the timeframe for future developments.

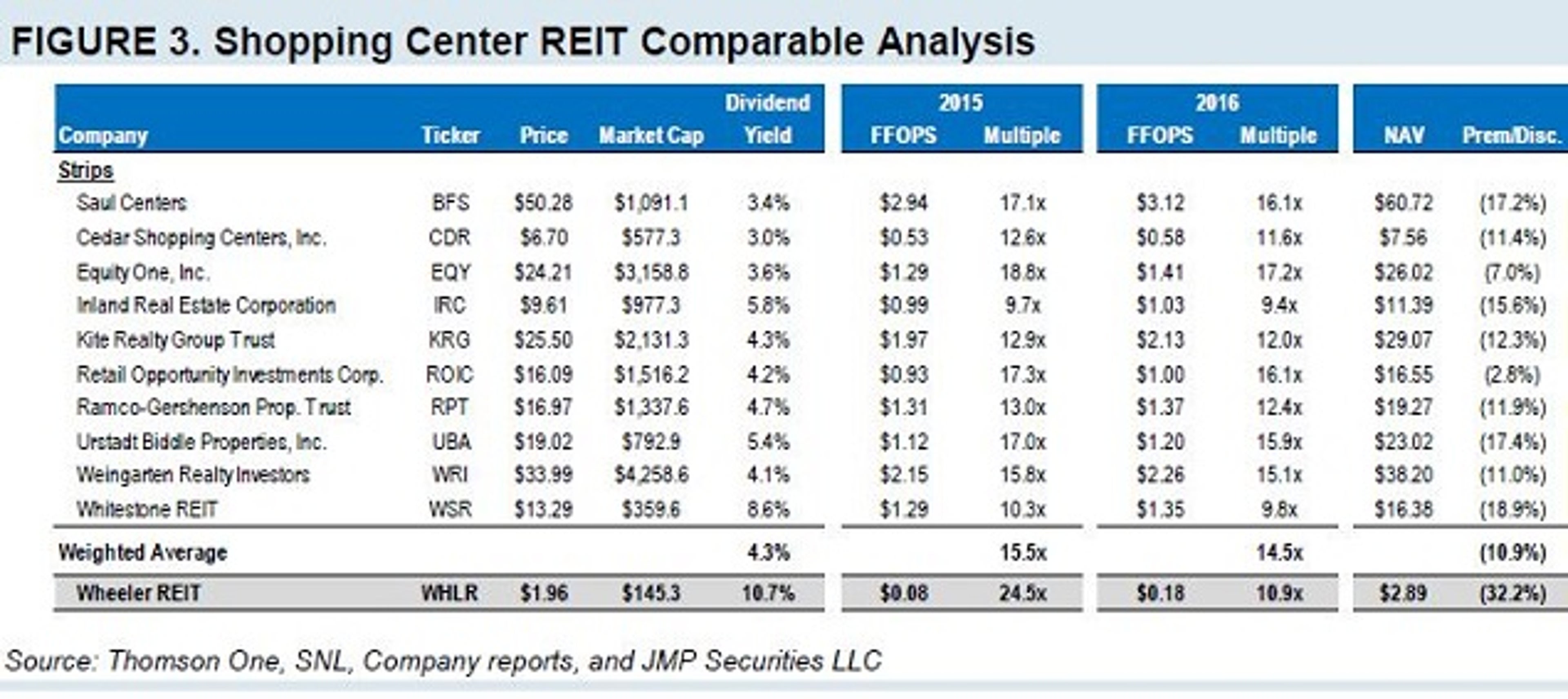

JMP - Wheeler vs Peer Group Metrics

Based on the July 9, close of $1.96 per share, WSLR was trading at over a 30 percent discount to JMP's $2.89 calculated NAV per share, vs. a peer NAV discount averaging just under 11 percent.

JMP - Wheeler Dividend Concerns

In conjunction with the equity private placement balance sheet transformation, in March 2015, Wheeler halved its prior monthly distribution from $0.035 per share, to $0.0175 per share.

"Roughly 70% of the dividend is covered in 2016, and if we adjust the dividend equivalent to 2016 AFFO, the altered yield stands at 7%, which still remains considerably ahead of peers, making this investment opportunity attractive to yield-focused institutions," according to Germain.

JMP estimates the current dividend shortfall to be $3 to $4 million, annually; however, a significant accretive growth pipeline, shown below in Fig. 12, is forecast to pick up much of the slack by year-end 2016.

JMP - Strong Wheeler Operating Metrics

Wheeler shopping centers are 90 percent grocery anchored.

The neighborhood centers sell necessities which are both recession and e-commerce resistant.

Notably, WHLR re-leasing spreads during the first quarter were close to 10 percent.

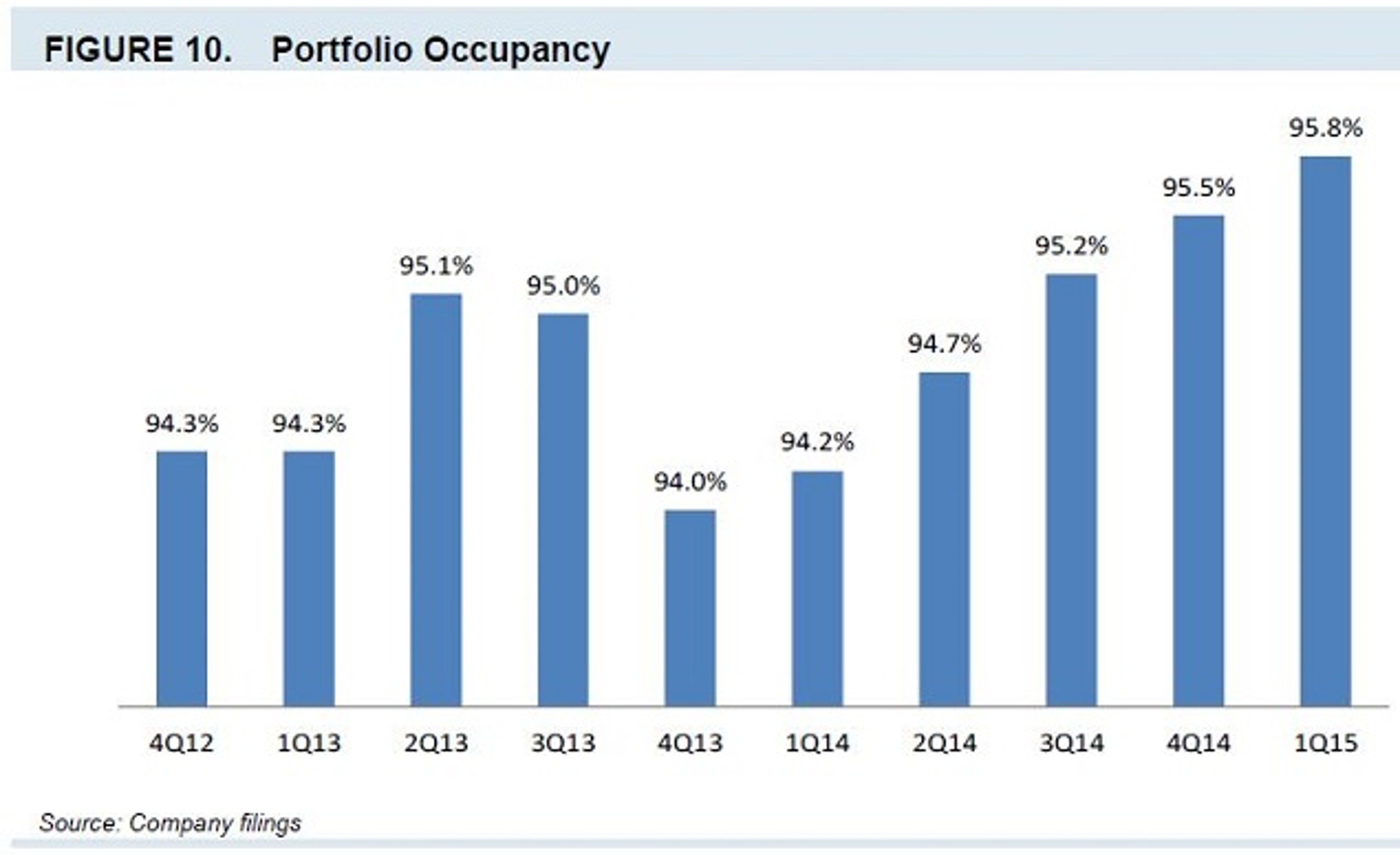

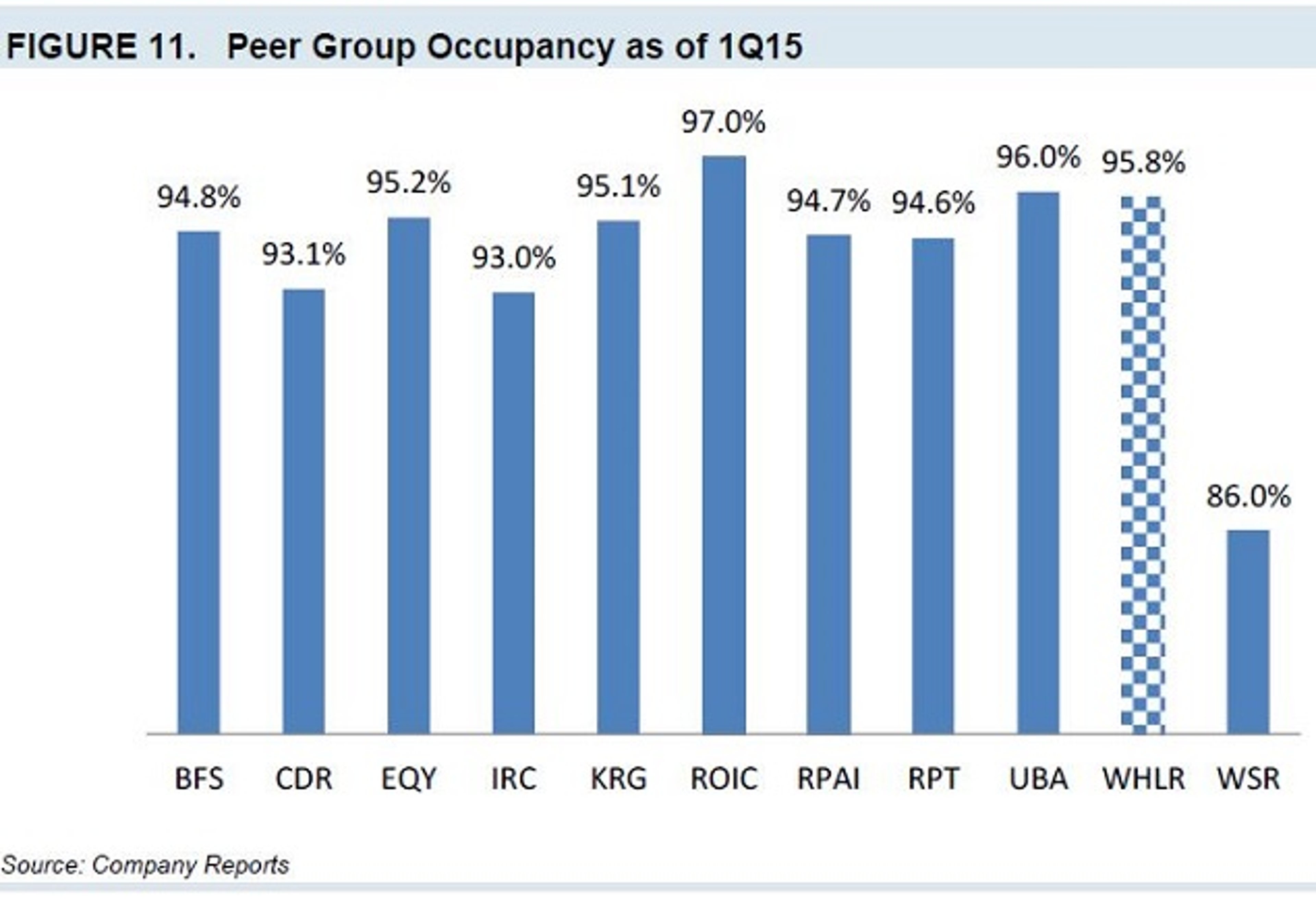

Wheeler portfolio occupancy is at the high-end of its small-cap shopping center peers.

JMP - Wheeler Acquisition Pipeline

JMP estimates Wheeler has about $170 million of dry powder to invest based upon a 55 percent LTV target.

Germain noted that the 8.6 average cash cap-rate is on stabilized assets, primarily 90+ percent leased; and he estimated levered returns in the low-teens, based upon 50 to 60 percent debt

.

JPM - Bullish Bottom Line

JPM does not see "…any headwinds given where the stock is trading currently, outside of potential liquidity constraints from some institutional investors, as the company has an ambitious growth strategy in place, along with a fiscally conservative posture toward managing the balance sheet, which we believe will result in multiple expansion."

Investor Takeaway

The old adage, "never let an old flame burn you twice," is certainly something for investors to consider.

On the other hand, JMP presented a cogent case as to why initiating a position at current levels just below $2.00 per share could be rewarding.

Wheeler REIT appears to be a special situation, suitable only for investors (or traders), who are willing to take on the risks associated with a potential 50 percent return.

Loading...

Loading...

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

date | ticker | name | Price Target | Upside/Downside | Recommendation | Firm |

|---|

Posted In: Long IdeasNewsREITDividendsSmall Cap AnalysisFinancingPrice TargetInitiationSmall CapManagementAnalyst RatingsTrading IdeasGeneralReal EstateJMP SecuritiesMitch Germainshopping centerspecial situation

Benzinga simplifies the market for smarter investing

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Join Now: Free!

Already a member?Sign in