On July 8, Barclays analyst Felicia Hendrix published a note, "Pinnacle Entertainment: You Got More, Consider the Bid," referring to Gaming and Leisure Properties, Inc. GLPI's latest offer, sweetening the pot by 54 percent for Pinnacle Entertainment, Inc. PNK's real estate assets.

GLPI was formed in November, 2013 as a REIT spin-out of Penn National Gaming PENN, and currently owns the real estate assets which are leased back to a PENN casino operating company, or OpCo.

Pinnacle issued a letter to shareholders confirming it had received the latest offer, and indicated that it was negotiating with GLPI, while simultaneously "working through" its own net-lease PropCo REIT separation plan.

Tale Of The Tape - 2015 YTD

Additionally, the GLPI shares currently pay out a dividend yielding ~6.2 percent.

GLPI - July 7, Presentation Slides

In order to accomplish this deal, Hendrix pointed out that Pinnacle would spin-out its casino OpCo in a taxable transaction to shareholders, and merge the real estate assets into the GLPI REIT.

Proposed Master Lease - Terms Similar To PENN

GLPI is proposing a triple-net Pinnacle master lease for an initial 10-year term, with five-year options.

Year 1 rent would be $377 million, based on building, land and percentage rents, as described in the slide above.

GLPI - Pinnacle Share Math

On July 8, shares of PNK closed at $39.17, down 1.2 percent on "the day the NYSE stood still," (the longest mid-day trading outage in NYSE history), giving back about 20 percent of the 5.8 percent gain from the previous day, after the proposal had been made.

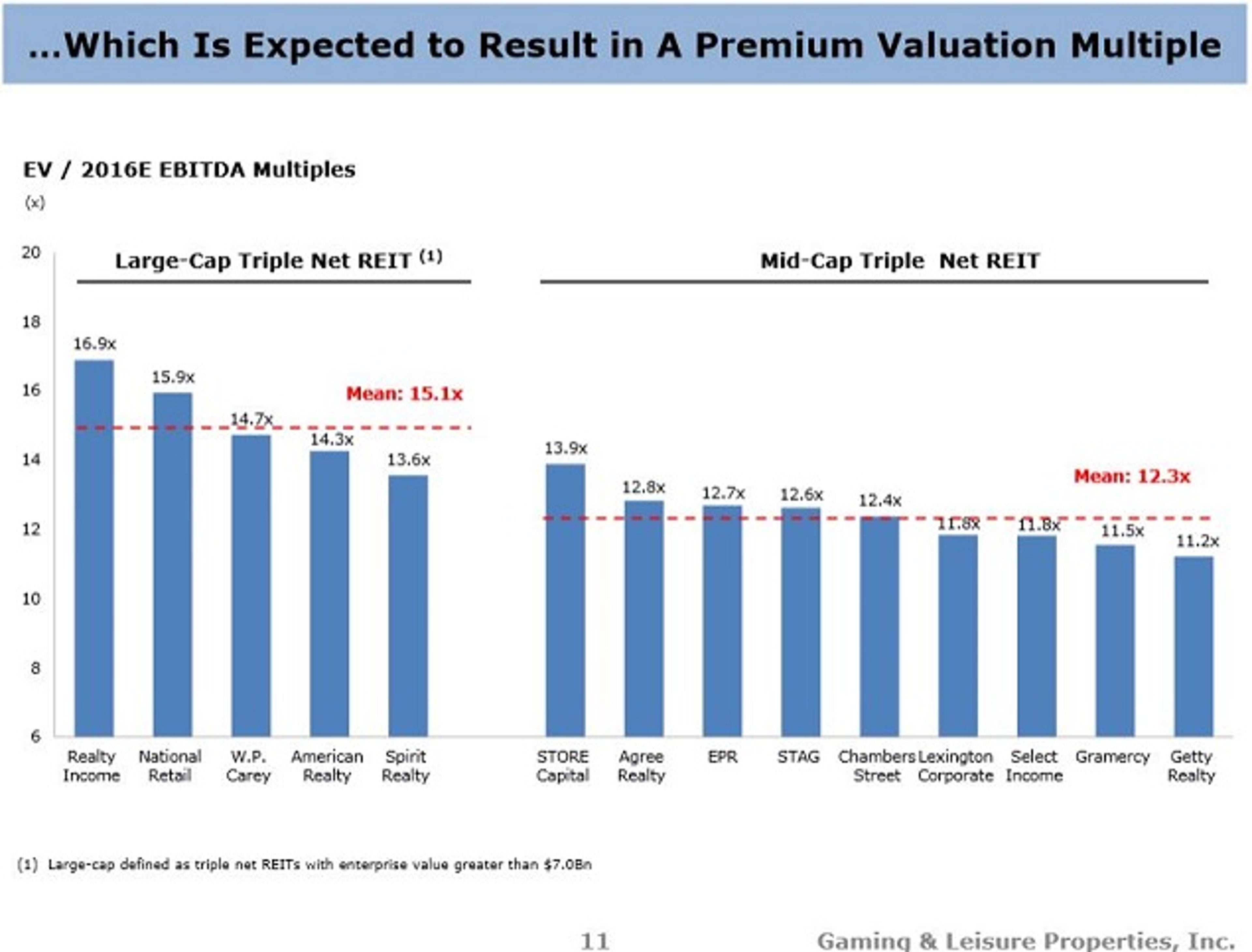

How Would The Combined REIT Stack Up?

GLPI management also makes the argument that larger cap net-lease REITs trade at higher multiples. However, a proposed REIT comprised of less than 40 properties, master-leased to two gaming industry tenants, is simply not a valid comparison.

The top single-tenant net-lease REITs own thousands of properties, leased to hundreds of tenants with both geographic and industry diversity, as well as many years of operating history. Investors should not expect similar valuations for a newly minted gaming PropCo REIT combination.

That does not take away from the fact that a gaming OpCo/PropCo arrangement does serve to unlock shareholder value.

Proposed Combined REIT Ownership

According to the July 7, GLPI letter, "Pinnacle stockholders and employee equity award holders would own 56.5 million shares in GLPI, representing an approximate 28% equity interest in the third-largest triple-net REIT by enterprise value…"

GLPI expects to issue 31 million new common shares to facilitate the transaction.

Deal Bottom Line

Hendrix calculates that a standalone Pinnacle PropCo REIT would be valued at ~$49 per share vs. an implied value of $47.48 for what appears to be the best and final GLPI offer.

She views the current GLPI offer "…as financially and strategically beneficial for both companies."

CS estimates that this transaction would "be accretive to GLPI's AFFO/share in the mid-teens percent range."

Investor Takeaway

Hendrix noted that the terms of GLPI's latest offer for Pinnacle's real estate, "…could set a new valuation level for gaming assets."

CS believes that using GLPI's EV/EBITDA, (which valued Pinnacle real estate assets at 13.3x and gaming operations at 7.5x), a REIT-spin could be significantly accretive for both $1.7 billion cap Boyd Gaming Corp. BYD and MGM Resorts International MGM.

Another analyst, Nomura's Harry Curtis was quoted in a July 8, Barron's article discussing the GLPI/Pinnacle deal, where he mentioned MGM's higher quality real estate portfolio of assets "…could fetch at least 2 turns higher valuation."

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

date | ticker | name | Price Target | Upside/Downside | Recommendation | Firm |

|---|

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.