Loading...

Loading...

On April 21, Wunderlich Securities analyst Merrill Ross published a report initiating coverage on self-storage mREIT IPO Jernigan Capital

JCAP with a Buy recommendation, and explains why JCAP's hybrid REIT business model is a winner.

There is simply no other public company with a laser focused business plan to help fund new self-storage development projects in top metro markets.

JCAP is up over 5 percent since its IPO, and Wunderlich's $25 PT represents a potential ~16 percent upside, not including dividends.

Industry Knowledge Is Key

JCAP CEO Dean Jernigan is a 30-year industry veteran, and former CEO of CubeSmart

CUBE one of the big five publicly traded self-storage REITs.

Related: Dean Jernigan Bio & Benzinga JCAP IPO Preview

According to Ross, Jernigan Capital "estimates that the top 50 MSAs could absorb 1,650 facilities over the next three years."

Wunderlich foresees Jernigan Capital achieving an eventual ROIC of ~20 percent through its hybrid construction loan product, which can result in up to a 50 percent equity participation.

A Hot Sector?

Notably, a sixth publicly traded self-storage REIT, National Storage Affiliates Trust, ticker NYSE: NSA, is expected to price this week at $15 to $17 per share, and the Benzinga IPO preview is available here.

JCAP Strategy: "Bigger Fish In A Pretty Large Pond"

Wunderlich noted, "JCAP's substantial self-storage industry knowledge and experience will position it to underwrite loans to self-storage operators and developers, even at high LTV ratios."

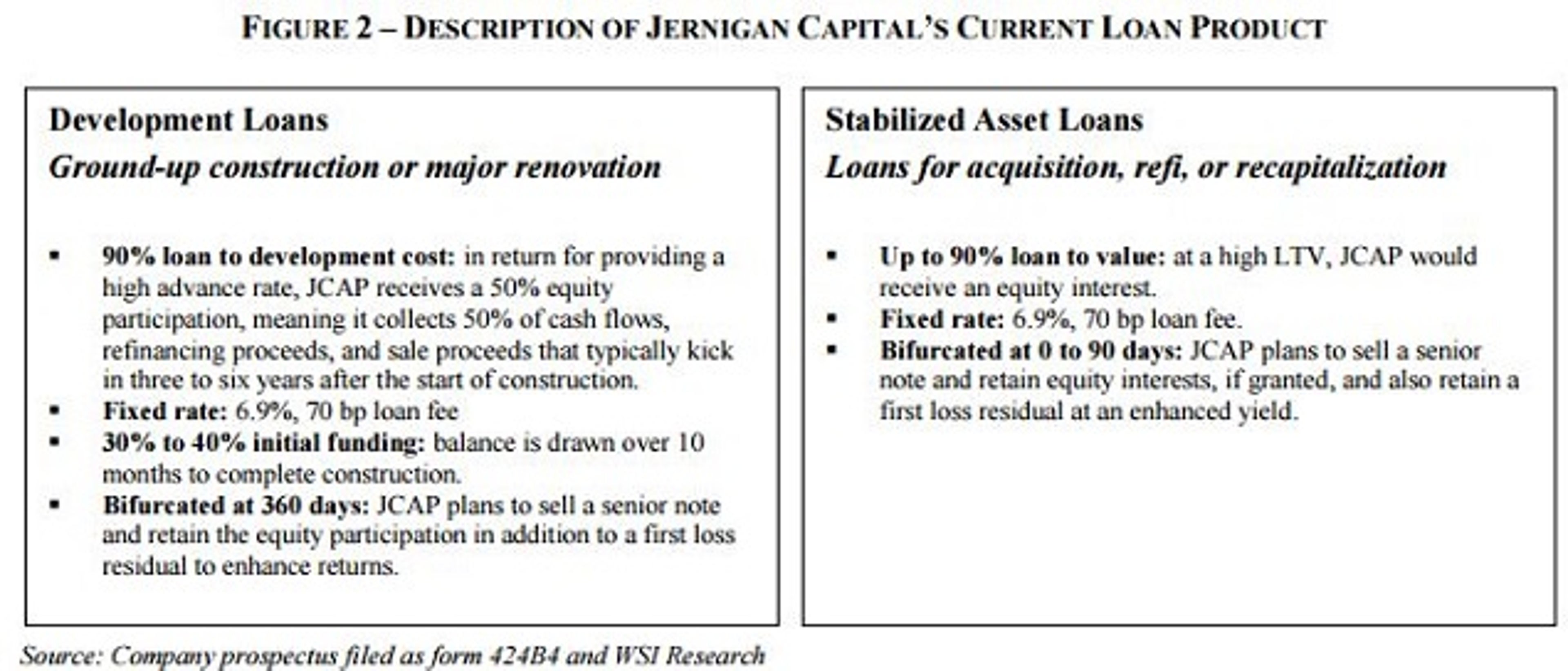

"JCAP currently offers a particular loan product: a six-year, 90% LTV loan that bears a 6.9% interest-only rate in which JCAP receives a 50% equity participation. Loans made at a lower LTV would not have an equity participation."

Wunderlich feels that "this loan will be appealing to merchant builders and that the product is likely to have little competition."

Wunderlich - JCAP Deeper Dive

JCAP also has a right of first offer on the property if it is offered for sale, which likely result in its balance sheet becoming increasing weighted toward lower risk equity REIT assets after the first three year project cycle.

However, the 14 percent unlevered returns on new construction loans would still help turbo-charge earnings.

JCAP keeps the high-yield tranche on its balance sheet, driving higher ROIC. If the properties are successfully leased to 85 percent or greater occupancy, Jernigan can put in place long-term financing, recycle capital and repeat the virtuous cycle.

Worst Case Could Be Best Case

JCAP is lending to merchant builders -- essentially development JV partners shunned by traditional lenders -- to help address the lack of new, institutional quality, self-storage facilities in otherwise healthy metro markets.

Sophisticated commercial mREITs, such as Starwood Capital and Blackstone Mortgage Trust are part of organizations with skill sets in operating, leasing and developing commercial properties unlike traditional lenders such as commercial banks.

These skill sets help to insure that loan underwriting is sound; and although it may sound a bit predatory, one way to think of programs like this is "loan to own."

They only lend on projects where they achieve targeted rates of return, and expect an even higher IRR if they were to take over the project.

Investor Takeaway

Wunderlich views the Jernigan Capital participating loans as a "zero default" business model --which will transition JCAP into a hybrid REIT with both mortgage securities and self-storage assets on its balance sheet.

If Jernigan Capital can execute on this business plan, and return ~20 percent ROIC, quite frankly, JCAP does appear to be a better mousetrap; albeit one that takes ~3 years to build and (hopefully) achieve stabilized occupancy rates.

Essentially, JCAP investors are betting on Dean Jernigan and his team's ability to underwrite well located projects, in strong markets, where the supply has been constrained -- primarily due to lack of capital.

Loading...

Loading...

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

date | ticker | name | Price Target | Upside/Downside | Recommendation | Firm |

|---|

Posted In: Analyst ColorLong IdeasREITPrice TargetInitiationAnalyst RatingsTrading IdeasGeneralReal EstateDean JerniganMerrill RossWunderlich Securities

Benzinga simplifies the market for smarter investing

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Join Now: Free!

Already a member?Sign in