Loading...

Loading...

On April 9, Jefferies analyst Omotayo Okusanya published a detailed research note explaining why the firm is lowering its rating on life science REIT BioMed Realty Trust

BMR from Buy to Hold.

In a broad sense, BioMed could be considered an office REIT, however, its bio-med/life science facilities are highly specialized, often including labs and R&D space for: pharmaceutical, education, medical and government agency tenants.

Intraday Trading - Jefferies Downgrade

During the past 52-weeks, shares of BioMed have traded in a range of $18.75 to $24.82; and are currently down over 4 percent during Thursday trading at mid-day.

Tale Of The Tape - Life Science REITs Past Year

The only other life science pure-play REIT is $6.9 billion cap Alexandria Real Estate

ARE, which currently pays a dividend yield of 3.1 percent.

BioMed currently has a market cap of $4.5 billion, and is paying a yield of 4.7 percent.

Jefferies - BioMed Realty: Downgrade Buy to Hold, Lowers PT $26 to $23

The Jefferies revised BioMed base case price target of $23 was derived from a dividend discount model (DDM); one-year forward portfolio NAV was estimated at $23.20 using a cap-rate of 6.9 percent.

Notably, Jefferies has lowered its 2015/2016 base case adjusted FFO estimates from $1.47/$1.54 to $1.41/$1.49 per share.

Occupancy is projected to increase 120 bps to 92.8 percent 2015, up 120 bps 2016; with renewal spreads of plus 5 percent.

Acquisitions projected at 6.5 percent cap-rate.

Jefferies - BioMed Base Case Rationale

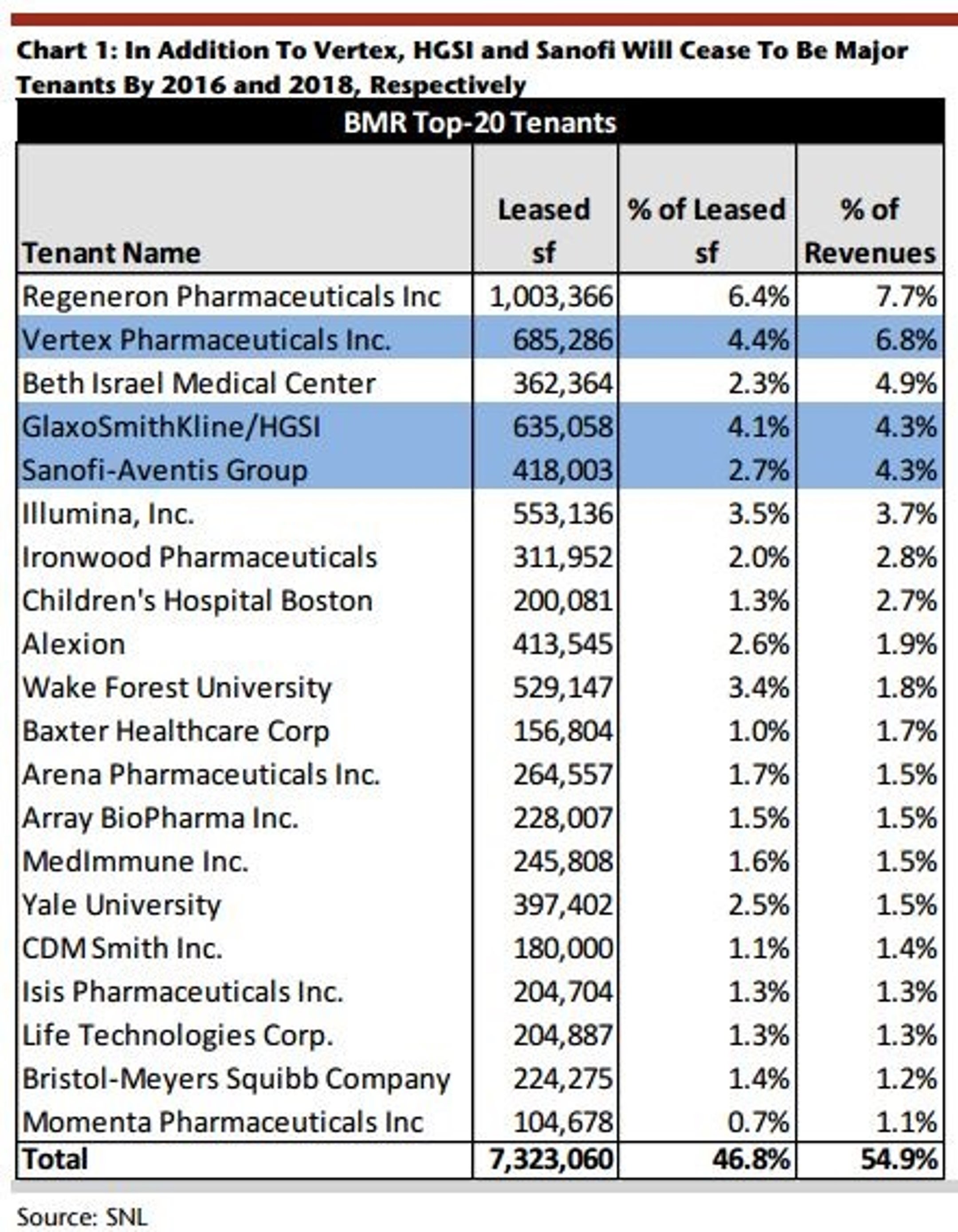

Large Lease Terminations: BMR recently terminated 313,000 SF of Vertex space in Cambridge; 105,000 SF of space at its Pacific Research Center.

Potential HSGI Purchase: Tenant HGSI, (a GlaxoSmithKline company), bought a $322.5 million property from BioMed in Q4 2014, and has a purchase option on an adjacent facility, Shady Grove in 2016.

Move-Out Announced: Sanofi, the fifth largest BMR tenant, has announced its intention to vacate 343,000 SF of its Genzyme space, and relocate to an Alexandria Realty facility in 2018.

A potential silver lining for BioMed is that demand for life science space appears to be strong in most markets; however, Jefferies believes the re-lease and reconfiguration of the space will have negative short-term impacts on FFO.

Jefferies - BioMed Upside Case

The Jefferies BioMed upside scenario price target of $28 was derived from a dividend discount model (DDM); one-year forward portfolio NAV estimate of $26.40 using a cap-rate of 6.4 percent.

Jefferies 2015/2016 upside case adjusted FFO estimates of $1.44/$1.58 per share.

Occupancy is projected to increase 240 bps to 94 percent 2015, up 120 bps 2016; with renewal spreads of plus 8 percent.

Acquisitions projected at a 7 percent cap rate.

Jefferies - BioMed Downside Case

The Jefferies BioMed downside scenario price target of $18 was derived from a dividend discount model (DDM); one-year forward portfolio NAV estimate of $20.80 using a cap-rate of 7.2 percent.

Jefferies 2015/2016 upside case adjusted FFO estimates of $1.37/$1.39 per share.

Occupancy is projected to increase 20 bps to 91.8 percent 2015, down 50 bps 2016; with renewal spreads of plus 2 percent.

Acquisitions projected at a 6 percent cap rate.

Jefferies - Bottom Line

BioMed Realty currently owns ~118 facilities containing 17 million rentable square feet.

Mr. Okusanya believes that the best long-term solution for BioMed would be to grow the scale of its portfolio to a scale where the vacancies caused by lease terminations and tenant purchase options are not as significant to earnings moving forward.

He noted that BioMed has a robust $900 million development pipeline of ~2 million SF, and that the company also has a land bank capable of supporting an additional 6.7 million SF of development.

However, there will be equity and debt raise required to fund these projects which could be a near-term drag on earnings.

Notably, there also has been significant C-Suite turnover recently, which could be a near-term concern for some investors as well.

Loading...

Loading...

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

date | ticker | name | Price Target | Upside/Downside | Recommendation | Firm |

|---|

Posted In: Analyst ColorBiotechREITDowngradesPrice TargetAnalyst RatingsGeneralReal EstateJefferiesOmotayo Okusanya

Benzinga simplifies the market for smarter investing

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Join Now: Free!

Already a member?Sign in