Loading...

Loading...

On February 26, Deutsche Bank upgraded mega-data center landlord QTS Realty Trust

QTS from Neutral to Buy, and raised its price target from $36 to $39, noting "'strong growth ahead," after the QTS Q4 earnings call.

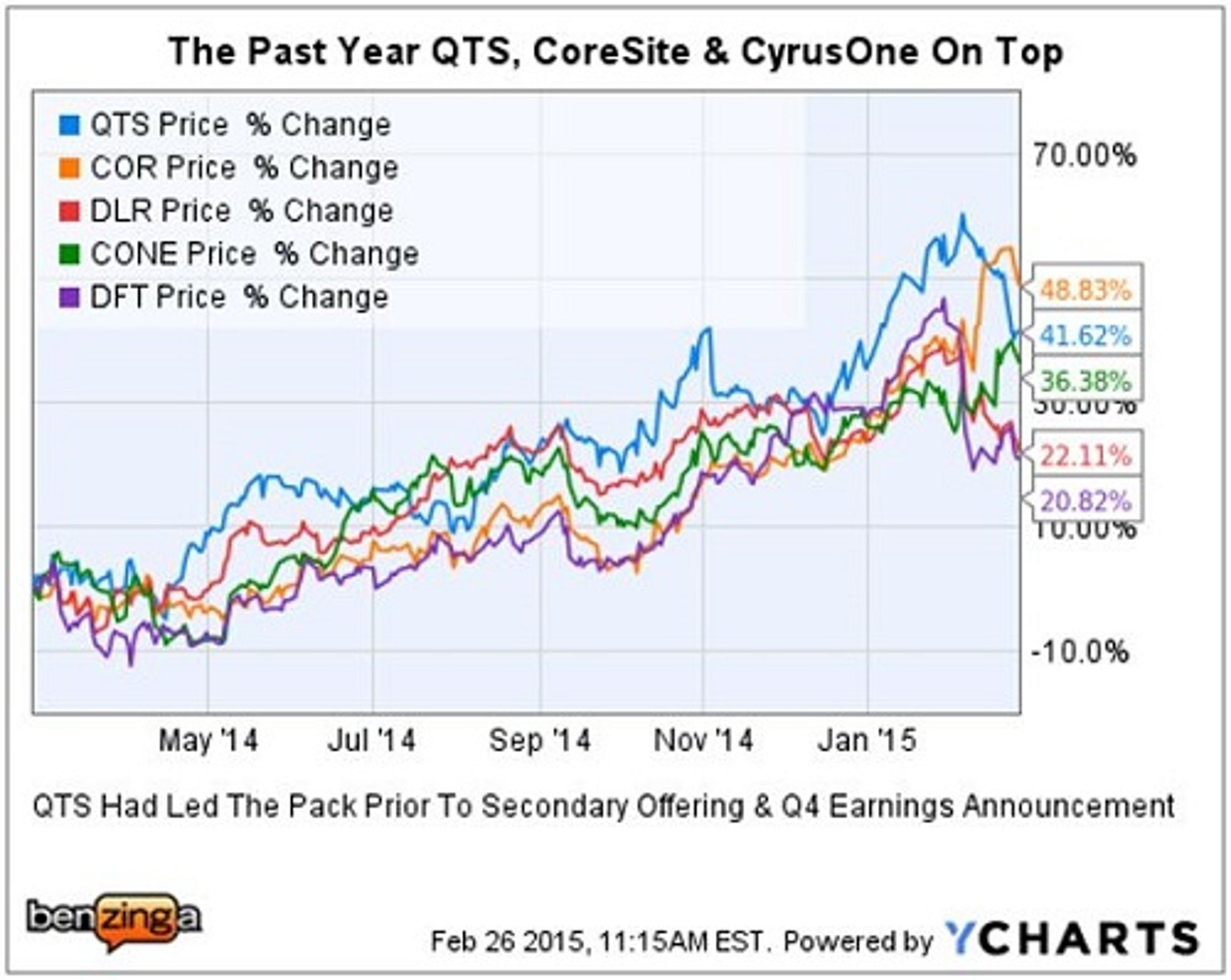

Data Center REITs - Tale Of The Tape

In addition to QTS, the two other top performing peers during the past 12 months were CoreSite Realty Trust

COR, and CyrusOne

CONE.

Deutsche Bank - QTS 'Key Concerns' Addressed

When DB initiated coverage on QTS Realty, there were three "key risks" that drove its Neutral rating: lack of operating history, above-average financial risk and ownership overhangs.

DB noted, "With these risks now diminished in our view, we are now valuing QTS at a slight premium to peers to reflect their strong execution since their IPO and an improved risk profile."

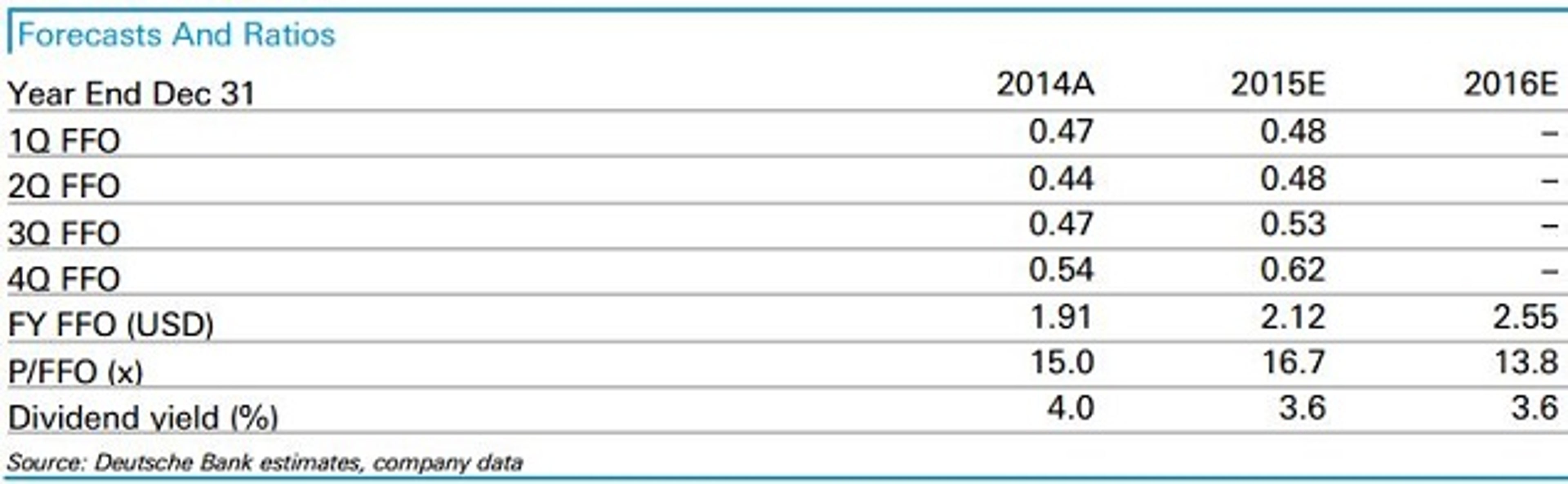

DB - Forecasts & Ratios

Deeper Dive - DB Investment Thesis

1. Operational execution has been solid:

"QTS has delivered consistently positive results since the IPO, with 2014 revenue growth of 22%, exceeding its targeted mid-to-high teens growth projection," and EBITDA up 33% also exceeding the high end of QTS's initial guidance."

DB noted, "With its 3C's platform which includes wholesale, retail, and cloud/managed services, QTS has been able to deliver steadier results that are less reliant on large wholesale deals."

"QTS has delivered a 51% annualized total shareholder return, which far exceeded the 24% return for the RMZ."

2. More comfortable with risk profile:

Noting QTS's heavy development pipeline, "we have gained some comfort in QTS's current financial risk profile as the equity offering lowers leverage near-term, helping prefund some of the company's 2015 capex spend…"

"QTS has de-risked its development via preleasing, with a current backlog of almost $58 million."

QTS "expects to spend $225-$275 million in capex in 2015, which includes the bulk of the $140 million attributable to the backlog."

DB noted, "… given its significant powered shell footprint and construction acumen, should allow [QTS] to deploy capital only when it has sufficient visibility on demand and/or preleases in hand, reducing future development risk."

3. Smaller ownership overhang; trading liquidity should improve:

"General Atlantic (GA), QTS's private equity sponsor, will sell down its stake via the 4.35 million share secondary offering and potentially an additional 1.403 million shares if the shoe is exercised."

"Following the closing of the offering GA will own 36% of QTS's common stock (32% including the shoe), down from about 56% prior to the offering."

DB noted that, "GA's stake in QTS will have been reduced to less than Cincinnati Bell's 44% stake in CONE and the Carlyle Group's 54% stake in CoreSite."

DB also noted, "The increased 'true' float should result in greater trading volumes, something that should also warrant some further multiple expansion and a larger pool of potential investors."

4. Raised target price to $39 from $36:

"…improved risk profile (balance sheet, development, ownership, and trading liquidity), and general improvements in data center valuations since our last update…"

DB note, "The increase reflects a change in our valuation methodology to one that is in line with the methodology we use for CONE, which includes a 50:50 blend of our EBITDA and FAD multiple based targets."

5. So why move to Buy now?

"Though the shares are up substantially since IPO, we see a long tail on the QTS growth story in light of its ability to more than double its sellable square footage within its existing footprint."

"Nearer term we believe QTS has the best EBITDA growth profile within the data center sector with 20% annualized EBITDA growth expected over the next 2 years versus about 12% for peers."

"QTS's current guidance also appears conservative [compared with] our current model…"

DB believes "the pullback in the shares from the pre-offering price provides a good entry point for investors."

Loading...

Loading...

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

date | ticker | name | Price Target | Upside/Downside | Recommendation | Firm |

|---|

Posted In: Analyst ColorREITUpgradesPrice TargetAnalyst RatingsGeneralReal EstateCarlyle GroupCincinnati BellDeutsche BankV

Benzinga simplifies the market for smarter investing

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.

Join Now: Free!

Already a member?Sign in