The Holy Grail for investors would be to find stocks that pay a huge yield, yet are also poised for profitable growth.

Here are three contenders:

- Preferred Apartment Communities APTS yielding 7.34 percent,

- Independence Realty Trust IRT yielding just over seven percent, and;

- Micro-cap Bluerock Residential Growth REIT BRG having announced a monthly dividend of $0.96667/share -- currently yielding nine percent on an annual basis.

Part 1 of this series will focus on the most dynamic of these contenders, $150 million market cap Preferred Apartment Communities, or PAC.

A Red-Hot REIT Sector

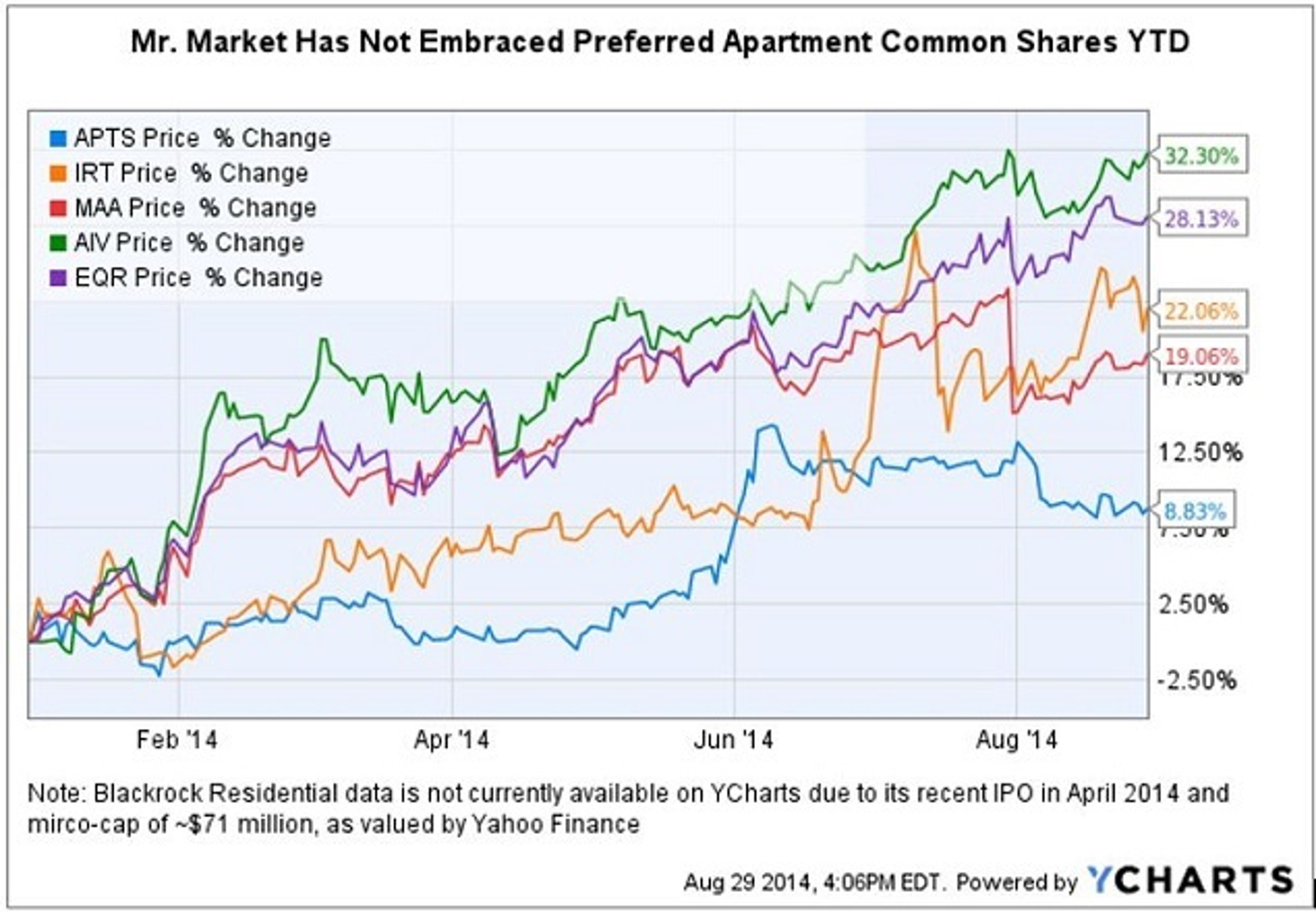

According to current NAREIT data, the multi-family sector has been crushing the market year-to-date with returns averaging ~29 percent.

A recent CNBC article pointed out two fundamental economic forces are working in tandem to boost this sector -- the strong secular trends creating an increase in demand for rentals and a lack of new apartment construction during the past five years.

When this is combined with low yields on fixed income securities such as the benchmark 10-year Treasury Note, it has co-created an ideal environment for the multi-family REIT sector to thrive.

Multi-family Apartment REIT Sector Overview

However, investors should note that when you add back in the APTS 7.34 percent dividend yield, total return for shareholders has still been better than the benchmark S&P 500 returns year-to-date.

MLV & Co. Makes A Bullish Call

On May 30, 2014 MLV & Co. initiated coverage on Preferred Apartment Communities, or PAC, with a Buy rating and a 2014 year-end price target of $13.00.

MLV analyst Ryan Meliker opined "We are initiating on Preferred Apartment Communities, Inc. with a BUY-rating and a $13 price target. Our positive view of APTS is driven by the company's unique and attractive investment strategy, coupled with a valuation disconnect, that leads to over 50% upside to our year-end 2014 price target."

"The main driver of our expectation for gross out-performance in the coming months is the value of APTS' purchase options on maturing development mezzanine loans, which we peg at $24mm, or about $1.50 per share." APTS was trading at $8.50 at the time of this note.

Great, that would take APTS to $10 per share, but how will the balance of the value be created to reach a $13.00 price target? Perhaps the answer is to be found in a few recently announced company initiatives.

What Is It About APTS That Makes It Harder For Wall Street To Value?

In a nutshell, there are quite a few moving parts and pieces to go along with the PCA primary strategy of owning and operating multi-family apartment communities, including:

- Underwriting and providing developers bridge loans and mezzanine financing as a source of capital required for land acquisition, pre-development, construction, and lease-up, in return for fees, interest, and options to purchase the newly developed communities.

- In addition to traditional apartment communities, PCA is also focused on college student housing. This is a specialty niche within the multi-family sector, which uses the "number of beds occupied" as a leasing metric, rather than the entire unit.

- The recent increasing the amount of PCA non-multifamily assets allowed as a percentage of total assets from 10 percent to 20 percent.

- This paved the way for a new Preferred Apartment Communities grocery-anchored necessity shopping center division which was announced on the Q2 earnings call, "New Markets ," with the goal of reaching large enough operational scale to spin-out a stand-alone retail shopping center REIT within ~1.5 years.

Two major deals were announced back-to-back in late July and early August of 2014 by PCA.

The Relatively Large Apartment Transactions

In its earnings release for the quarter ended June 30, 2014 PCA reported $383 million of total assets -- a 47 percent increase from $260 million reported year-over-year.

On July 25, 2014 PCA entered into a purchase agreement to purchase four apartment communities -- a total of 1,397 dwelling units -- for ~$181.7 million. This would be an increase of just over 72 percent over the 1,929 units PCA currently owns and operates.

The Q2 2014 Earnings Supplement also points out that an additional 3,491 units are under construction by way of the PCA mezzanine loan program.

If the company were to only exercise these options -- and not acquire any additional multi-family communities -- this would result in a huge 353 percent increase by 2016, over the current inventory of 1,929 units.

The PCA Shopping Center Announcement

During the Q2 earnings call there was quite a bit of discussion surrounding the purchase agreements -- previously announced on July 29 and August 1, 2014 -- PCA entered into to acquire nine grocery-anchored neighborhood centers for an aggregate purchase price of $125 million.

This transaction clearly transformed Preferred Apartment Communities from a pure-play residential housing focused REIT, to more of a diversified REIT. Of course, the mezzanine loan program and student housing initiatives certainly would contribute to that perception by Mr. Market as well.

A Recent PCA Mezzanine Loan Example

On August 19, 2014 Preferred Apartment Communities announced a mezzanine loan of up to $17.2 million for a 304 unit apartment community being developed in Northern Virginia by privately held Westport Capital Partners, LLC.

In conjunction with this mezzanine loan, APTS received an option to purchase this 304 unit community upon completion and stabilization of the project. Investment bank MLV & Co. advised PAC on this transaction.

In addition, PAC announced that it expects to partner with affiliates of Westport on similar mezzanine loan opportunities totaling another ~$275 million in development costs.

If all goes well, this will generate some additional income and create some off-market future acquisition opportunities.

Investor Takeaway

Oftentimes in the REIT sector, diversified REITs are not valued highly as pure-play REITs. This may partially explain PCA currently trading at a lower FFO multiple compared to other pure-play multi-family REIT peers.

However, there is quite a bit of due diligence required in order to try and answer one simple question. Will all of this rapid PCA growth be accretive to earnings and consequently benefit common shareholders?

Although attractive on its face, the current 7.34 percent dividend yield should only be part of the reason to invest in the common shares of Preferred Apartment Communities.

© 2024 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.

date | ticker | name | Price Target | Upside/Downside | Recommendation | Firm |

|---|

Trade confidently with insights and alerts from analyst ratings, free reports and breaking news that affects the stocks you care about.